1Where Mortgage Rates Actually Stand Right Now

Let's just start with the number everyone wants: the 30-year fixed rate is sitting at 6.11% as of March 12, 2026, according to Freddie Mac's Primary Mortgage Market Survey. That's up from 6.00% the week before — but down more than half a point from where we were a year ago, when the 30-year averaged 6.65%.

The 15-year fixed? 5.50%. And the 5/1 ARM is bouncing around 5.56% nationally, though some lenders are quoting closer to 5.47% depending on your profile.

Here's the thing nobody tells you upfront: those are averages. Freddie Mac collects that data from thousands of loan applications, which means it's a real market rate — not some teaser rate a lender plastered on a billboard. Your actual rate will be higher or lower based on your credit score, down payment, loan type, property type, and which lender you call. A borrower with an 800 credit score putting 20% down is gonna see something meaningfully better than those averages. Someone with a 640 score and 5% down? Budget higher.

And yeah — spring homebuying season is in full swing. Existing-home sales jumped 1.7% in February, purchase applications ticked up this week. The market's alive. People who sat out the 7%-plus era of 2023-2024 are starting to move.

So what's actually driving rates right now? Mostly the 10-year Treasury yield, which mortgage rates have always tracked closely. Inflation data, Fed policy signals, and labor market strength all feed into that yield. The Fed hasn't cut rates dramatically — they've been cautious — but the trend has been downward from the peak. Nobody credible is forecasting a return to 3% rates. The realistic bull case if inflation cooperates is maybe high 5s by late 2026. Maybe. Don't plan your life around it.

What this means practically: if you're waiting for rates to get 'good enough' to buy, you might be waiting a long time. The math often works better than people think even at 6%, especially with rents still elevated in most metros.

One more thing on rate context before we move on. The spread between the 30-year mortgage rate and the 10-year Treasury has been historically wide — around 250-270 basis points vs. a historical average closer to 170 bps. Why does that matter to you? Because as the mortgage market normalizes and lenders get less risk-averse, there's a structural argument for rates to drift down even without Fed action. Or they don't. Honestly, predicting rates is a fool's game. Buy when the math works, not when the forecast says to.

2Mortgage Types: Which Loan Actually Fits Your Situation

There are five main mortgage types and every one of them has a specific use case. Getting this wrong is one of the most expensive mistakes homebuyers make — not because the loan terms are catastrophically different but because a mismatch costs you money in fees, rate, or flexibility for years.

**Conventional Loans**

This is the default. No government backing, sold to Fannie Mae or Freddie Mac in the secondary market, conforming loan limit in 2026 is $766,550 in most of the country (higher in expensive markets). You need at minimum a 620 credit score though realistically lenders want 660+ for decent pricing. Down payment can be as low as 3% (Fannie's HomeReady or Freddie's Home Possible programs) but expect PMI until you hit 20% equity.

Best for: borrowers with good credit (680+), stable income, who want flexibility on property type and loan terms. If your credit and income are solid, conventional is almost always cheaper long-term than FHA because you can drop PMI.

**FHA Loans**

Federal Housing Administration backing means lenders take less risk — so they'll accept lower credit scores and smaller down payments. The 2026 FHA loan limits run from roughly $541,287 in low-cost areas up to $1,249,125 in high-cost regions like San Francisco and New York.

Here's the requirement breakdown: - Credit score 580+: 3.5% down - Credit score 500-579: 10% down (and good luck finding a lender) - Must be primary residence - Debt-to-income ratio generally needs to be under 43% (some exceptions up to 50% with compensating factors)

The catch — and it's a real one — is mortgage insurance. You pay 1.75% upfront MIP (usually rolled into the loan) plus an annual MIP between 0.55% and 0.85% depending on loan term and LTV. And unlike conventional PMI, FHA MIP doesn't automatically go away at 20% equity if you put less than 10% down. You're stuck with it for the life of the loan. That can add tens of thousands of dollars over a 30-year term.

Best for: first-time buyers with credit challenges, anyone below 620, situations where 3.5% is the difference between buying and not buying. Just do the math on long-term MIP cost vs. waiting to improve your credit score and go conventional.

**VA Loans**

Honestly the best loan product in existence if you qualify. Zero down. No PMI. Competitive rates. The VA doesn't set a loan limit for borrowers with full entitlement anymore (though lenders still apply their own caps for jumbo VA). You do pay a one-time VA funding fee — 2.15% for first use with 0% down, less if you put money down — but that's it. No monthly mortgage insurance ever.

Requirements: active duty military, veterans, National Guard/Reserve members with qualifying service, and surviving spouses in some cases. You'll need a Certificate of Eligibility. Credit score minimums are set by individual lenders — VA doesn't mandate one, but most lenders want 620 minimum, preferably 640+.

Best for: any eligible veteran or service member, full stop. There's almost no scenario where a VA loan isn't the best option for a qualifying borrower.

**USDA Loans**

Another 0% down option — but with geographic and income restrictions most people don't realize are more flexible than the name implies. 'Rural' in USDA's definition includes a lot of small towns and suburbs. About 97% of U.S. land mass qualifies. Income limits are tied to your county's median income — typically you can't earn more than 115% of the area median.

