1What a Personal Loan Actually Is (And What It Isn't)

Okay so here's the thing most articles get wrong from the jump — they treat personal loans like this mysterious financial product that needs three pages of setup before you understand it. It doesn't.

A personal loan is a fixed amount of money you borrow, pay back in equal monthly installments, at a fixed interest rate, over a set period of time. Usually 2 to 7 years. That's it. No moving parts, no rate that spikes when the Fed blinks, no minimum payments that barely dent the principal.

You ask a lender for $15,000. They approve you at 11.5% APR for 48 months. Your payment is $392/month, every month, until month 48. Then it's gone. Done. No surprises.

That predictability is the whole point — and it's actually underrated. Most people get so fixated on the interest rate number that they miss what's genuinely valuable here: you know exactly when you'll be debt-free. With a credit card, that date is a vague, anxiety-inducing somewhere-in-the-future. With a personal loan, it's a specific Tuesday in 2029.

Now, 'personal loan' is a bit of an umbrella term. What people usually mean — and what we're covering in depth here — is an unsecured personal loan. You're not pledging your house or your car. You qualify based on your credit score, income, and debt-to-income ratio. If you stop paying, the lender can't immediately grab your stuff — they have to sue you and go through collections. That's what 'unsecured' means in practice.

There are also secured personal loans, which we'll get into later, where you do put up collateral. Lower rates, higher stakes.

Personal loans can be used for almost anything. Debt consolidation (the most common use, by a lot), home improvement, medical bills, weddings, moving costs, small business startup, car repairs. Lenders technically restrict certain uses — you can't fund illegal activities or, usually, use the money to buy securities — but nobody's really checking what you bought. The stated use on your application can affect which lenders make sense, though. LightStream, for example, has specific loan programs tied to purpose (home improvement, auto, etc.) with different rate tiers.

One thing that doesn't qualify: most lenders won't let you use personal loan funds for college tuition. Use student loans for that. Different rules, better rates, more protections.

2Where Rates Are Right Now in 2026

Let me just give you the actual numbers instead of dancing around them.

As of March 2026, the average personal loan rate sits around 12.26% for borrowers with a 700 FICO score on a $5,000 loan with a 3-year term, per Bankrate data. For 5-year loans the average jumps to closer to 17-18%. Those are averages though — meaning half of borrowers are doing better and half are doing worse.

Here's how it breaks down by credit tier, roughly:

Excellent credit (760+): 6–11%. You're in LightStream and SoFi territory. The best lenders are competing for you.

Good credit (700–759): 10–16%. Still decent. Multiple good options. You might pay an origination fee to get a better rate, or find a no-fee lender at a slightly higher rate — worth doing the math.

Fair credit (640–699): 16–25%. More limited options. Upstart might actually be your best bet here because of how they underwrite (more on that later). Avant is in play. Standard bank options start disappearing.

Bad credit (below 640): 25–36%. Rough. OneMain Financial, Avant, and Upstart are basically the whole market for unsecured loans. At these rates, consolidation math gets dicey — you have to compare carefully against what you're already paying.

A few things pulling rates higher across the board right now: the Fed held rates elevated through most of 2025, and while there've been cuts, personal loan rates haven't dropped as dramatically as mortgage rates did. They tend to be stickier on the way down.

Also — and this is something I want to flag early — the rate advertised is almost never the rate you get. Lenders show their best possible rate, which goes to borrowers in the top credit tier with high income and low debt. The average borrower with 'good' credit is often getting quoted 3-5 points above the advertised floor. Always get pre-qualified with a soft pull before you apply for real.

3The 10 Best Personal Loan Lenders in 2026, Ranked

Going to give you the real rundown here. Not a list that just repeats what every other site says. These are the lenders I'd actually tell a friend to check first depending on their situation.

---

**1. LightStream — Best for Excellent Credit**

APR range: 6.49%–24.49% (with AutoPay). Zero fees. No origination, no late fees, no prepayment penalty. Nothing.

LightStream is a division of Truist Bank and they are aggressively competitive for borrowers with strong profiles. Their Rate Beat program will beat any competitor's rate by 0.10% if you show them a better offer. That's not marketing fluff — I've seen people actually use it.

