1What a Savings Account Actually Is (And How It Works)

Let's be honest — most people open a savings account because their bank told them to. The branch rep was friendly, the sign-up took ten minutes, and you got a debit card in the mail two weeks later. You deposited your first paycheck and forgot about the whole thing. That's fine. But if you're still earning 0.01% APY at a big national bank in 2026, you're leaving real money on the table — and I mean that literally.

A savings account is a deposit account held at a bank or credit union that pays you interest in exchange for keeping your money there. The bank takes your deposit, lends it out to borrowers at higher rates, and splits a slice of that spread with you. Simple enough. But the difference between what big banks share with you (basically nothing) and what online banks offer (3.20% to 5.00% APY right now) is staggering.

Here's the mechanics, stripped down.

You deposit money. The bank holds it. Every day, interest accrues on your balance at whatever the daily periodic rate is — which is just your annual rate divided by 365. Most savings accounts compound interest daily and credit it monthly. That compounding is what people mean when they say 'money working for you.' It's not magic. It's just math running in the background.

Say you've got $10,000 in a savings account earning 4.00% APY with daily compounding. After one year, you've got $10,407.44 — not $10,400.00. That extra $7.44 is compounding doing its thing. Sounds tiny. Scale it to $50,000 over five years and the gap opens up considerably — you'd have $60,832 versus $60,000 simple interest. The more you have and the longer it sits, the more compounding matters.

APY versus APR is worth clarifying once and then never again. APY — annual percentage yield — accounts for compounding. APR — annual percentage rate — doesn't. When banks advertise savings rates, they use APY because it's the bigger number and it's more accurate for your actual earnings. When they advertise loan rates, they often use APR because it's the smaller number. You should only ever compare savings accounts using APY.

Savings accounts also come with some structural guardrails. Historically, federal Regulation D capped withdrawals at six per month — that rule was suspended in 2020 and hasn't been fully reinstated, but many banks still enforce it internally. Exceed their limit and you might get a fee or have your account converted to checking. Worth reading the fine print before you plan on moving money around constantly.

And the big one: FDIC insurance. Any savings account at an FDIC-member bank is federally insured up to $250,000 per depositor per institution per ownership category. Credit unions have the equivalent through NCUA. Your money doesn't disappear if the bank fails — the FDIC steps in and makes you whole up to the limit. I'll go deep on FDIC strategy later, because there are legitimate ways to push your insured coverage way above $250K without jumping through too many hoops.

2Types of Savings Accounts — They're Not All the Same

There are more flavors of savings account than most people realize, and picking the wrong type can cost you thousands of dollars per year in foregone interest. I'm not exaggerating.

**Traditional Savings Accounts**

This is the savings account your parents had. Usually offered by big national banks — Bank of America, Wells Fargo, Chase — with rates hovering embarrassingly close to 0.01% APY. They often come with monthly fees unless you maintain a minimum balance. The only real advantage is branch access and the fact that you already have a checking account at the same institution. That convenience is real. It's also not worth $1,200/year in lost interest.

The FDIC national average savings rate as of early 2026 is 0.39% APY. That's the average. Big banks drag that number down severely. You can do a lot better.

**High-Yield Savings Accounts (HYSAs)**

This is where you should be if you're leaving money in cash for any period of time. HYSAs are almost exclusively offered by online banks — Ally, Marcus, Discover, Synchrony, Barclays, and others. No physical branches means lower overhead means higher rates passed to depositors. Right now in March 2026, the best accounts are sitting between 3.20% and 5.00% APY. That's 8x to 12x the national average.

They're FDIC insured. They compound daily. They have no or very low minimum balance requirements. The main downside is the transfer lag — moving money to and from your external checking account takes 1-3 business days, which can be annoying when you need cash fast. Some people keep a small buffer in their checking account specifically to avoid that problem.

**Money Market Accounts**

Money market accounts are sort of a hybrid between checking and savings. They typically offer competitive rates — often comparable to HYSAs — plus check-writing privileges and sometimes a debit card. Great if you want easy access to your savings without a transfer lag.

The catch: they often come with higher minimum balance requirements. Some require $1,000 or $2,500 to open or to avoid fees. Rates can be tiered — you might earn a lower rate below $10,000 and a better rate above it. Don't confuse money market accounts (bank deposit products, FDIC insured) with money market funds (investment products, not FDIC insured). Same name, very different thing.

**Certificates of Deposit (CDs)**

CDs are technically savings products but work differently — you lock your money up for a fixed term (3 months to 5 years) in exchange for a guaranteed rate. You give up liquidity for predictability. If rates drop after you open your CD, you're still earning whatever rate you locked in. If rates rise, you're stuck at the lower rate until maturity (or you pay an early withdrawal penalty to get out).

In early 2026, the best 1-year CD rates are sitting around 4.50-4.80% APY — a bit higher than HYSAs — which is the expected premium for giving up liquidity. I'll compare these more directly in a later section.

**Specialty Savings Accounts**

These serve specific purposes:

— *Kids' savings accounts*: Usually joint accounts or custodial accounts (UGMA/UTMA) opened by parents. Some banks offer dedicated kids accounts with modest rates and educational tools. Rates are often mediocre.

— *Health Savings Accounts (HSAs)*: For people with high-deductible health plans. Triple tax advantage — contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Not a traditional savings account but behaves like one and is genuinely one of the most powerful savings vehicles available.

— *Individual Retirement Accounts (IRAs)*: Not savings accounts in the traditional sense, but some people hold their IRA cash in savings-like vehicles while deciding how to invest. Some banks offer IRA savings accounts.

— *Business savings accounts*: Separate accounts for business cash. Usually earn less than personal HYSAs. More on those later.

— *Goal-based savings accounts*: Some banks (Ally's bucket system, for instance) let you earmark portions of your savings for specific goals — vacation, car, emergency fund — within a single account. Mostly a UX feature but genuinely useful for people who want to track savings goals without opening a dozen accounts.

3The 2026 Rate Environment — What's Actually Happening

Here's where we are right now, and honestly the story is more interesting than just a rate table.

The Fed spent 2022 and 2023 hiking rates aggressively to fight inflation — the federal funds rate went from near zero to 5.25-5.50%, the highest it had been in 22 years. Banks, especially online banks, followed and pushed HYSA rates above 5.00% by late 2023. It was genuinely a golden era for cash holders. I had money sitting in Ally earning 5.00% with no risk and full liquidity. That felt almost wrong.

Then the Fed started cutting. Three cuts in late 2024, bringing the rate down. By January 28, 2026, the federal funds rate was holding at 3.50-3.75%. Markets are now pricing in maybe one or two more cuts in 2026 — Goldman Sachs is calling for a 25bp cut in June and another in September, though that's far from certain.

What this means for you: rates have come down from the 2023 peaks but are still historically attractive. If the Fed does cut twice more in 2026, you'll see HYSAs drift toward 3.00-3.25% by year-end. They're not going back to 0.01% anytime soon, but the easy-money era for cash is probably past peak.