USDA has a 1% guarantee fee (upfront, usually rolled in) and a 0.35% annual fee. That annual fee is lower than FHA MIP. Credit scores: most lenders want 640+ though the program technically allows lower.

Best for: moderate-income buyers who want zero down and are buying outside of major urban cores. Fantastic deal if you qualify.

**Jumbo Loans**

Anything above the conforming loan limit ($766,550 in most areas, up to $1,149,825 in high-cost counties) is a jumbo loan. These don't conform to Fannie/Freddie standards so lenders hold them on their own books or sell to private investors — which means stricter requirements.

Typically you'll need: - 700+ credit score (720+ for better rates) - 10-20% down minimum, most lenders want 20% - Cash reserves of 6-12 months of payments - Lower DTI — often 43% max, some lenders want 38% - Full documentation income

Rates on jumbos are sometimes actually close to or even below conforming rates because you're dealing with high-income, low-risk borrowers with substantial assets. But the qualification bar is genuinely higher. No shortcuts here.

Best for: buyers in high-cost markets who need loan amounts above the conforming limit and can document strong financial profiles.

3Fixed vs. Adjustable Rate: The Math Most People Skip

The 30-year fixed at 6.11% vs. a 5/1 ARM at 5.56%. That's a 55 basis point gap right now. On a $400,000 loan that's roughly $145 per month cheaper on the ARM payment. Sounds good. Is it?

Depends entirely on two things: how long you plan to stay, and where rates go after the initial fixed period.

Let's run the actual math. $400,000 loan amount.

30-year fixed at 6.11%: monthly payment ~$2,432 (principal + interest) 5/1 ARM at 5.56%: monthly payment ~$2,290 for the first 5 years

Difference: $142/month, or $1,704/year, or $8,520 over 5 years.

So after 5 years the ARM has saved you $8,520. But here's what happens at year 6 — the rate adjusts. 5/1 ARMs are typically tied to the SOFR index plus a margin (usually 2.5-3.5%). After the initial period, they adjust annually with caps: 2% per adjustment, 5% lifetime cap over the start rate.

Worst case scenario: your 5.56% ARM hits the 5% lifetime cap and becomes 10.56%. Monthly payment on your remaining balance (roughly $375K at year 5) shoots to ~$3,500. That's $1,068 more than the fixed rate payment you gave up. You'd erase the entire $8,520 savings in about 8 months of elevated payments.

Break-even logic for fixed vs. ARM: Add up the savings in the fixed period. Divide by the maximum possible payment increase per month after adjustment. That gives you your 'buffer months' — how long rates would have to be elevated before you lose money on the ARM. If you're confident you're selling or refinancing before or shortly after the fixed period ends, the ARM math is favorable. If you might be in the house long-term? The 30-year fixed is boring, predictable, and genuinely the right call.

One scenario where ARMs absolutely make sense: you know you're relocating in 3-4 years. Or you're buying a property as a bridge to something bigger. Or you expect rates to drop significantly and plan to refinance. All legitimate.

The scenario where ARMs destroy people: you convince yourself 'rates will be lower in 5 years' and they're not. Or life happens and you can't sell when you planned. Or the payment shock hits a budget that had no cushion.

My honest take: at 6.11% on the 30-year, the extra 55 bps you're paying over the ARM for certainty is cheap insurance. But I'm not you. Run your specific numbers.

Beyond the 5/1 ARM, you've got 7/1 and 10/1 ARMs. The 7/1 gives you seven years of fixed rate — on a $400K loan at 5/1 pricing you're often looking at 5.70-5.85% for a 7/1, narrowing the savings vs. fixed considerably. And the 10/1 ARM is almost a philosophical product — 10 years is a long time, and the rate difference vs. a 30-year fixed is usually only 20-30 bps. Not worth the complexity unless you have a specific reason.

Also worth knowing: 15-year fixed at 5.50% right now. Monthly payment on a $400K loan is ~$3,270 vs. ~$2,432 for the 30-year. You're paying $838 more per month but you'll own the house free and clear 15 years earlier and pay dramatically less interest. Total interest on the 30-year at 6.11%: roughly $475,000. Total interest on the 15-year at 5.50%: roughly $189,000. That's a $286,000 difference. If your cash flow can handle the higher payment, the 15-year is one of the best financial moves available.

People treat the mortgage process like a black box.

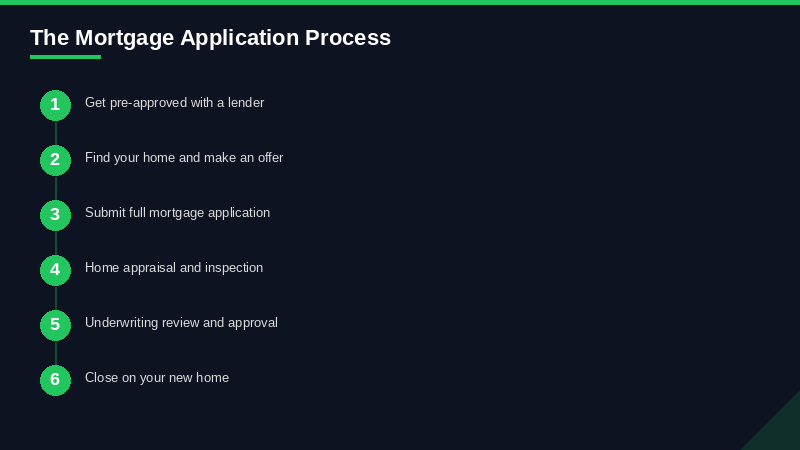

4The Mortgage Process from Start to Keys in Your Hand

People treat the mortgage process like a black box. It doesn't have to be. Here's what's actually happening at each stage.