The catch: you need excellent credit to get in the door. Their minimum score is technically around 660 but realistically you want 720+ to see the rates worth getting excited about. They also do hard pulls for pre-qualification, which is annoying. But if your credit is strong and you know you're getting approved, it doesn't much matter.

Loan amounts from $5,000 to $100,000. Terms from 2 to 12 years (longer for home improvement). Same-day funding possible.

---

**2. SoFi — Best Overall for Good to Excellent Credit**

APR range: 8.99%–29.99% (with AutoPay). Origination fee: 0%–7% (may be charged).

SoFi is interesting because they've gone back and forth on origination fees. For a while they were fee-free. Now some loans carry an origination fee of up to 7%, which... changes the math significantly on smaller loan amounts. Always check the Loan Estimate and calculate the all-in APR including any origination fee before accepting.

What makes SoFi worth considering even so: they have excellent member benefits, including unemployment protection (they'll pause your payments for up to 12 months if you lose your job), career coaching, and financial planning. For someone who's not just borrowing money but trying to stabilize their financial life, that stuff has real value.

Loan amounts $5,000–$100,000. Terms 2–7 years. Pre-qualification with soft pull. Funding typically within a few days.

---

**3. Discover — Best No-Fee Option for Good Credit**

APR range: 7.99%–24.99%. Zero origination fees, zero application fees, zero late fees. Straight up.

Discover is quietly one of the best options for borrowers with scores around 660–750. No fees means the APR you see is the actual cost — no origination fee hidden in the fine print adjusting your true rate upward. That's rarer than it should be.

Minimum credit score around 660. Loans from $2,500 to $40,000. Terms 3 to 7 years. Same-day funding if you deposit into a Discover account. Next business day for other banks.

The ceiling is $40K, which rules Discover out for larger consolidations.

---

**4. Marcus by Goldman Sachs — Best for No-Fee Flexibility**

APR range: 6.99%–24.99%. No fees of any kind — no origination, no late fees, no prepayment penalty.

Important caveat here: Goldman Sachs announced they're winding down new Marcus personal loans for most of the public. They're now only accepting applications from people who receive a direct mail or email invite. If you got one, use it — the product is excellent. If you didn't, it's probably not accessible to you right now.

I'm including it because a) many people have existing Marcus loans or invites, and b) the situation may change. Goldman doing classic Goldman things with their retail banking ambitions.

For those who can access it: payment deferral feature (make 12 on-time payments, defer one — interest still accrues but no late fee), flexible payment dates, good mobile app.

---

**5. Upstart — Best for Fair Credit and Non-Traditional Profiles**

APR range: roughly 7%–35.99%. Origination fee: 0%–12% of loan amount.

Upstart is genuinely different from every other lender on this list. They use an AI/ML underwriting model that looks at education, employment history, and area of study in addition to credit score. A 24-year-old with a 640 score, a CS degree from a solid school, and a software engineering job at a real company can get a dramatically better rate from Upstart than from a traditional lender.

That asymmetry cuts both ways. If your credit score undersells you — maybe you're young, maybe you had some bumps but have stable income now — Upstart is worth checking. If your credit score is fair but your education/job history is also thin, you might not see much benefit.

The origination fees are the thing to watch. Up to 12% is real, and on a $10,000 loan that's $1,200 coming straight off your proceeds. Always factor that in.

Loans from $1,000 to $50,000. Terms 3 or 5 years (limited flexibility).

---

**6. LendingClub — Best Peer-to-Peer Option**

APR range: 8.98%–35.99%. Origination fee: 2%–8%.

LendingClub has been around forever in fintech years — they're one of the original peer-to-peer lending platforms, though they've evolved significantly. They're now a licensed bank. Their underwriting tends to be a bit more flexible than pure banks, and they explicitly market to debt consolidation borrowers.

LendingClub's Balance Transfer Loan is worth calling out — they can pay your credit card issuers directly instead of depositing funds in your account. For people who want to make sure the money actually goes to debt paydown (and not, say, a spontaneous trip to Portugal), that's a legitimately useful feature.

Loans from $1,000 to $40,000. Terms 2 to 5 years.

---

**7. Best Egg — Best for Middle-of-the-Road Credit**

APR range: 6.99%–35.99%. Origination fee: 0.99%–9.99%.