Lock in what you can. The case for moving money to an HYSA is still strong.

Here's where major banks are sitting as of mid-March 2026:

| Bank | APY | Min Balance | Monthly Fee | Notes | |---|---|---|---|---| | Varo Bank | 5.00%* | $0 | None | *Requires $1,000/mo direct deposit; 5% on first $5,000 only, 2.50% above | | Synchrony | 3.50% | $0 | None | Formerly higher; has cut with Fed | | Barclays | 3.70-3.85% | $0 | None | 3.85% on $250K+ balances | | Wealthfront | 4.00% | $1 | None | Cash Account; up to $8M FDIC via partner banks | | Betterment | 4.00% | $0 | None | Cash Reserve; similar partner bank FDIC structure | | American Express HYSA | 3.90% | $0 | None | No ATM access | | Discover | 3.80% | $0 | None | Solid app, no Discover credit card required | | Ally | 3.20% | $0 | None | Has cut rates significantly from 2023 peak | | Marcus by Goldman Sachs | 3.65% | $0 | None | No app transfers via Zelle, but solid otherwise | | Openbank (Santander) | 4.09% | $500 | None | Relatively new entrant to US market |

A few things worth noting about this table.

Varo's 5.00% is real but conditional. You need $1,000/month in direct deposits to qualify, and the 5.00% rate only applies to balances up to $5,000. Anything above that earns 2.50%. If you're trying to park $30,000, the blended rate is much lower. Do the math for your actual balance before chasing that headline number.

Ally has been disappointing, honestly. I've had an Ally account since 2019 and they were genuinely competitive for years. Their rates tracked the Fed closely going up. Coming down, they've been faster to cut than I'd like — from 4.35% in mid-2023 to 3.20% today. The app is still excellent and the bucket system is useful, but purely on rate, other options are beating them right now.

Wealthfront and Betterment offer their rates through networks of partner banks, which also lets them extend FDIC coverage way beyond the standard $250K limit. More on that in the FDIC section. If you have large cash balances, that matters a lot.

Openbank is newer to US consumers but it's owned by Santander, which has been around forever. The 4.09% APY is competitive and the $500 minimum is reasonable. Worth considering if you can meet that minimum.

The broader point: the difference between a 0.01% big-bank account and a 3.50-4.00% HYSA on a $25,000 balance is roughly $875-$1,000 per year. That's a car payment. It's a vacation. Leaving that on the table because you haven't gotten around to opening an account is one of the most expensive forms of financial procrastination there is.

APY is the headline but it shouldn't be the only number you look at.

4How to Actually Compare Savings Accounts

APY is the headline but it shouldn't be the only number you look at. Here's the full framework I use.

**APY — But Read the Fine Print**

The advertised APY is the starting point, not the ending point. Ask: — Is there a minimum balance to earn that rate? (Some banks offer 0.01% on low balances and the headline rate only above $1,000 or $2,500) — Is the rate tiered? (Higher balances sometimes earn more, sometimes less) — Are there conditions attached? (Varo's 5.00% requires monthly direct deposit) — Is it an introductory rate? (Some banks offer promotional rates for the first few months that drop sharply afterward — Cit Bank and a few others have done this)

An account advertising 4.50% with a $10,000 minimum and an intro rate that expires after 6 months is not better than an account offering 3.90% on any balance permanently. Do the math over 12 months, not just month one.

**Fees**

Monthly maintenance fees are the most common. A $10/month fee on an account earning 3.00% APY means you need roughly $4,000 sitting there just to break even on the fee. Most HYSAs at online banks have no monthly fees at all, which is why they're generally better than traditional savings accounts.

Other fees to watch: excessive withdrawal fees (some banks still charge if you exceed 6 transactions/month), incoming wire fees, paper statement fees. None of these are dealbreakers individually but they add up.

**Minimum Balance Requirements**

Some accounts require a minimum to open, a minimum to earn the advertised rate, or a minimum to avoid fees. These are three different things and they're not always the same number. An account might have a $0 minimum to open, $500 minimum to earn the advertised rate, and a $300 minimum to avoid a $5/month fee. Read all three before you commit.

**Deposit and Withdrawal Mechanics**

How fast can you get your money when you need it? For most HYSAs, transferring money to an external checking account takes 1-3 business days via ACH. Some banks offer same-day transfers or instant transfers for an additional fee. Ally, for example, offers free standard transfers in 3 days or faster transfers for a fee.

If you're using this account as an emergency fund, that 3-day lag matters. Either keep a small buffer in checking, or choose a money market account with ATM access.

**ATM Access**

Most savings accounts don't come with an ATM card. Money market accounts often do. If you need the ability to withdraw cash directly from your savings, check whether the account comes with a debit card or ATM card, and whether there's a fee for ATM use.

**Mobile App Quality**

This is surprisingly important and under-discussed. A bad app creates friction that makes you less likely to actually manage your savings well. The best apps in this space right now are:

— **Ally**: Clean UI, bucket savings feature, good mobile deposit — **Marcus**: Simple and reliable, though less featured than Ally — **Discover**: Very polished, good account management — **Wealthfront**: Excellent UX, especially if you also invest with them

Bigger banks have improved their apps significantly but they're still generally behind fintech-native products.

**Customer Service**

You hopefully won't need it often. But when you do — locked out of your account, suspicious transaction, incorrect interest posted — you want to actually reach someone. Ally and Discover have 24/7 phone support with short wait times in my experience. Marcus has been more hit or miss. Newer fintechs sometimes rely heavily on chat support which can be frustrating for urgent issues.

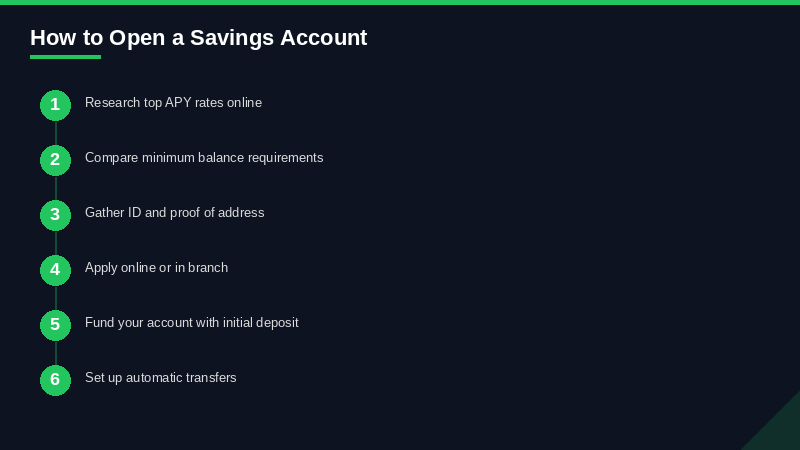

**Account Opening Requirements**

Most banks require a Social Security number, a government ID, and a funding source. Some do a soft credit pull (Discover, for instance) — won't affect your credit score but they're checking. A few do hard pulls for certain products. Read the disclosures. Opening a savings account is generally much easier than a credit card application, but there are still requirements.