**Step 1: Get Your Financial House in Order (Do This First)**

Before you talk to a single lender, pull your free credit reports from annualcreditreport.com — all three bureaus, Equifax, Experian, and TransUnion. Look for errors. Dispute anything wrong immediately because fixing credit reporting errors can take 30-60 days. Also check your FICO mortgage score specifically (banks use FICO 2, 4, and 5 — different from the score on your credit card app).

Get your documents together now because the underwriter is going to want all of this anyway: - 2 years tax returns (personal + business if self-employed) - 2 months bank statements (all pages) - 2 most recent pay stubs - W-2s from past 2 years - Investment/retirement account statements - Landlord contact info and rental payment history if applicable

**Step 2: Pre-Approval (Not Pre-Qualification — There's a Difference)**

Pre-qualification is basically a lender looking at numbers you tell them and saying 'sounds good.' It means almost nothing. Pre-approval is a real credit pull, document review, and a conditional commitment from an underwriter. Sellers and their agents know the difference.

Apply for pre-approval before you start seriously looking at houses. The hard inquiry on your credit is only one point or two — don't let that stop you. Multiple mortgage inquiries within a 14-day window count as a single inquiry under FICO scoring models, so don't hold back on applying with multiple lenders simultaneously.

Pre-approval letters are typically good for 60-90 days. If your house hunt runs longer than that, you'll need to refresh.

**Step 3: House Hunting (with a budget you actually know)**

You know your pre-approval limit. This is your ceiling, not your target. There's often significant daylight between what you can technically borrow and what makes sense to borrow. More on the affordability math in the next section. Work with a buyer's agent who understands mortgage constraints — they'll help you filter for realistic options and not waste your time on properties at the edge of your range.

While shopping, get the inspection contingency in your offer. Non-negotiable for most buyers unless you're in an absolute warzone market and you've accepted the risk. Mortgage contingency too.

**Step 4: Loan Application**

Once your offer is accepted, you have a deadline — usually 30-45 days to closing. You go back to your lender and submit the formal application. They send you a Loan Estimate within 3 business days. Read every line. Compare across multiple lenders if you haven't locked yet.

Something people screw up here: don't make any large financial moves after going under contract. No new credit cards, no big purchases, no job changes, no moving cash around without documentation. The underwriter is going to re-verify your employment and pull credit again right before closing.

**Step 5: Appraisal**

The lender orders an appraisal — a licensed appraiser visits the property and confirms it's worth at least what you're paying. If the appraisal comes in low, you've got options: negotiate the price down, pay the gap in cash, challenge the appraisal with comps, or walk if the contract allows. Low appraisals kill deals. It happens more in hot markets where prices are moving faster than comparable sales data.

**Step 6: Underwriting**

This is where it can feel slow and frustrating. An underwriter (human, not just software) reviews your entire file and determines whether you meet lending guidelines. They will ask for more documents. Respond immediately — every day you delay is a day closer to your rate lock expiration and closing deadline.

Common underwriting requests: letters of explanation for deposits, employment gaps, credit inquiries, or account transfers. Keep copies of everything.

You'll eventually get one of three outcomes: approved, approved with conditions (most common — just submit whatever they ask for), or denied. Denial at underwriting is rough but not the end — it usually tells you what to fix.

**Step 7: Closing Disclosure and Final Walkthrough**

Three business days before closing you receive the Closing Disclosure — final version of all your costs. Compare it line-by-line with your Loan Estimate. Fees can change; some can't. If a lender suddenly inflated a fee, push back. You have the right to ask.

Do your final walkthrough 24 hours before closing. Confirm nothing changed about the property, agreed-upon repairs were made, everything that was supposed to stay is still there.

**Step 8: Closing**

You show up (or sign remotely in many states), sign approximately 100 pages of documents, wire your down payment and closing costs, and get keys. Wiring instructions: CALL THE TITLE COMPANY directly to verify before sending any wire. Wire fraud targeting home buyers is rampant. Do not trust emailed wire instructions without a verbal confirmation.

The whole process from offer acceptance to closing typically takes 30-45 days with a cooperative seller, clean title, and smooth underwriting. Cash buyers can close faster. Complex loans, title issues, or condo purchases with HOA financials can take longer.

5How Much House Can You Actually Afford

The bank will tell you how much they'll lend. That's a ceiling, not a recommendation. Let's talk about what actually makes sense.

**The 28/36 Rule**

This is a decades-old guideline that still holds up reasonably well. The rule says: - Your housing costs (PITI — principal, interest, taxes, insurance) shouldn't exceed 28% of your gross monthly income - Your total debt payments (housing + all other debt: car, student loans, credit cards) shouldn't exceed 36% of gross monthly income

Some lenders have pushed this to 43% total DTI, and FHA goes up to 50% with compensating factors. But just because you can qualify for 43% DTI doesn't mean 43% DTI is comfortable.