Best Egg operates in that 620–700 credit score range fairly effectively. They're not the cheapest if you have excellent credit, but they're accessible and fast — funding in 1–3 business days, sometimes same day.

They've added a secured personal loan option using fixtures in your home as collateral (not the home itself, which would make it a HELOC). Niche product but it can unlock lower rates for homeowners with decent equity and credit that isn't quite prime.

Loans from $2,000 to $50,000. Terms 3 to 5 years.

---

**8. Prosper — Best for Peer-to-Peer with Co-Borrowers**

APR range: 8.99%–35.99%. Origination fee: 2.41%–5%.

Prosper is one of the other original P2P lending platforms and they allow joint applications, which is a real differentiator. If you have a spouse or family member with better credit who's willing to co-borrow, you can potentially unlock substantially better rates.

Their origination fees are on the moderate end for this type of lender. Not great, not terrible. The joint borrower angle is the main reason to choose Prosper over, say, Best Egg or LendingClub.

Loans from $2,000 to $50,000. Terms 2 to 5 years.

---

**9. Avant — Best for Bad Credit Borrowers Who Need Reasonable Terms**

APR range: 9.95%–35.99%. Origination/administration fee: up to 9.99%.

Avant's minimum credit score is around 550 — lower than almost anyone else on this list. They're very deliberately targeting borrowers who've been turned away by traditional lenders. The rates are high because the risk profile is high. That's just how it works.

But here's what matters: their APR caps at 35.99%, which is the highest most state laws allow. Payday loans and some online predatory lenders charge effective APRs in the 200–400% range. Avant at 35.99% is painful but it's not predatory.

If your score is in the 550–620 range and you need a personal loan, Avant is one of the most legitimate options available. Just go in with eyes open on the fees.

Loans from $2,000 to $35,000. Terms 1 to 5 years.

---

**10. OneMain Financial — Best for Bad Credit with Physical Branch Access**

APR range: 18%–35.99%. Origination fee: flat ($25–$500) or percentage-based (1%–10%), whichever is higher, varies by state.

OneMain is branch-based, which is either a feature or a bug depending on who you are. They have physical locations around the country and do in-person underwriting that can override what a pure algorithm would deny. Seriously — a loan officer looking at your actual situation and advocating for you still exists here.

They also accept secured loans against vehicles, which can unlock lower rates for borrowers with bad credit who own a car outright.

The minimum credit score? They don't publish one. They've approved borrowers with scores in the 500s. Their rates are expensive and the fees vary wildly by state, so you need to get an actual quote and do the math. But for someone with genuinely bad credit who can't get approved elsewhere and needs to consolidate something worse, OneMain is a real option.

You qualify on your creditworthiness alone.

4Secured vs. Unsecured Personal Loans: What's Actually Different

Most personal loans are unsecured. No collateral. You qualify on your creditworthiness alone. If you stop paying, the lender's remedies are legal — collections, credit damage, eventually a lawsuit — not physical. They can't show up and take your car.

Secured personal loans flip that. You pledge an asset — usually a car you own outright, sometimes savings deposits, sometimes home fixtures (Best Egg's niche product) — and the lender gets a security interest in it. Default, and they can legally seize and sell that asset to recoup the debt.

Why would anyone do that? Rates. Lower risk for the lender = lower rate for you. If you have bad credit but own a paid-off car worth $12,000, you might get a secured loan at 18% instead of an unsecured one at 28%. That 10-point spread on a $10,000 loan over 3 years is roughly $1,800 in interest. Real money.

The thing people get wrong about secured vs. unsecured: they think of secured loans as the last resort for people with no options. That's not right. Secured loans can be a rational choice even with okay credit if you have an asset, hate paying high rates, and have stable enough income that default is genuinely not on the table. The risk is real but so is the savings.

Where it gets dangerous: pledging a car you need to get to work. If things go sideways financially and you have to choose between the loan payment and rent, losing your car means losing your job, which means everything gets worse fast. Think hard about what you're pledging and what losing it would actually mean for your life before you sign.

Also worth knowing: OneMain Financial specifically does secured loans against vehicles and can go quite a bit lower on rate than their unsecured products for the same borrower. If you're in their credit range (bad to fair) and own your car, ask them specifically about secured options.

5Debt Consolidation Loans: The Math That Actually Matters

This is the section most people need most — and most articles whiff on because they use toy examples with round numbers that don't feel real.