**FDIC Status**

Every account you're seriously considering should be FDIC insured (or NCUA for credit unions). Check the FDIC's BankFind tool if you're not sure. Some fintech apps that look like banks aren't actually banks — they're apps with banking-as-a-service backends. Usually still FDIC insured through the partner bank, but the coverage mechanics work differently. Confirm before you deposit large sums.

5Best Savings Accounts of 2026 — Ranked and Reviewed

These aren't affiliate picks. These are the accounts I'd actually consider based on rate, features, and reliability.

**1. Varo Bank — Best for Direct Deposit Users Who Can Max the Conditions**

Rate: 5.00% APY (on first $5,000; 2.50% above) Minimum: $0 Fees: None

Varo is the rate leader for balances under $5,000 if you're getting a paycheck via direct deposit. The 5.00% rate is legitimate — I've seen people confirm it for months running. But it is genuinely conditional. You need $1,000+ in direct deposits per month and a positive balance in both accounts at month-end. Miss either condition in a given month and you drop to 2.50% for that month.

For someone with a job and regular direct deposit, this is almost effortless to qualify for. For freelancers, business owners, or people with irregular income, it's genuinely annoying.

Also the math: 5.00% on $5,000 and 2.50% on anything above. If you have $20,000, the blended rate is about 3.12%. Suddenly not so special. Varo makes the most sense if your cash savings is under $5,000 and you already use them for direct deposit.

**2. Wealthfront — Best for Large Cash Balances**

Rate: 4.00% APY Minimum: $1 Fees: None

Wealthfront's Cash Account is technically not a savings account — it's a cash management account — but it functions like a HYSA and earns 4.00% APY on any balance. What makes it compelling for larger balances is the FDIC coverage: Wealthfront spreads your money across a network of partner banks, giving you up to $8 million in FDIC insurance. That's not a typo.

If you have $500K sitting in cash — maybe you sold a house, got an inheritance, or are in between investments — this is genuinely one of the best solutions out there. You get market-rate APY on the full balance and more FDIC coverage than you could ever engineer manually. The app is excellent. The investing platform is right there if you want to put money to work beyond cash.

**3. Betterment Cash Reserve — Best Combination of Rate and Coverage**

Rate: 4.00% APY Minimum: $0 Fees: None

Similar structure to Wealthfront. 4.00% APY, up to $2 million in FDIC coverage through partner banks, no minimum, no fees. Betterment's investing platform is also strong. If you're already investing with Betterment, holding cash here makes the portfolio management cleaner.

The rate has been stable — they pass through changes from their partner banks but don't tend to make dramatic sudden moves. Solid and boring, which is exactly what you want from a cash account.

**4. American Express High Yield Savings — Best for Amex Cardholders**

Rate: 3.90% APY Minimum: $0 Fees: None

Amex's HYSA doesn't get enough attention. 3.90% APY, no minimum, no fees, and the Amex brand has serious backing. Transfers to/from external accounts are clean. The only real downside is that you can't get cash via an ATM — there's no debit card on this account. Pure savings vehicle only. If you're an Amex cardholder already and want to keep your financial relationship consolidated, this is a strong option.

**5. Barclays Online Savings — Best for Reliable Rate History**

Rate: 3.70-3.85% APY Minimum: $0 Fees: None

Barclays has been consistently competitive since they entered the US online savings market years ago. The rate is tiered — 3.70% below $250K, 3.85% above it. Most people won't hit the $250K threshold, so call it 3.70% in practice. Not the absolute highest but Barclays has a reputation for not playing games with teaser rates. The account does what it says.

**6. Discover Online Savings — Best All-Rounder**

Rate: 3.80% APY Minimum: $0 Fees: None

Discover's savings account is about as clean as it gets. No minimum, no fees, 3.80% APY, excellent app, 24/7 customer service. You don't need a Discover credit card to open one. Transfers are reliable. Discover also has a good cashback checking account that pairs well if you want to consolidate banking.

The rate is slightly below some competitors right now, but Discover's track record on customer service and reliability is stronger than many. Sometimes you pay slightly for that dependability.

**7. Marcus by Goldman Sachs — Best for Goldman Credibility**

Rate: 3.65% APY Minimum: $0 Fees: None

Marcus has the Goldman Sachs name behind it, which genuinely matters for large deposit holders who care about institutional credibility. The rate at 3.65% is slightly behind some competitors but Marcus has historically been reliable. No minimum, no fees. The app is simpler than some others — less featured — but that simplicity also means less to go wrong.

Marcus went through some internal restructuring at Goldman Sachs in 2022-2023, including pausing some products temporarily, which spooked some users. The savings account was never at risk but it's worth knowing that history.

**8. Openbank High Yield Savings — Best Emerging Option**

Rate: 4.09% APY Minimum: $500 to open Fees: None

Openbank is Santander's digital banking arm and has been quietly competitive in the US market. 4.09% APY beats most of the legacy players, and the $500 minimum to open is reasonable. Santander's backing means this isn't some venture-funded fintech that could disappear. Worth considering if you can meet the opening minimum.

**9. Ally Online Savings — Best Savings Features and UX**

Rate: 3.20% APY Minimum: $0 Fees: None

Ally's rate has slipped relative to competitors, which is frustrating. But the product features remain best-in-class. The bucket system lets you mentally earmark money within a single account without opening separate accounts — really useful for goal-based saving. The app is excellent. Customer service is 24/7 and actually answers. If you're optimizing for product quality and don't mind trading a bit of APY, Ally is still worth considering.

**10. Synchrony High Yield Savings — Best Simple Option**

Rate: 3.50% APY Minimum: $0 Fees: None

Synchrony is no-frills in the best way. Rate has come down from where it was, but 3.50% is still solid. The account comes with an optional ATM card (rare for a pure savings account), which makes Synchrony uniquely useful if you occasionally want ATM access to your savings. No fees, no minimums.

**Full Comparison Table**

| Bank | APY | Min to Open | Monthly Fee | ATM Access | FDIC Coverage | Best For | |---|---|---|---|---|---|---| | Varo | 5.00%* | $0 | None | No | $250K | Direct deposit users, balances under $5K | | Wealthfront | 4.00% | $1 | None | No | Up to $8M | Large cash balances | | Betterment | 4.00% | $0 | None | No | Up to $2M | Combined investing + savings | | Openbank | 4.09% | $500 | None | No | $250K | Competitive rate seekers | | Amex HYSA | 3.90% | $0 | None | No | $250K | Amex cardholders | | Discover | 3.80% | $0 | None | No | $250K | All-around best product | | Barclays | 3.70% | $0 | None | No | $250K | Reliable long-term rate history | | Marcus | 3.65% | $0 | None | No | $250K | Goldman Sachs brand trust | | Synchrony | 3.50% | $0 | None | Yes (optional) | $250K | ATM access with HYSA rate | | Ally | 3.20% | $0 | None | No | $250K | Best savings features and UX |

*Varo 5.00% requires $1,000/mo direct deposit, applies to first $5,000 only

6Online Banks vs Traditional Banks — This Isn't a Close Fight

I'll save you the false balance: online banks win on rate. It's not even close and it hasn't been close for years.