**Real Scenarios at Different Income Levels**

Household income $75,000/year ($6,250/month gross): - 28% front-end: $1,750 max housing payment - At 6.11% on 30-year fixed, with 20% down, $1,750 P&I supports roughly a $270,000 loan — so ~$337,000 home price - Property taxes + insurance typically add $400-700/month depending on location, so your P&I budget shrinks to $1,100-1,350 - Realistic purchase price: $200,000-$230,000 in most markets - At 36% total DTI with $400/month car payment: even less room

Household income $120,000/year ($10,000/month gross): - 28% front-end: $2,800 max housing payment - Subtract taxes/insurance: P&I budget around $2,100-2,400 - Supports roughly a $380,000-$435,000 loan - With 10% down: homes in the $420,000-$480,000 range - This is a common 'comfortable professional couple' scenario in mid-tier metros

Household income $200,000/year ($16,667/month gross): - 28% rule: $4,667 max housing payment - P&I budget after taxes/insurance: $3,800-4,100 - Supports roughly $630,000-$680,000 loan - With 20% down: homes up to $850,000 - At this income level you can often stretch — but watch lifestyle creep eating the budget elsewhere

**DTI Math That Actually Matters**

Lenders calculate DTI using minimum monthly debt payments. Not what you actually pay — the minimum. So if you have $10,000 in credit card debt, the payment they're counting is the minimum (maybe $200-250) not what you're aggressively paying.

Student loans get complex. If you're on income-based repayment with a $0 payment, some lenders use 0.5-1% of the outstanding balance instead. That can kill a deal when you have $150,000 in student loans — suddenly you've got a $750-1,500/month 'payment' counted even though you're paying $0 currently.

**The Other Costs People Forget**

Mortgage payment is not the full cost of homeownership. Budget separately for: - Property taxes: $3,000-$12,000+/year depending on location and assessed value - Homeowners insurance: $1,200-$3,000/year for most single-family homes - HOA fees: $100-$700+/month if applicable (condos, planned communities) - Maintenance: the old rule is 1-2% of home value annually. On a $400K house that's $4,000-$8,000/year for the boiler that dies, the roof that needs work, the HVAC that goes out - Utilities: harder to estimate but factor in before buying a house twice the size of your current place

A real honest-to-god affordable payment is one where you can make it, cover all the above, contribute to retirement, and still not have anxiety when the check engine light comes on. If the mortgage payment alone maxes out 28% of gross but you have no margin elsewhere, you're house poor — even if the lender approved you at 43% DTI.

6Down Payment Strategies: From 3% to 20% and Everything Between

How much you put down shapes your monthly payment, your PMI situation, your rate, and sometimes whether you even get the loan. Let's actually work through the numbers at different levels.

**The 3% Down Option**

Conventional 3% down exists via Fannie Mae's HomeReady and Freddie Mac's Home Possible programs. These are for first-time buyers (or buyers who haven't owned in 3 years) with income at or below the area median.

On a $350,000 home: - Down payment: $10,500 - Loan amount: $339,500 - At 6.11%: P&I payment ~$2,062 - PMI: approximately 0.75-1.25% of loan annually = $212-$354/month - Total housing payment before taxes/insurance: $2,274-$2,416

The PMI hit is real. And at 3% down your equity position is essentially zero after closing costs — you'd actually be slightly underwater on day one if you factor in what it would cost to sell. That's fine if you're committed to staying. Not fine if you might need to move in 2 years.

**The 5-10% Down Zone**

More common for repeat buyers or first-timers with some savings. PMI is still in play but the rate is lower (less risk to the lender). On the same $350,000 home:

5% down ($17,500): Loan $332,500, PMI roughly 0.65-0.90%/year = $180-$249/month 10% down ($35,000): Loan $315,000, PMI roughly 0.40-0.65%/year = $105-$170/month

Big jump in PMI between 5% and 10%. Worth running the math on how long it takes the PMI savings to offset keeping more cash. Generally: if you'd earn more than the PMI cost in investment returns on that cash, keep the cash and put less down. If you'd earn less, put more down.

**The 20% Down: The PMI Killer**

Every dollar you put toward that 20% threshold eliminates PMI. On a $350,000 home, 20% is $70,000. That's a big number. But it buys you: - No PMI (saves $100-350+/month depending on loan amount) - Better rate (usually 0.125-0.25% lower) - More negotiating power as a buyer (stronger offers) - Immediate positive equity cushion

The counterargument: that $70,000 invested in an index fund at historic average returns beats the PMI cost in many scenarios. True. But it ignores the behavioral finance reality that most people don't invest the difference, and the risk-adjusted value of owning a house outright (or nearly so) is real.

**PMI Math: What It Actually Costs You**

PMI rates depend on your credit score, LTV, and loan type. Rough ranges in 2026: - 95% LTV (5% down), 720+ credit: 0.65%/year - 95% LTV, 680 credit: 1.00-1.10%/year - 90% LTV (10% down), 720+ credit: 0.40%/year - 90% LTV, 680 credit: 0.60-0.80%/year

On a $315,000 loan at 0.65% PMI: $170/month = $2,040/year. Until you hit 20% equity at which point you can (and should, immediately) request cancellation. PMI automatically terminates at 22% equity under the Homeowners Protection Act.