Let me do real math.

Say you're carrying four credit cards. This is absurdly common:

- Card A: $4,200 balance at 22.99% APR - Card B: $6,800 balance at 24.99% APR - Card C: $2,100 balance at 21.74% APR - Card D: $3,900 balance at 26.99% APR

Total debt: $17,000. Weighted average APR: roughly 24.3%.

Minimum payments on these four cards combined might be around $450–$510/month. At minimums, you're barely moving. The interest is eating almost everything.

Now: you apply for a debt consolidation loan at 9.5% APR, $17,000, 48-month term. (Realistic for someone with a 700 score and solid income.)

Monthly payment: $431. Total interest paid over 48 months: $3,696.

Versus keeping the cards and paying that same $431/month split across them — you'd pay somewhere north of $8,000–$9,000 in interest and it would take you 5–6+ years depending on utilization creep and whether you ever add to the balances.

The savings: roughly $4,300–$5,300 in interest. Plus you go from four due dates and four logins and four minimum payment anxieties to one payment. That's not nothing.

But — and I want to be direct here — the math only works if you stop using the credit cards. This is where consolidation debt stories go wrong. You consolidate, feel psychological relief, start using the cards again because now they're paid off, and 18 months later you have the original loan AND new credit card debt. The consolidation didn't fail. You did. Know which one you're doing before you start.

Some lenders will actually pay your credit card companies directly — LendingClub does this explicitly with their Balance Transfer Loan. That removes the temptation step entirely. For people who don't trust themselves with paid-off cards, this is worth paying attention to.

Now let's factor in origination fees, because that changes the math.

If that 9.5% APR loan comes with a 4% origination fee, you need to borrow $17,708 to net $17,000 (because $17,000 / 0.96 = $17,708). The fee is deducted at funding. Your true all-in APR is now closer to 11.2%, not 9.5%.

Over 48 months at $17,708 at 9.5%: monthly payment goes to $449. Total interest: $3,856. Plus you already paid $708 in origination. Total cost: $4,564.

Still way better than the credit card scenario. But the no-fee lender at 10.5% — monthly payment $434, total interest $3,823, zero fees — is actually cheaper over the loan life despite the higher stated rate.

This is why you cannot compare personal loans by rate alone. You have to run the full numbers.

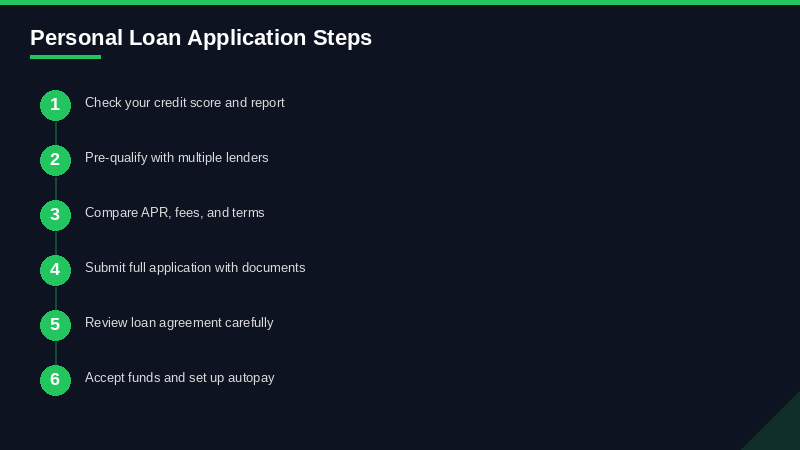

7How to Qualify: What Lenders Are Actually Looking At

People think qualifying for a personal loan is a mystery box. It's not. Lenders are looking at like five things. Understand these five things and you understand exactly where you stand.

**Credit Score**

This is the entry gate. Most lenders want 620+ for approval. 660+ for decent rates. 720+ to access the best products.

Your FICO 8 score is what most personal loan lenders pull. Some use VantageScore. A few like Upstart supplement or partially replace score with other factors.

Before you apply anywhere: pull your credit reports (annualcreditreport.com is the official free source — once a week free through 2026 per FTC rules), verify there are no errors dragging you down, and check your actual FICO 8 score through your bank or a free service. Going in blind is how you accidentally tank your score with multiple hard inquiries before realizing your score was lower than you thought.