The average savings rate at the four biggest US banks right now — Bank of America, Wells Fargo, Chase, Citibank — is somewhere between 0.01% and 0.50% APY depending on account type and balance. The best HYSAs are at 3.50-4.00%+. On a $20,000 balance, that's the difference between earning $20/year and earning $700-800/year. The math is embarrassing for big banks.

Why do big banks pay less? A few reasons.

First, overhead. Physical branches are expensive. Chase has thousands of them. Every teller, every lease, every ATM costs money. Online banks don't have that cost structure and pass the savings to depositors — in the form of higher rates and lower fees.

Second, deposit stickiness. Big banks have massive existing customer bases who are inertial. They know most of their depositors won't bother to move money for a few percentage points. So they don't need to compete on rate. Online banks don't have that cushion — they have to earn deposits with competitive rates because they don't have the branch relationships and brand inertia.

Third, funding costs. Big banks have diverse funding sources. They don't depend heavily on retail deposits to fund their lending. Online banks and fintech-native banks often rely more on retail deposits and thus have to price them more attractively.

That said, there are real tradeoffs with online-only banking.

*Cash deposits are harder.* Most online banks don't accept cash deposits. If you have cash that needs to go somewhere, you might need to deposit it at a traditional bank account and then transfer. Some online banks have workarounds — Ally, for instance, partners with Allpoint ATMs for cash withdrawals but cash deposits are still limited.

*Relationship banking disappears.* If you need a mortgage, a small business loan, or a line of credit, having a long-standing relationship with a local banker can matter. Online banks don't offer that. For pure savings, this is irrelevant. For people who want their full financial life in one place, it's worth considering.

*The 1-3 day transfer lag.* Already mentioned this but worth repeating. Moving money from your online HYSA to your checking account takes 1-3 business days for standard ACH. In an emergency at 6pm on a Friday, that's a genuine problem if you don't maintain a buffer.

For most people — honestly, the vast majority of people reading this — the online bank advantage on rate is real enough and the tradeoffs manageable enough that you should have at least one HYSA at an online bank for your serious savings. Keep a small checking buffer at your traditional bank for day-to-day stuff. Let the bulk of your cash earn real interest somewhere that actually pays you.

Credit unions deserve a mention here. They're member-owned, not-for-profit, and often offer competitive rates. Navy Federal Credit Union, Alliant Credit Union, and Pentagon Federal (PenFed) regularly compete with the best online bank HYSAs on rate while offering better customer service than some digital-only banks. Eligibility requirements vary — some credit unions are geographically restricted or require membership in a specific group — but if you qualify for one of the major ones, it's absolutely worth checking their rates.

7Savings Account Fees and How to Avoid Every Single One

Fees on savings accounts are either completely avoidable or a sign you're at the wrong bank. Let's run through them.

**Monthly Maintenance Fees**

The most common fee. Traditional banks charge $5-15/month unless you maintain a minimum balance or meet direct deposit requirements. Bank of America's Advantage Savings charges $8/month unless you maintain $500 minimum. That's $96/year — more than you'd earn in interest at their 0.01% rate on $96,000. The fee-free solution: move to an online bank. Every major HYSA has zero monthly fees.

**Excessive Withdrawal Fees**

Even though federal Regulation D transaction limits were suspended in 2020, many banks still enforce a 6-per-month withdrawal limit on savings accounts and charge $3-10 per excess transaction. This matters if you use your savings account like a checking account. Don't. Savings is for money that sits. For frequent transactions, use checking. If you need the rate but also the access, a money market account might be the better product.

**Wire Transfer Fees**

Incoming domestic wires at most banks: free. Outgoing domestic wires: $15-30. International wires: $25-50 or more. If you're moving large amounts and wire speed matters, check the fee schedule. For most savings purposes you're using ACH transfers anyway, which are free.

**Paper Statement Fees**

Some banks charge $1-3/month if you want paper statements instead of electronic. Go paperless. You already get transaction alerts on your phone. This fee is completely optional.

**Returned Payment Fees**

If you try to fund your savings account with a transfer that bounces (the source account doesn't have the funds), you might get hit with a returned payment fee of $10-30. The fix: don't overdraw the funding account.

**Below-Minimum Balance Fees**

Some accounts require you to maintain a minimum balance and charge a monthly fee if you fall below it. The minimum might be $300, $500, or $1,000 depending on the bank. This is separate from the minimum to open the account. Read the account disclosure carefully.

**How to Completely Avoid Fees**

Honestly, it's simple: choose an online bank HYSA with no monthly fees, no minimums, no excess transaction fees. Wealthfront, Betterment, Ally, Marcus, Discover, Amex, Varo, Synchrony — all zero monthly fees. None of them charge you for the privilege of keeping your money there. If your savings account charges you monthly fees in 2026, the account is the problem, not your balance.

FDIC insurance is maybe the least glamorous topic in personal finance and also one of the most important.

8FDIC Insurance — The Deep Dive

FDIC insurance is maybe the least glamorous topic in personal finance and also one of the most important. If you've got serious money in savings, you need to understand this beyond the headline $250K number.

**The Basics**

The Federal Deposit Insurance Corporation (FDIC) was created in 1933 after roughly 9,000 banks failed during the Great Depression and depositors lost everything. The FDIC insures deposits at member banks up to $250,000 per depositor, per institution, per ownership category. When a bank fails, the FDIC steps in — depositors have never lost a single cent of FDIC-insured funds in the FDIC's 90+ year history.

Not every financial institution is FDIC-insured. Federal and state chartered banks, savings associations, and some online banks are. Credit unions have equivalent protection through the NCUA (National Credit Union Administration). Check the FDIC's BankFind tool or look for the FDIC logo before depositing.

**The $250K Limit — Per Depositor, Per Institution, Per Category**

The word 'category' is where this gets interesting. The FDIC distinguishes between ownership categories, and each category gets its own $250K coverage. The main categories:

— *Single accounts*: Accounts owned by one person, including all their single-owner accounts at that institution. Coverage: $250K total across all your single accounts at that bank.

— *Joint accounts*: Accounts owned by two or more people. Each co-owner gets $250K of coverage. A joint account for a couple = $500K total coverage at that institution.

— *Trust accounts (revocable trusts)*: This is the powerful one. Coverage is $250K per owner per unique beneficiary, up to $1.25M for five or more beneficiaries (if you have five or more unique benificaries named). A single person with a revocable trust naming five beneficiaries can have up to $1.25M insured at a single bank.

— *Retirement accounts (IRAs)*: Up to $250K per depositor per bank for IRA deposits, separate from your non-retirement deposits.

— *Business accounts*: Up to $250K for each entity, separate from the owner's personal deposits.