How long to reach 20% equity from 10% down on a $350,000 home? With a 30-year fixed at 6.11%, you'll cross the 80% LTV threshold (20% equity based on original value, ignoring appreciation) in roughly 10-11 years through amortization alone. With even modest appreciation you get there much faster.

**Down Payment Assistance Programs**

This section is wildly underutilized. Every state has DPA programs and many counties and cities do too. Some highlights:

- State HFAs (Housing Finance Agencies): Many offer 0-3% second mortgages for down payment, some forgivable after 3-5 years of residency - Chenoa Fund: Up to 3.5% DPA for FHA loans nationwide, repayable second mortgage - Bank programs: Chase offers up to $5,000 in grants for buyers purchasing in certain communities. Bank of America has similar programs - USDA and VA: zero down by design — that's already your assistance

To find DPA programs in your area: HUD maintains a free database at hud.gov/buying/localbuying. Also check your state's housing finance agency directly. Income limits apply to most programs and they're not always advertised by lenders who'd rather sell you a bigger loan.

**Lender-Paid PMI (LPMI): The Trade You Don't See**

Some lenders offer to 'pay' your PMI — but they don't pay it, they just roll the cost into a higher interest rate. This might make sense if: - You plan to sell or refinance within a few years (before the higher rate adds up to more than PMI would have cost) - You can't deduct PMI but can deduct mortgage interest (the tax situation changed in 2018 but check current rules) - The rate bump is small and your loan amount is modest

Do the math. If LPMI adds 0.375% to your rate on a $300,000 loan, that's about $94/month in perpetuity vs. PMI that disappears at 20% equity. If you hit 20% equity in 5 years, LPMI cost you $5,640 more than just paying PMI.

7Closing Costs: Every Fee Explained and What You Can Actually Negotiate

Average closing costs on a purchase in 2026 run roughly $6,900 on a $350,000 home — but that's excluding prepaids and varies wildly by state. In Washington D.C. you're looking at $17,545 average. Missouri averages $1,740. On larger loans in expensive states with attorney requirements, $12,000-$15,000 is very real.

Here's what you're actually paying for:

**Lender Fees (Most Negotiable)**

Origination fee: 0.5-1.0% of loan amount. This is the lender's cut for making the loan. On a $400,000 loan that's $2,000-$4,000. This is directly negotiable — especially if you have competing offers from other lenders. Say 'Lender B offered me 0.5% origination, can you match that?' It works more often than you'd think.

Application fee: $0-$500. Some lenders charge it, some don't. If a lender is charging $500 to take your application, that's a yellow flag — good lenders often waive this or credit it back at closing.

Processing fee: $300-$900. Covers the cost of putting your file together and managing the process. Legitimate cost, but also negotiable as part of a total fee package.

Underwriting fee: $400-$900. The actual review of your file. Less negotiable but not immune to pushback in a competitive situation.

**Third-Party Fees (Less Negotiable, But You Can Shop)**

Appraisal: $350-$750 for a single-family home. The lender orders this but you pay it (usually upfront before closing). You cannot choose the appraiser — it's assigned by an AMC (appraisal management company). But if the fee seems high you can ask if the lender can order from a different AMC.

Title search: $150-$400. A search of public records to confirm the seller can legally convey the property. Required.

Title insurance (lender's policy): $500-$1,500 depending on loan amount. Required by virtually all lenders. Protects the lender from undiscovered title claims. You can shop for title insurance in most states — rates are regulated but companies vary.

Title insurance (owner's policy): Optional but strongly recommended. Protects you if a claim surfaces after closing — mechanic's lien from work done before you bought, an heir nobody knew about, a forged deed in the chain of title. Usually $500-$1,000. Well worth it. Get it.

Survey: $200-$700 if required. Not always needed, especially if the previous survey is recent and the property hasn't changed.

Pest inspection: $75-$200. Required by VA and USDA. Optional but recommended on older homes.

Credit report fee: $25-$75. Whatever it costs the lender to pull your tri-merge credit report.

**Government Fees (Non-Negotiable)**

Recording fees: $50-$250. County charges to record the deed and mortgage in public records.

Transfer taxes: Varies enormously. Some states have no transfer tax. New York City has some of the highest — can be 1.4-2.075% of purchase price. Know your state's rules before you're surprised at the closing table.

**Prepaids (Not Really 'Closing Costs' But Still Cash Out of Pocket)**

These aren't fees for services — they're things you're paying in advance:

Homeowners insurance: First year premium paid at or before closing. $1,200-$2,500/year for most single-family homes.

Property taxes: 2-6 months prepaid into escrow. If your monthly taxes are $600 and the lender wants 3 months, that's $1,800 at closing.

Prepaid interest: Per diem interest from closing date to the end of the month. If you close on the 5th of the month, you're paying 25 days of interest upfront (~$60-90/day on a $400,000 loan at 6.11%). Pro tip: closing at the end of the month minimizes this amount.

**What You Can Actually Negotiate**

Lender fees are the main targets. Lenders have margin built into origination, processing, and sometimes underwriting. Competing loan estimates side by side and asking for a match is the single most effective tactic.