**Debt-to-Income Ratio (DTI)**

This one surprises people. A 750 credit score does not guarantee approval if your DTI is out of control.

DTI = all monthly debt payments / gross monthly income.

So if you make $5,000/month gross and have $1,800 in monthly debt payments (mortgage, car loan, credit cards, student loans), your DTI is 36%.

Most personal loan lenders want your post-loan DTI under 40–43%. Some go up to 50% but at increasingly unfavorable terms. If adding the new personal loan payment pushes your DTI above 45%, expect either denial or a much higher rate.

The obvious lever if your DTI is the problem: pay down some existing debt before applying. Even killing a small credit card balance that has a $60/month minimum can shift your DTI meaningfully.

**Income**

All lenders want to verify income. Most accept: - Pay stubs (last 2–3) - W-2s or tax returns (last 1–2 years) - Bank statements (last 2–3 months) - For self-employed: 2 years of tax returns plus a current P&L, usually

Some online lenders do soft income verification via Plaid (linking your bank account to show deposit history). Others require hard-copy documents. Know what you're applying for before you start.

Gig workers and freelancers: this is harder than it should be. Erratic deposit patterns confuse algorithms. Self-employment income with significant deductions on your taxes can make your qualifying income look lower than your actual income. Some lenders handle this better than others — LendingClub and Upstart tend to be more flexible. Traditional bank personal loans can be brutal.

**Employment History**

Most lenders want to see at least 2 years of continuous employment, or at least a stable employment pattern. Gap in your work history in the last year? Get ready to explain it. Doesn't automatically disqualify you but it creates friction.

Recently switched jobs with a raise? Actually fine — lenders care about stability AND direction. Starting a new job at higher pay is a positive signal.

**Loan Purpose**

You'll be asked what the loan is for. Debt consolidation, home improvement, medical expenses, and major purchases all generally get better treatment than vague 'personal expenses.' It's worth being specific and honest — some lenders actually calibrate underwriting slightly based on stated purpose.

APR — Annual Percentage Rate — is supposed to be the universal comparator.

8How to Compare APR the Right Way (Real Calculator Examples)

APR — Annual Percentage Rate — is supposed to be the universal comparator. And it is, in theory. In practice, the way lenders calculate and disclose APR varies enough that you should always double-check the math yourself.

Federal law (Truth in Lending Act) requires lenders to include origination fees in APR calculation. So a loan with a 9% note rate and a 3% origination fee should show an APR higher than 9%. But the exact APR depends on loan term, when the fee is charged, and how the lender chooses to disclose it. Small variations in methodology can shift the number enough to mislead a comparison.

Here's a quick manual sanity check you can always run:

**Example 1: No-fee loan** - Loan amount: $10,000 - APR: 12% - Term: 36 months - Monthly payment: $332.14 - Total repaid: $11,957 - Total interest: $1,957

**Example 2: Loan with 5% origination fee, lower rate** - Loan requested: $10,526 (to net $10,000 after 5% fee) - APR disclosed: 10% - Term: 36 months - Monthly payment: $339.86 - Total repaid: $12,235 - Total interest paid: $1,709 — but you paid $526 in fees - Total cost: $2,235

So the lower-rate loan with the fee actually costs $278 more over the life of the loan. The APR of 10% looks better than 12% but the true all-in cost is worse.

Wait, that can't be right with proper APR disclosure, you're thinking. And you'd be right — a properly calculated APR on Example 2 would be around 12.1%, not 10%. But some lenders are calculating APR only on the amount disbursed, not the amount owed. That's the sleight of hand. Always verify.

Your manual check: multiply monthly payment by number of payments. Subtract the net amount you actually received in your bank account. That's your total cost of borrowing. Compare that single number across all options.

**Example 3: What a bad credit rate actually costs**

Same $10,000, 36 months, at 29% APR (no fee, Avant or similar): - Monthly payment: $413.37 - Total repaid: $14,881 - Total interest: $4,881

Versus carrying $10,000 on a credit card at 24.99% APR and paying $400/month: - Time to payoff: about 34 months - Total interest: approximately $3,400

In this specific scenario, the credit card actually costs less — because the payment is similar and the rate difference isn't enough to overcome it. Bad credit personal loans are not always better than credit cards. You have to run the actual math for your actual situation.