**A Practical Example**

Suppose you and your spouse have $1.5M in cash you want to keep fully insured at a single bank. How?

Option 1: Two single accounts + one joint account + two IRA accounts — Your single account: $250K — Spouse's single account: $250K — Joint account: $500K (=$250K x 2 owners) — Your IRA: $250K — Spouse's IRA: $250K — Total: $1.5M fully insured at one institution

Option 2: Revocable trust accounts — Your trust naming five beneficiaries: $1.25M — Spouse's trust naming five beneficiaries: $1.25M — That's $2.5M at one bank

If you have more than that, spread across multiple FDIC-insured institutions. Each one gets its own fresh $250K-per-category.

**Wealthfront and Betterment's Approach**

Wealthfront's Cash Account extends FDIC coverage up to $8 million by spreading your deposits across a network of partner banks, with each one carrying standard FDIC coverage for your slice of funds held there. You don't need to manage this — Wealthfront's program bank network does it automatically. Betterment Cash Reserve works similarly, providing up to $2 million in coverage. This is a legitimate and FDIC-recognized structure.

For people with large cash balances who don't want to manually manage multiple accounts across multiple banks, this is genuinely useful.

**CDARS and ICS Programs**

The Certificate of Deposit Account Registry Service (CDARS) and Insured Cash Sweep (ICS) are programs that your bank can participate in to automatically spread large deposits across multiple FDIC-member banks while you maintain a single banking relationship. If your bank offers this, it can be a cleaner solution than managing accounts at multiple banks yourself. Ask your bank if they participate.

**What FDIC Insurance Doesn't Cover**

FDIC insurance covers deposits — savings accounts, checking accounts, money market deposit accounts, CDs. It does not cover investments — stocks, bonds, mutual funds, ETFs, annuities. It doesn't cover losses from bad investment decisions. And it doesn't cover deposits above the limits. Know where your money is and how its protected.

**The SVB Lesson**

Silicon Valley Bank's collapse in March 2023 was a good stress test. Most SVB depositors were businesses with balances far above FDIC limits — exactly the scenario where you'd expect losses. The FDIC and Treasury ultimately guaranteed all deposits, above and beyond normal limits, but that was an exceptional intervention in an unusual situation. Don't bank on above-limit guarantees in future failures. Stay within insured limits or use the strategies above.

9Savings Accounts vs Alternatives — Where Does Cash Belong?

A savings account isn't always the right home for every dollar. Here's an honest comparison of your alternatives.

**Savings Accounts vs Certificates of Deposit (CDs)**

The basic trade: CDs offer a slightly higher rate in exchange for locking your money up for a fixed term.

Right now in March 2026, the best 1-year CDs are offering around 4.50-4.80% APY — maybe 0.70-1.00 percentage points above the best HYSAs. For money you genuinely won't need for 12 months, that premium is worth considering. For an emergency fund? Never put it in a CD — you need that money liquid.

The CD ladder strategy is worth knowing: instead of locking all your money in one CD, divide it across multiple CDs with staggered maturities — say, 3-month, 6-month, 9-month, and 12-month. As each one matures, you either spend the cash or roll it into a new CD at whatever rate is current. This gives you both a liquidity ladder and exposure to rate changes.

**Savings Accounts vs Treasury Bills**

T-bills are short-term US government debt — 4-week, 8-week, 13-week, 26-week, and 52-week maturities. Current rates are roughly 4.17-4.33% APY depending on the term. A few points:

— T-bill interest is exempt from state and local income taxes. For people in high-tax states (California, New York, New Jersey), this is significant. A T-bill yielding 4.25% might be worth 4.60-4.80% on an after-state-tax basis compared to a HYSA. — T-bills are backed by the full faith and credit of the US government — arguably the safest asset on earth, even safer than FDIC-insured deposits in theory. — You can't withdraw mid-term without selling on the secondary market, though the market is deep and liquid. — You buy them through TreasuryDirect.gov or a brokerage. There's more friction involved than opening a savings account.

For high earners in high-tax states with excess cash beyond the emergency fund, T-bills are genuinely competitive. Do the after-tax math for your situation.

**Savings Accounts vs Money Market Funds**

Money market funds are mutual funds that invest in very short-term, high-quality debt instruments — T-bills, commercial paper, repos. They aim to maintain a $1.00 net asset value and pay current short-term rates as a yield. Right now Vanguard's Federal Money Market Fund (VMFXX) is yielding around 4.00-4.30%.

Key differences from savings accounts: — Money market funds are NOT FDIC insured. There's been one instance of a fund 'breaking the buck' (NAV dropping below $1.00) in 2008 — the Reserve Primary Fund. The risk is theoretical but real. — Money market fund interest (if invested in Treasuries) may be partially state-tax-exempt. — You hold them in a brokerage account, which means they integrate naturally with an investment portfolio. — Slightly more yield in some cases than the best HYSAs.

For cash sitting in an investment account waiting to be deployed, a money market fund makes sense. For your emergency fund that you want in a simple, FDIC-insured, easily accessible account, a HYSA is cleaner.

**Savings Accounts vs I Bonds**

Series I Savings Bonds were an incredible deal in 2022 when they were paying 9.62% APY due to high inflation. That era is over. Current I bond rates are much lower — rates reset every six months based on CPI.

I bonds still have attractive properties: inflation protection, federal tax deferral (you don't pay federal taxes until you redeem), state and local tax exempt. But you can only buy $10,000 per year per person (plus up to $5,000 in tax refunds), and you can't redeem for 12 months. Early redemption before 5 years costs you 3 months of interest.

For most savers in 2026, the best HYSAs offer comparable or better rates to I bonds without the purchase limits and lock-up. I bonds make most sense for people who want the inflation hedge and plan to hold for several years.

**The Bottom Line on Alternatives**

Emergency fund: HYSA. Full stop. Liquid, insured, earns real interest.

Cash you won't need for 6-12 months: CD ladder or T-bills, depending on your tax situation.

Cash in an investment account: money market fund.

Inflation hedge with 1+ year horizon: I bonds, up to the $10K annual limit.

Medium-term savings (1-5 years): Combination of HYSAs and CDs.

10How to Actually Maximize Your Savings Returns

Strategy matters as much as account selection. Here's what actually moves the needle.