Seller concessions: In a buyer's market (or at least a balanced market), you can ask the seller to pay some or all of your closing costs. This is rolled into the offer negotiation. VA and FHA allow up to 4-6% seller concessions. Conventional allows 3-9% depending on LTV. This can save you $5,000-$12,000 out of pocket at closing — in exchange for either paying a slightly higher purchase price or getting the price reduction smaller.

Lender credits: Pay a slightly higher interest rate and the lender credits you money at closing to offset your costs. This makes sense if you're short on cash now and expect to refinance or sell within a few years (before the higher rate adds up to more than the credits saved).

No-closing-cost mortgages: The fees don't disappear — they're either rolled into the loan balance or reflected in a higher rate. Know what you're trading and run the break-even math.

There's no single best lender — it depends entirely on your loan type, credit profile, and how you like to communicate.

8Best Mortgage Lenders 2026: Who to Actually Call

There's no single best lender — it depends entirely on your loan type, credit profile, and how you like to communicate. But here's an honest assessment of the major players.

**Online Lenders**

Rocket Mortgage (formerly Quicken Loans) is the largest mortgage originator in the country and earns it mostly on customer experience. The application is genuinely good, document upload is easy, you can track your loan status in real time, and they have people available evenings and weekends. Their rates aren't always the lowest but they're competitive for most borrowers, and the efficiency of the process can offset a few basis points of rate. Best for: conventional and FHA loans for borrowers who value a smooth digital experience.

Better.com is an interesting play for rate-conscious borrowers. They've been aggressively competitive on pricing, especially for well-qualified conventional borrowers. No loan officer commissions (they use salaried staff) so theoretically the savings pass to you. The experience is more DIY than Rocket — if you're comfortable with your situation and don't need hand-holding, you might get a better deal here.

NBKC Bank is consistently ranked among lenders with the lowest average interest rates — data puts them around 6.33% average vs. higher for major retail lenders. They're licensed in all 50 states, strong on conventional and VA loans, and the fee structure tends to be leaner than the big guys.

**Traditional Banks**

Chase has an underrated mortgage program. Existing Chase banking customers can get a rate discount (0.125-0.25%) through their relationship pricing, and they offer up to $5,000 in homebuyer grants for purchases in specific communities. If you already bank with Chase, it's worth getting a quote just for the relationship discount. Also note Chase scored well on affordability and availability metrics in 2026 rankings.

Bank of America similarly rewards existing customers and has similar grant programs. Their digital mortgage experience has improved considerably. Good for FHA and conforming conventional loans.

Wells Fargo has had a rocky few years on the regulatory/reputation front but the mortgage product itself is fine for straightforward borrowers. Not my first call but worth including in your comparison.

**Credit Unions**

PenFed Credit Union consistently offers some of the best rates in the market — research puts them at the top of interest rate comparisons during the review period. Membership is open to anyone (you can join by making a small donation to a partner charity if you don't qualify via military/federal employment). Strong on conventional, VA, and jumbo. If you're willing to navigate the credit union application process, the rate savings can be substantial.

Navy Federal Credit Union — if you're eligible (military, veterans, DOD employees, family members) — this is arguably the best lender for VA loans, period. Their rates, service, and understanding of the VA loan process is excellent. They also have flexible conventional products.

Local credit unions: check your state and employer. Credit unions are member-owned so their profits don't go to shareholders — they come back as better rates. The tradeoff is sometimes slower processing and less tech-savvy interfaces. For the right borrower at the right time, a local credit union can beat everyone else on rate.

**Mortgage Brokers**

A broker isn't a lender — they're a middleman who shops your loan to dozens of wholesale lenders. This is actually really valuable if your situation is complex: self-employed income, recent credit issues, unusual property type, jumbo loan. Brokers access wholesale rates that aren't available to consumers directly, and a good broker will find the best overall package — rate plus fees — across multiple lenders.

The catch: not all brokers are created equal. Ask any broker you're considering how many wholesale lenders they have access to (you want 20+), how they're compensated (typically 1-2% of loan amount paid by the lender), and what their average time to close looks like.

For self-employed borrowers especially: a broker who specializes in non-QM or bank statement loans can often get deals done that retail lenders would decline. That expertise has real value.

**Who Has the Lowest Rates Right Now?**

Lennar Mortgage was showing 5.34% averages in recent rankings — though this partly reflects their builder incentive programs where the developer subsidizes the rate to sell homes. Veterans United was at 6.40% average but strong on VA-specific products. NBKC at 6.33%. The variance across lenders for the same borrower profile can easily be 0.25-0.50% on rate — which on a $400,000 loan represents $50-100/month or $18,000-36,000 over 30 years. Getting three quotes isn't optional. It's required.

9How to Shop Mortgage Rates Without Destroying Your Credit

Here's the thing that keeps people from shopping properly: fear of credit score impact. Multiple hard inquiries, multiple lenders, damaged credit — that's the story people tell themselves. It's mostly wrong.

FICO and VantageScore both treat multiple mortgage applications within a short window as a single inquiry. FICO's window is 45 days (the old guidance was 14 days but newer scoring models expanded it). VantageScore's window is 14 days. Since most lenders use FICO models, you have 45 days to shop as many lenders as you want and it counts as ONE hard inquiry — not multiple.

So practically: - Apply to 3-5 lenders simultaneously or within a 2-week window - Collect all your Loan Estimates within the same period - Compare side by side - That's one inquiry on your credit. One.