This is exactly why 'consolidate everything into a personal loan' isn't automatically good advice.

9Personal Loan vs. Credit Card vs. HELOC: Which One Wins

People treat this as a complicated question but it actually collapses to three scenarios pretty fast.

**Scenario 1: You own a home and have substantial equity**

HELOC is probably cheapest. Current HELOC rates in 2026 are running 7.5–8.5% for qualified borrowers, which beats even the best personal loan rates for most people. The risk is your house is the collateral — default and you're in foreclosure territory. But if you're disciplined and your income is stable, a HELOC for $20K+ of high-interest debt consolidation is hard to beat on pure cost.

The other HELOC gotcha: variable rate tied to prime. Your 7.8% HELOC could be 10% in two years if rates move. Personal loans lock you in.

**Scenario 2: Debt consolidation, no home equity, good credit**

Personal loan wins over credit card. You're converting revolving debt with creep risk into a fixed installment with a clear payoff date. The rate will be lower, the structure is better, and the psychological clarity of a due date is real.

0% balance transfer cards are worth considering here too — if you have good credit (680+), you can often get a 0% intro rate for 15–21 months with a 3–5% transfer fee. For someone who can pay off $8,000 in 18 months, a 3% transfer fee beats a 10% personal loan rate easily. But if the balance is larger or you need more time, the math flips.

**Scenario 3: Fair or bad credit**

Credit cards probably aren't available at decent rates anyway. HELOCs require home equity and a minimum credit score (usually 620+). Personal loans from Avant, OneMain, or Upstart become the realistic option. High rates, but structured. Better than payday loans or cash advances by a wide margin.

**Quick comparison table in plain language:**

Credit Cards: lowest friction, highest rates, revolving (no payoff date), easy to reuse (danger). Best for short-term spend you'll pay off monthly or 0% promo situations.

Personal Loans: fixed rate, fixed term, one payoff date, moderate rates, requires application. Best for medium-term borrowing with defined purpose.

HELOC: lowest rates, variable, requires home equity, slow to close, puts house at risk. Best for large amounts with stable long-term income.

Home Equity Loan (different from HELOC): fixed rate, lump sum, requires home equity, slower to close. Basically a secured personal loan using your house. Good for large one-time amounts.

The thing people miss about personal loans vs. credit cards: the discipline lock-in. A credit card lets you re-borrow. A personal loan doesn't. For certain personality types and financial situations, that structural constraint is worth paying a slightly higher rate for.

10Same-Day Personal Loans: Who Actually Funds That Fast

Yes, same-day personal loans are real. The fine print matters a lot though.

Lenders that can fund same day or next business day:

- **LightStream**: Same-day funding available on approved applications submitted before certain cutoffs. They push money via ACH. In practice, applications approved before noon on a business day can sometimes hit your account by end of day.

- **SoFi**: Can fund same-day for existing SoFi members. New applicants are more typically 1–3 business days.

- **Discover**: Same-day funding if you're depositing into a Discover bank account. Otherwise next business day.

- **Best Egg**: Advertises 1-business-day funding. Some borrowers report receiving funds same day after morning approval.

- **Avant**: Can be as fast as next business day after approval.

- **LendingClub**: Typically 2–4 business days, slower than the others.

The caveats that matter:

First, 'same-day' almost always means you submitted and completed the application before a cutoff (usually 2:00–2:30pm ET on a business day). Submitting Thursday afternoon might mean Friday or Monday funding.

Second, income verification and ID verification have to clear. If there's any document issue or your Plaid bank connection fails, add 1–2 days minimum.

Third, your bank's ACH processing time matters too. Even if the lender sends same day, some banks put next-day or 2-day holds on large ACH deposits.

Fourth: same-day for a personal loan is fast but it's not payday-loan fast. You're not walking out with cash in two hours. If you genuinely need money in 2 hours, you have different options with worse economics.

For genuine emergencies: if you have a credit card with available credit and can handle the balance, use it now and apply for a personal loan to pay it off. Better terms, and you get your immediate need handled while the loan processes.