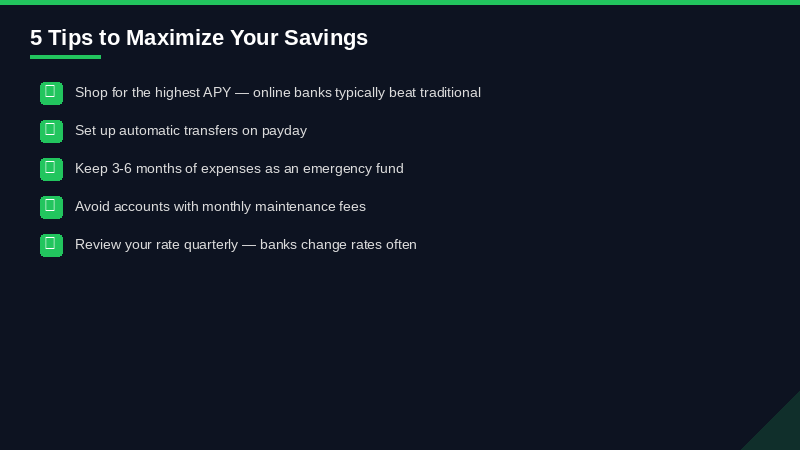

**Automate Everything**

The single most powerful savings habit isn't picking the right account — it's automating transfers before you can spend the money. Set up a recurring ACH transfer from checking to HYSA on payday. Even $200/month automated is more valuable than $500/month manual because the manual transfers always find an excuse not to happen.

Most HYSAs make this easy — Ally, Discover, Marcus all let you set scheduled recurring transfers. Set it, forget it, watch the balance grow.

**Rate Chasing — Worth It or Not?**

Rate chasing means moving your money when a competitor starts offering a higher rate. It's worth it at scale, but the math is nuanced.

On $10,000, the difference between 3.50% and 4.00% APY is $50/year. Is opening a new account worth $50? Maybe. On $100,000, the same rate difference is $500/year. Yes, absolutely.

But there are friction costs to chasing rates: — Opening a new account takes time. — Moving money takes 1-3 days and you earn nothing in transit. — Some banks have opening deposits or requirements. — You'll get a new 1099-INT at tax time from each institution.

My rule: if the rate differential is at least 0.50 percentage points and my balance is at least $20,000, the annual benefit justifies the switch. Below those thresholds, the friction isn't worth it. Your math may differ.

**The Multiple-Account Strategy**

Not everyone needs one account. There's a legitimate case for maintaining 2-4 savings accounts for different purposes:

— *Emergency fund account*: Keep 3-6 months of expenses here. Choose the highest-rate HYSA with no minimums and easy transfer mechanics. Never touch this unless it's a real emergency.

— *Short-term goals account*: Saving for a vacation, car, home renovation — money you'll spend in 1-2 years. Same type of account, just mentally earmarked differently. Ally's bucket system handles this elegantly within one account if you'd rather not manage multiple.

— *Down payment account*: If you're saving for a home purchase 2-5 years out, a mix of HYSA and CDs makes sense. The portion you need in 2 years goes in CDs. The rest stays liquid in HYSA.

— *Tax account*: If you're self-employed, keeping a dedicated savings account just for quarterly estimated taxes prevents the painful surprise of owing money you've already spent.

**Bonus-Rate Strategies**

Some banks offer referral bonuses or signup bonuses — $200-300 for opening an account and meeting deposit requirements. These are worth taking when available. Marcus and SoFi have both run these promotions. Check before you open.

Some banks also offer 'boosted' rates for linking to a checking account or investing account. Betterment, Wealthfront, and SoFi all have versions of this. If you're already using the ecosystem, it's essentially free money.

**Don't Let the Balance Stagnate**

Here's a thing that happens: you save diligently for a year, hit your emergency fund target, and then... keep saving into the same account until you have way more cash than you need in a HYSA. Three months of expenses should be the emergency fund. Anything beyond that is probably better put to work in investments unless you have specific near-term plans for it.

I've seen people with $80,000 in a savings account earning 4.00% APY when that money could be earning 7-10% long-term in index funds. The emergency fund deserves full liquidity and FDIC protection. The rest deserves to be invested. Savings accounts are a vehicle, not a destination.

11Savings Accounts for Specific Situations

The right savings account depends a lot on what you're saving for.

**Emergency Fund**

This is the foundational use case. Standard wisdom is 3-6 months of essential expenses — rent/mortgage, utilities, food, insurance, minimum debt payments. For people with variable income (freelancers, commission-based workers) or in industries with volatile employment, lean toward 6 months.

For an emergency fund, priority order is: 1. FDIC insured — non-negotiable 2. Liquid — transfers out in 1-3 days maximum 3. Earning real interest — HYSA at minimum 4. Separate from checking — so you're not accidentally spending it

Don't optimize an emergency fund for rate over liquidity. An extra 0.30% APY isn't worth it if accessing the money requires jumping through hoops.

Best picks: Ally (strong UX, zero friction), Discover (solid rate + service), Marcus (reliable).

**Down Payment Savings**

If your home purchase is 2-4 years out, this is where a CD ladder starts making sense alongside a HYSA. Keep 12-18 months of the target amount in a HYSA for liquidity, and put the rest in CDs maturing near your expected purchase date. You get a higher rate on the locked portion and liquidity on the rest.

Important: if the purchase timeline is uncertain, stay in HYSA. Nothing worse than paying a CD penalty because your closing date moved up.

**Kids' Savings Accounts**

For teaching kids about money, a dedicated savings account is excellent. Options:

— *Custodial accounts (UTMA/UGMA)*: You open and control the account until the child reaches majority (18-21 depending on state). Any interest earned is potentially taxable — the 'kiddie tax' rules apply. Standard HYSAs can be opened as custodial accounts at most banks.

— *529 plans*: Not a savings account but relevant — for college savings, these are better than a regular savings account because the growth is tax-free when used for qualified education expenses.

— *Kids-specific products*: Some banks (Ally, Chase, Capital One) offer kids accounts with parental controls. Rates are usually modest. The educational value outweighs the rate optimization at this stage.

**Business Savings Accounts**

Business savings accounts are separate legal entities from personal accounts. FDIC insures business deposits up to $250K per business entity, separate from your personal $250K.

Rates on business savings accounts are generally lower than personal HYSAs — it's an annoying market reality. Some online options: Relay Financial, Bluevine, Mercury, and Novo all offer competitive business checking with savings-like features. For businesses with significant cash reserves, a combination of a business HYSA and short-term T-bills through a brokerage often beats the straight business savings account rate.

**High-Balance Situations (Over $250K)**

If you've got more than $250K in cash — post-home sale, liquidity event, inheritance — FDIC strategy becomes critical. Options:

— Multiple institutions: Keep $250K or less per ownership category per bank. Yes, this means managing multiple accounts. — Wealthfront or Betterment: As discussed, these platforms provide multi-million dollar FDIC coverage automatically. — CDARS/ICS programs: If your bank offers it, they can handle the spreading automatically. — Treasury bills or money market funds: For amounts above what FDIC conveniently covers, government-backed instruments offer sovereign credit quality without the deposit limits.

**Recent Windfall**

Got a large unexpected sum — bonus, inheritance, legal settlement? Park it in a HYSA immediately while you figure out what to do with it. Earning 3.50-4.00% APY while you make a deliberate plan beats sitting in your checking account earning nothing. Take 3-6 months to decide. The money will earn a few hundred to a few thousand dollars during that decision window depending on amount.

Interest earned on savings accounts is taxable income.

12Tax Implications of Savings Account Interest

Interest earned on savings accounts is taxable income. Full stop. The IRS is not subtle about this.