**How to Actually Compare Loan Estimates**

The Loan Estimate form is standardized — all lenders use the same format because regulators require it. This makes comparison easier. Focus on:

Page 1, Section A: Lender fees (origination, points, processing, underwriting). This is where lenders differ most and where you have negotiating leverage.

Page 1, interest rate and APR: Rate matters but APR tells you more — it's the rate plus all fees expressed as an annual percentage. A lower rate with higher fees might have a higher APR than a slightly higher rate with lower fees.

Page 2, cash to close: Bottom line — what are you actually bringing to closing?

Page 3: Contact info and comparisons. Lenders are required to include comparisons with other loan products here.

Bring competing Loan Estimates to each lender and ask them to beat it. 'Lender A quoted me 6.00% with $1,800 in origination on the same loan amount and term — can you do better?' They'll often find room.

**Rate Locks: What They Are and How to Use Them**

Once you're under contract and have chosen a lender, you'll need to lock your rate. A rate lock is a commitment from the lender to honor a specific rate for a specific period — typically 30, 45, or 60 days.

Longer locks cost more — usually 0.125-0.25% per 15-day extension. A 60-day lock might be 0.25% more expensive than a 30-day lock. If your closing is in 30 days, lock for 30. If you're cutting it close on a complicated deal, lock for 45.

If rates drop after you lock: some lenders offer float-down options — you pay a fee upfront and if rates drop by a certain amount before closing you get the lower rate. Worth it in a declining rate environment.

If your lock expires before closing (construction delays, title issues, etc.): you'll need to either extend the lock (at cost) or re-lock at whatever current market rate is. This is genuinely painful if rates moved up since you locked. Build in buffer.

**The Rate Quote Shell Game**

Not every lender advertises the full picture. Watch for: - Teaser rates that assume points purchased (1 'point' = 1% of loan amount = rate reduction of roughly 0.25%. A 5.75% rate might require paying 2 points to get there) - Rates quoted without property taxes/insurance ('payment' quotes that look low) - Introductory ARM rates presented without the adjustment risk - 'Rate' vs APR confusion — always compare APR to APR

ASK: 'Is this rate with or without points?' If with points, ask what the rate is without points and calculate whether buying down makes sense for your situation.

10Refinancing in 2026: When the Math Works and When It Doesn't

Refi applications ticked up this year as rates came off their 2023-2024 peaks. A lot of homeowners are sitting on mortgages in the 7-8% range from that era and the math to refinance at 6.11% is starting to look compelling. Let's run through it properly.

**The Basic Break-Even Calculation**

Step 1: Calculate your monthly savings. If your current rate is 7.25% and you refinance to 6.11% on a $350,000 remaining balance: - Old payment: ~$2,390/month P&I - New payment: ~$2,124/month P&I - Monthly savings: ~$266

Step 2: Estimate closing costs. A straight rate-and-term refi on that loan amount typically runs $4,000-$7,000 depending on state, lender, and whether you buy points.

Step 3: Break-even = closing costs / monthly savings - $5,500 / $266 = 20.7 months (under 2 years)

If you plan to stay in the house at least 2 years, this refi makes clear financial sense. If you're planning to sell in 18 months, it's a wash or slightly negative.

**The Thumb Rule People Cite (And Its Limits)**

The 'refinance when you can lower your rate by 1%' rule is a rough heuristic from an era of smaller loan balances. On a $600,000 loan, even a 0.5% rate reduction can justify a refi depending on closing costs. On a $150,000 loan, you might need 1.5% improvement before the math works. Use the actual break-even calculation, not the rule of thumb.

**Rate-and-Term vs. Cash-Out Refinance**

Rate-and-term: You're just changing the rate and/or loan term. Loan balance stays roughly the same. This is pure interest cost optimization.

Cash-out: You borrow more than your current balance, pocket the difference. On a home worth $500,000 with a $250,000 mortgage, you might refinance to a $350,000 mortgage and take $100,000 cash out (minus closing costs). Useful for home improvements, debt consolidation, or investment.

The warning on cash-out: You're converting equity into debt. At 6.11% on a 30-year refi, that $100,000 costs you roughly $63,000 in interest over the life of the loan. If you're using it to pay off 22% credit card debt, absolutely worth it. If you're using it to take a vacation, aggressively bad idea.

Cash-out refinance rates are typically 0.125-0.25% higher than rate-and-term because the lender's risk goes up when you're pulling equity out.

**What to Watch When Refinancing**

Don't reset your amortization thoughtlessly. If you're 7 years into a 30-year mortgage, refinancing to a new 30-year starts the clock over — you'll be paying mortgage interest for another 30 years, adding 7 years of total payments. Consider refinancing to a shorter term (20-year, 15-year) if your monthly cash flow supports it.

Stealth cost: lenders sometimes roll closing costs into the loan balance ('no closing cost' refi). Your rate is slightly higher, or your balance is larger. Not inherently bad but understand what you're trading.

Employment and income verification: same drill as a purchase. Don't change jobs right before a refi.

Streamline refis: FHA and VA have streamlined refi programs that skip the appraisal and reduce documentation. FHA Streamline requires you currently have an FHA loan and are lowering your rate. VA IRRRL (Interest Rate Reduction Refinance Loan) is the VA version — similarly simplified. These can close faster and cheaper. If you have an FHA or VA loan from 2023-2024 at 7-8%, you should be calling your lender about a streamline right now.