11Co-Signer Personal Loans: How They Work and When to Use One

A co-signer is someone who agrees to be equally responsible for repaying your loan if you don't. Not secondarily responsible. Equally responsible. This is the number people miss when they ask a parent or sibling to co-sign.

If you default, the lender goes after both of you simultaneously. The co-signer's credit takes the same hit as yours. If you disappear, they're on the hook for the full balance. This is a serious thing to ask someone.

That said — done right, co-signing is a legitimate tool and can make a huge difference.

The math: say you have a 620 score and would qualify at 24% APR solo. Your parent has a 780 score. With them as co-signer, you might qualify at 12%. On a $15,000/48-month loan that's the difference between $464/month and $394/month — $70/month and about $3,360 total.

Lenders who allow co-signers on personal loans (2026): LendingClub, LightStream (joint applications), Prosper (joint), SoFi (no co-signer but joint applications). Not all lenders offer this — Upstart, Best Egg, and Avant don't allow co-signers on personal loans.

Practical advice: if you're going to ask someone to co-sign, be honest about your full financial picture. Show them your debt, your income, your budget. Don't minimize. And seriously consider setting up automatic payments — missing a payment on a co-signed loan has a way of destroying family relationships faster than almost anything else in personal finance.

For borrowers who want to improve their credit rather than just get approved once: co-signing is a short-term fix. The real play is building your own credit profile so you don't need a co-signer next time. Make every payment on time, pay it off, watch your score climb.

Credit builder loans from local credit unions are another option in this situation — small secured loans specifically designed to build payment history.

Having bad credit (FICO below 580) or fair credit (580–669) doesn't mean no options.

12Personal Loans for Bad Credit: What's Actually Available

Having bad credit (FICO below 580) or fair credit (580–669) doesn't mean no options. It means fewer options and worse terms. Let's be precise about what's out there.

First, let's define the landscape. If your score is below 580, you're essentially looking at:

- **Upstart**: They'll go down to around a 300 score in some cases because of their AI underwriting model. Seriously. But you're going to see origination fees and rates at the top of their range. A 500-score borrower might see 30%+ APR and 10%+ origination fees.

- **Avant**: Minimum around 550. APR 9.95%–35.99%, admin fees up to 9.99%. They serve this market explicitly — their whole value proposition is filling the gap between payday lenders and mainstream credit.

- **OneMain Financial**: No published minimum score. They do manual underwriting in branches. Rates 18%–35.99%, significant origination fees. Secured vehicle loans available here which can help.

- **NetCredit and OppLoans**: I didn't include them in the main lender rankings but they exist in this space too. Rates can go higher than the 35.99% cap because they operate in states with higher usury limits or through bank partnerships. Be careful. Read the fine print.

For 580–669 (fair credit), the list opens up meaningfully: add Best Egg, LendingClub, and Prosper to the above. Still expensive but you start seeing rates in the 18–25% range.

The thing I want to say directly here: if your credit score is below 600 and someone is offering you an unsecured personal loan at under 15%, be suspicious. That either means your application is being misunderstood, there's a bait-and-switch coming, or you're about to find some fees you didn't expect. Real rates for sub-600 credit are painful because the default risk is real.

Credit unions are worth checking before online lenders for this segment. Federal credit unions cap personal loan rates at 18% APR by law. If you're a member of a credit union (or can join one — membership requirements are often surprisingly easy to meet), their bad credit product might be considerably cheaper than anything online.

Also: what is the purpose of this loan? If it's to pay off higher-rate debt, the math still works even at 28% if the alternative is 36% or payday-level rates. If it's for a discretionary purchase, the cost of bad-credit borrowing should make you reconsider whether you need it now or can save up.

Upstart's AI underwriting deserves a separate note. They're looking at: education level and field of study, employment history and industry, area code/location, standardized test scores (for recent graduates), and your 'income trajectory' — not just current income. A 22-year-old with a 580 credit score and a recent engineering degree at a stable company can get treated very differently by Upstart than by a traditional underwriter. If you have a thin but positive profile, check them.

13Common Mistakes People Make with Personal Loans

Been watching people make these same mistakes for years. They're all preventable.

**Mistake 1: Not checking your credit before applying**

You apply with a 640 score expecting 15% and get quoted 25% and an origination fee. Could've checked first, spent a few months improving the score, and saved thousands. Pull your credit. Verify for errors. Know your number.