**Federal Taxes**

Savings account interest is ordinary income — taxed at your marginal federal income tax rate, which ranges from 10% to 37% depending on your bracket. There's no special capital gains rate here, no preferential treatment. A dollar of savings account interest is taxed identically to a dollar of wage income.

This is an important number when comparing savings accounts to alternatives. A HYSA earning 4.00% APY for someone in the 32% federal bracket nets about 2.72% after federal tax. A T-bill earning 4.25% with state tax exemption for someone in California (9.3% state rate) nets roughly 3.31% after all taxes. The T-bill wins on after-tax basis even though the headline rate is higher on the HYSA.

Do your after-tax math. Don't compare pre-tax rates across taxable and partially tax-exempt instruments.

**The 1099-INT**

If you earned $10 or more in interest from a bank or other financial institution, you'll receive a Form 1099-INT by January 31 of the following year. Your bank sends a copy to the IRS simultaneously — so this isn't optional reporting, and the IRS will know if you don't include it on your return.

Less than $10 in interest? You technically still owe federal tax on it. You just won't get a 1099-INT. Report it on Schedule B of your Form 1040 anyway. Realistically, the IRS is unlikely to audit you over $3 in missing interest income, but it's the correct thing to do.

If you have accounts at multiple banks, you'll get multiple 1099-INTs. Keep them organized. They should all arrive by late January/early February.

**State Taxes**

Most states that have an income tax also tax savings account interest. A few exceptions and nuances: — Nine states have no income tax (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming — though some tax investment income specifically). — Tennessee and New Hampshire have historically taxed interest and dividends but not wages. Tennessee phased this out entirely. New Hampshire still taxes interest and dividends above certain thresholds. — State tax rates on interest income range from low single digits to over 13% (California's top rate).

If you're in a high-tax state, the state tax drag on savings account interest is significant and should factor into your comparison with T-bills (which are state-tax-exempt).

**FBAR and FATCA for Foreign Accounts**

This only applies to a tiny percentage of savers, but it's important if you're in it. If you have foreign bank accounts — either because you're an expat or because you've opened accounts at foreign institutions — you may have FBAR (FinCEN Form 114) and FATCA (Form 8938) filing obligations.

FBAR: If the aggregate value of all your foreign financial accounts exceeds $10,000 at any point during the year, you must file FinCEN 114 with the Treasury Department by April 15 (with extension to October 15). Penalties for willful non-filing are severe — up to $100,000 or 50% of account value per violation.

FATCA/Form 8938: Required if foreign financial assets exceed certain thresholds (starting at $50,000 for single filers). Filed with your regular tax return.

For most American savers keeping money in domestic FDIC-insured banks, none of this applies. It's worth mentioning because some fintech products route deposits through partner banks that people sometimes assume are foreign.

**Tax-Advantaged Alternatives**

If the tax drag on savings account interest bothers you, here are structures where savings grow more efficiently from a tax standpoint:

— *Health Savings Account (HSA)*: Contributions pre-tax, growth tax-free, withdrawals tax-free for medical expenses. The ultimate tax-advantaged savings vehicle if you have a qualifying high-deductible health plan. — *529 plans*: Growth tax-free for qualified education expenses. — *Roth IRA*: Contributions after-tax but growth and qualified withdrawals are tax-free. Some people hold their IRA cash in a savings-like vehicle within a Roth IRA while deciding how to invest. — *I Bonds*: Federal tax deferred until redemption; state and local tax exempt.

For emergency fund purposes, you accept the tax drag because liquidity is non-negotiable. For longer-term savings where you have flexibility, tax-advantaged wrappers significantly improve your net return over time.

13How Interest Rates Are Set — The Full Pipeline

Understanding why your HYSA rate moved last week requires understanding the chain that connects monetary policy to your savings account balance.

**The Federal Reserve and the Federal Funds Rate**

The Federal Reserve — specifically the Federal Open Market Committee (FOMC) — sets the target range for the federal funds rate. This is the rate at which banks lend money to each other overnight to meet reserve requirements. The FOMC meets eight times per year and can hold, raise, or cut this rate based on their dual mandate: maximum employment and stable prices (2% inflation target).

As of January 28, 2026, the federal funds rate sits at 3.50-3.75%. It was 5.25-5.50% at the 2023 peak. The three cuts in late 2024 brought it down. Markets are pricing in maybe one or two more cuts in 2026, with Goldman Sachs projecting June and September as the most likely dates.

Here's the crucial point: the federal funds rate is an overnight rate. Banks don't necessarily pass every single basis point of movement directly to their savings account customers — but it's the primary input.

**How the Rate Gets to Your Account**

When the Fed raises rates, it becomes more expensive for banks to borrow money. To attract deposits as an alternative funding source, they raise savings rates. When the Fed cuts, the cost of borrowing falls, competition for retail deposits decreases, and savings rates drift down.

The pass-through isn't immediate or mechanical. Banks have discretion. Big banks with large, sticky deposit bases can afford to lag — their depositors won't leave for an extra 25 basis points. Online banks with rate-sensitive deposit bases have to be more responsive.

This is exactly what happened in 2022-2023. The Fed hiked 525 basis points. Big banks barely moved their savings rates — maybe from 0.01% to 0.10-0.25%. Online banks went from 0.50% to 4.50-5.00%+. The divergence was historic. Now that the Fed is cutting, online bank rates have drifted down, but they're still dramatically higher than big bank rates.

**The SOFR Connection**

Banks also use the Secured Overnight Financing Rate (SOFR) — the rate on overnight Treasury repo transactions — as a benchmark for many financial products. SOFR closely tracks the federal funds rate. When you see money market fund yields and HYSA rates move in lockstep with SOFR/fed funds, that's the mechanism.

**Deposit Competition**

Beyond the Fed, bank-specific factors affect your rate:

— *How much does the bank need deposits?* A bank growing its loan book aggressively needs to fund those loans. They'll pay up for deposits. A bank with excess liquidity has less incentive to pay competitively.

— *What are competitors paying?* Online banks track each other's rates closely. When SoFi raises their rate, Ally faces pressure to respond.

— *What's the bank's profit spread?* Banks earn the spread between what they pay depositors and what they charge borrowers. When credit spreads compress or loan demand drops, they can afford to pay less on deposits.

**What This Means Practically for 2026**

If the Fed cuts twice more in 2026 as projected — each cut 25 basis points — that's 50 more basis points of cuts. The best HYSA rates would likely drift from ~4.00% today to ~3.50% by year-end in a two-cut scenario.

That's still very good. Not 2022-level embarrassing for cash holders, but not the 5.00%+ peak either.

The argument for opening a CD or T-bill position now is essentially a bet that rates will fall. If you can lock in 4.50% for 12 months on a portion of your savings, you're insulated from the drift downward. If the Fed surprises and holds or hikes, you'll have locked in a rate slightly below where things end up. That's the tradeoff.

For most people: keep emergency fund in HYSA (accept the rate variability because you need the liquidity), consider laddering some of your non-emergency savings into CDs if you believe the rate-cut scenario.

14Red Flags and What to Avoid

Not every savings account is worth your time or your money. Here are the things that should make you pause.

**Teaser Rates**

Some banks — and this happens more than people realize — advertise a headline rate that's only available for the first 3-6 months, then drops sharply. CIT Bank has played this game. So have some credit unions.

Always ask: is this the ongoing rate or an introductory rate? Read the APY disclosure, not just the marketing copy. Look for language like 'introductory APY,' 'promotional rate,' or 'rate valid for X months.' If you can't find a clear answer on the bank's site, call them and ask directly.

A bank offering 5.00% for 3 months before dropping to 2.50% permanently is actually offering you a 12-month blended rate of about 3.12% — which isn't special.

**Tiered Rates That Punish Normal Balances**

Some accounts advertise high rates but only for balances in specific tiers — sometimes the higher rate applies only to higher balances (straightforward), but occasionally it works backward. Some accounts earn a high rate on the first $10,000 and a dramatically lower rate on balances above that. Read the full rate schedule before depositing large amounts.

**Excessive Conditions**

Multiple conditions stacked to earn a competitive rate is a yield trap. Varo's 5.00% requiring direct deposit is reasonable — one condition, easy to meet if you have a job. But some accounts stack conditions: direct deposit plus minimum number of debit card transactions per month plus maintaining a minimum balance plus logging into the app. Each condition is a gotcha that drops you to a much lower rate when you miss one month.

Count the conditions. One condition, fine. Two conditions, acceptable. Three or more conditions, look elsewhere.

**Fintech Charter Risk**

Some fintech apps look exactly like banks but aren't. They're apps with banking-as-a-service backends — they partner with chartered banks that hold the actual deposits. Usually this is fine and the FDIC coverage flows through the partner bank. But there have been failures in this model.

In 2024, Synapse Financial — a banking middleware company — collapsed, and users of fintech apps that relied on Synapse (including Yotta and others) found themselves unable to access funds for months while regulators sorted out who owed what. The FDIC insurance was theoretically there, but the accounting mess meant it took months to resolve.

The lesson: verify that your savings account is directly at an FDIC-insured bank, not just routing through one via middleware. For major established banks — Ally, Marcus, Discover, Synchrony, Barclays — this is not a concern. For newer fintech apps with consumer-friendly UIs and high advertised rates, verify the FDIC chain carefully.

**Variable Rates That Can Move Instantly**

This isn't exactly a red flag but it's important to internalize: HYSA rates are variable and can change at any time. There's no lock-in. Ally dropped from 4.35% to 3.20% over the course of a year. Marcus moved down steadily. The bank is not obligated to notify you a certain number of days in advance of a rate cut (though many do send email notifications).

If rate certainty matters for your financial planning, CDs or T-bills are more appropriate. If you choose HYSAs, just know that you need to periodically check whether your rate is still competitive.

**Account Minimums Hidden in Fee Schedules**

Some banks have separate minimum balance requirements to earn the advertised APY versus minimum balance to avoid a monthly fee versus minimum to open. These can be three different numbers. I've seen accounts where you need $2,500 minimum to earn the advertised rate, $500 minimum to avoid a $5/month fee, and $25 to open. None of those three numbers match the others. Read the full account disclosure, not just the rate advertised on the landing page.

**Obscure Banks Offering Dramatically Higher Rates**

When an account offers rates significantly above everything else — say 6.00% or 7.00% APY on a savings account when the market is 4.00% — it's worth asking why. Either the bank is desperately trying to attract deposits (could indicate financial stress), the rate is heavily conditioned (tiered, introductory, or conditional), or something else is going on.

I'm not saying never take a higher rate from a smaller bank — Newtek Bank was legitimately offering 4.20% and is backed by real assets. But don't chase a 7% savings rate without understanding exactly why that's possible and whether the institution is sound. Check the bank's FDIC status, look up their call report data, read recent news about them.

15Calculator Examples — Real Math on Your Money

Numbers help. Here are worked examples for the most common scenarios.

**Example 1: The Cost of Staying at a Big Bank**

Balance: $25,000 Big bank rate: 0.01% APY Best HYSA rate: 3.90% APY (Amex)

Big bank after 1 year: $25,002.50 (you earned $2.50) HYSA after 1 year: $25,978.12 (you earned $978.12)

Annual opportunity cost: $975.62. That's roughly a round-trip flight to Europe or five car payments.

After 3 years (assuming rate holds): Big bank: $25,007.50 HYSA: $28,006.15

You left $2,998.65 on the table over three years. That's a used car down payment.

**Example 2: Varo vs Ally for a $5,000 Balance**

Varo: 5.00% APY on first $5,000 Ally: 3.20% APY

Varo after 1 year: $5,255.81 Ally after 1 year: $5,161.53

Difference: $94.28/year. Decent. Easy math for $5K.

**Example 3: Varo vs Wealthfront for $50,000**

Varo: 5.00% on $5,000, 2.50% on remaining $45,000 — blended ~2.67% Wealthfront: 4.00% on full $50,000

Varo after 1 year: $51,347 (approx) Wealthfront after 1 year: $52,040 (approx)

Wealthfront wins by ~$693/year on $50,000. This is why blended rate math matters when considering conditional high-rate accounts.

**Example 4: HYSA vs CD Trade-off**

Balance: $20,000 HYSA rate: 4.00% APY (variable) Best 12-month CD: 4.60% APY (fixed)

HYSA after 12 months: $20,816 12-month CD after maturity: $20,936

CD advantage: $120 — is that worth giving up 12 months of liquidity? If the money is absolutely not needed for 12 months, probably yes. If there's any chance you'll need it, no.

Alternatively, if the Fed cuts 50 basis points and your HYSA drops to 3.50% over the course of the year: Actual HYSA return (average 3.75%): $20,757 CD return (still locked at 4.60%): $20,936

CD advantage grows to $179. The cut scenario makes the CD more attractive in retrospect.

**Example 5: Compounding Frequency Doesn't Matter as Much as You Think**

Daily vs monthly compounding on $10,000 at 4.00% APY: — Daily compounding: $10,407.44 — Monthly compounding: $10,407.00

Difference: $0.44. Basically irrelevant. Banks advertise daily compounding like it's a feature because it sounds impressive. It's real but the practical difference is cents, not dollars. Don't factor this into your account decision.

**Example 6: The Emergency Fund Sweet Spot**

Monthly expenses: $4,500 (rent, food, utilities, insurance, minimums) 3-month emergency fund target: $13,500 6-month emergency fund target: $27,000

$13,500 in a 4.00% HYSA earns $556/year. $27,000 in a 4.00% HYSA earns $1,113/year.

That's real money just sitting there, fully liquid, fully insured, doing its job. The emergency fund isn't a sacrifice — it's money earning ~4% while also being available if your car breaks down or you lose your job.