**Mistake 2: Only looking at monthly payment instead of total cost**

A 7-year loan at 12% has a lower monthly payment than a 4-year loan at 12%. It also costs you roughly 75% more in total interest. The monthly payment is not the metric. Total cost is the metric.

**Mistake 3: Accepting the first offer**

Personal loan rates vary enormously between lenders for the same borrower. Differences of 4–7 percentage points are not unusual. Get pre-qualified with 3–4 lenders (soft pulls don't hurt your score) before picking one.

**Mistake 4: Ignoring origination fees**

As covered above — a lower rate does not mean lower cost if the origination fee is high. Run total cost every time.

**Mistake 5: Consolidating debt and then running up the cards again**

I talked about this already but it deserves repeating because it's so common. The cards being paid off feels like money. It isn't. Cut them up if you have to. Freeze them in a block of ice. Do something physical that creates friction.

**Mistake 6: Borrowing more than you need**

Lenders often try to upsell loan amounts. 'You're approved for $25,000!' when you needed $12,000. The larger amount is tempting. Every dollar over what you need is a dollar you're paying interest on for no reason.

**Mistake 7: Missing the autopay discount**

Most lenders offer 0.25%–0.50% APR reduction for enrolling in autopay. That's real money. Always set up autopay. Also: you won't accidentally miss a payment.

**Mistake 8: Applying everywhere at once**

Multiple hard inquiry applications in a short window — especially spread across more than 14–45 days — can each ding your credit score. Use pre-qualification (soft pull) tools first. Then apply to your top choice or two. FICO scoring does give rate-shopping grace periods but only for certain loan types, and personal loans don't always get the same lenient treatment as mortgage inquiries.

**Mistake 9: Using a personal loan for ongoing expenses**

Personal loans are for defined, one-time borrowing needs. If you're borrowing $5,000 to cover living expenses because your income is below your spending, a loan doesn't fix the underlying problem — it kicks it 3 years down the road with interest added.

**Mistake 10: Not reading the prepayment terms**

Some lenders charge prepayment penalties. If you think you might pay off early — especially if you expect a raise, bonus, or windfall — verify there's no penalty. LightStream, SoFi, Discover, and Marcus all have no prepayment penalties.

14When You Should NOT Get a Personal Loan

This section might be the most useful one on the page and it's not going to be in most personal loan guides because those guides want you to take out loans.

Don't get a personal loan if...

**Your income is unstable and you don't have a backup plan for payments.** A personal loan payment doesn't disappear if you lose your job. Missed payments destroy your credit and trigger collection. If your income could evaporate — gig work, seasonal work, a struggling employer — think hard. SoFi's unemployment protection feature is real but it's not guaranteed and it's not forever.

**You're consolidating credit card debt but haven't changed the behavior that created it.** If you overspend relative to income and your credit cards are the evidence of that, consolidation is a delay, not a solution. The loan gets paid off and you do it again. This is a spending problem, not a debt structure problem.

**A 0% balance transfer card covers your timeline.** If your debt is manageable (under $12,000–$15,000) and you have good enough credit to get a 0% transfer card, and you can realistically pay it off within the promo period — usually 15–21 months — the transfer fee beats loan interest. Do the actual math.

**You're taking on new debt for a discretionary purchase you could save for.** Want to renovate the kitchen? Fund a vacation? Buy equipment for a hobby? If it's not urgent, saving up costs you $0 in interest. A personal loan costs you 10–25% annualized. Time the decision against how long it would take to save vs. how long you'd be paying interest.

**The loan rate isn't meaningfully better than what you currently have.** Sometimes people apply for consolidation loans and get offered rates that are only 1–2% lower than their existing debt. The math on consolidating with a 5% origination fee and saving 1.5% in rate over 4 years might barely break even. Model it.

**You're in financial crisis and considering loans to stay current on other loans.** This is the debt spiral pattern. Taking out loans to make loan payments accelerates the hole. If you're here, call the National Foundation for Credit Counseling (NFCC) before taking on more debt. Nonprofit credit counselors can often negotiate rates and payment plans directly with creditors.

**A personal loan is less obvious than I'd thought.** If you went from 'I definitely need this loan' to 'maybe I should think about this more' after reading this section — that reaction is your budget trying to tell you something. Listen to it.