11Home Equity Products: HELOC vs. Home Equity Loan in 2026

If you bought a home in 2019-2021 you likely have significant equity. Prices ran up 30-50%+ in many markets and you've been paying down principal for 4-5+ years. That equity is an asset. Here's how to use it intelligently — and the traps to avoid.

**Current Rates**

As of mid-March 2026, according to Bankrate's survey of major lenders: - HELOC average: 7.18-7.23% (variable, prime-based) - Home equity loan (10-year fixed): 7.44-7.89% (the spread varies by lender) - Borrowers with excellent credit (750+) can find HELOCs closer to 6.50%

Both are at their lowest since 2022 — down significantly from the 9-10% range in 2023.

**HELOC (Home Equity Line of Credit)**

This is a revolving credit line secured by your home equity. You get approved for a line amount, draw on it as needed (like a credit card but secured and much lower rate), pay it down, draw again.

Typical structure: - Draw period: 5-10 years where you can borrow and only pay interest - Repayment period: 10-20 years where the balance amortizes - Variable rate tied to prime rate (currently Prime + 0-2% depending on your credit and lender) - LTV limit: most lenders go up to 80-85% combined (mortgage + HELOC / home value)

On a $500,000 home with $200,000 mortgage: your available HELOC equity at 80% CLTV is $200,000 ($400K x 80% = $400K - $200K existing = $200K line available).

Best use cases: home improvements with variable cost (you draw as bills come in, not upfront), emergency fund backstop (leave it undrawn but available), situations where you need flexible access to capital over time.

Risk: it's a variable rate product. When the Fed was hiking in 2022-2023, HELOC rates went from 4% to 9%+ in 18 months. Your payments can jump. Don't use a HELOC to fund fixed ongoing expenses with no plan to pay it down.

**Home Equity Loan**

Lump sum, fixed rate, fixed payment, fixed term. You borrow a specific amount, get it all at once, pay it back in equal monthly payments at a locked rate.

On the same $500,000 home, a $100,000 home equity loan at 7.47% for 10 years: monthly payment ~$1,187. Total interest paid: ~$42,500.

Best use cases: one-time large expenses you know the total for upfront — a specific renovation project, debt consolidation, education costs. The predictability of a fixed payment is the whole product.

**HELOC vs. Home Equity Loan — Which One**

If you know exactly how much you need and when: home equity loan. The slightly higher rate buys you certainty.

If you need flexible access over time, may not draw the full amount, or want to pay down and redraw: HELOC. The variable rate risk is real but manageable.

If rates are rising: home equity loan (lock the fixed rate before it gets worse). If rates are declining (like 2026): HELOC might be better since your variable rate will drift down with prime.

**One More Option: Cash-Out Refi vs. HELOC**

If you could simultaneously lower your first mortgage rate AND access equity, a cash-out refi makes more sense than adding a home equity product. The math: if your first mortgage is 7.5% and you're being quoted 6.11% on a new first with cash out — you're lowering your primary rate AND accessing equity in one transaction. One closing cost, one payment.

If your first mortgage is 3.5% (bought in 2020-2021), you absolutely do not want to touch that rate. A HELOC or home equity loan keeps your first intact while accessing equity. Don't give up a 3.5% mortgage to pull cash out at 6.11%.

You pay it upfront at closing to permanently reduce your interest rate.

12Mortgage Points: The Buy-Down Math Explained

Mortgage points. Also called discount points. One point equals 1% of your loan amount. You pay it upfront at closing to permanently reduce your interest rate.

Typical trade-off in 2026: pay 1 point (1% of loan amount) to reduce rate by approximately 0.25%.

On a $400,000 loan: - 1 point = $4,000 upfront - Rate reduction: 6.11% → 5.86% - Monthly payment difference: $2,432 → $2,365 = $67/month - Break-even: $4,000 / $67 = 59.7 months = just under 5 years

If you stay in the house for 5+ years: buying points was a good deal. Under 5 years: you paid $4,000 to save less than $4,000. Bad trade.

This math gets better on: - Larger loan amounts (the monthly savings scale up; the 5-year threshold roughly holds) - Longer expected hold periods - When rates are elevated and you expect the discounted rate to still be competitive vs. future refis

It gets worse when: - You might sell or refi within a few years - You're cash-constrained and paying points depletes your reserves - The rate reduction offered is smaller than 0.25% per point (some lenders offer only 0.125% — check this explicitly)

**Negative Points (Lender Credits)**

This is the reverse: lender pays you points at closing (credits to offset your fees) in exchange for a higher rate. You can use lender credits to reduce closing costs significantly — sometimes to near zero.

Makes sense if: cash is tight at closing, you plan to sell or refi within 3-4 years, you'd rather have the cash now. The math is just break-even in reverse — how long before the higher rate costs you more than the credits saved?

**Builder Rate Buy-Downs**

New construction has popularized temporary buy-downs — 2-1 buy-down being common. The builder (or sometimes the seller in resale) pays to temporarily reduce your rate: - Year 1: 4.11% (2% below note rate) - Year 2: 5.11% (1% below note rate) - Year 3+: 6.11% (full note rate)

The builder pays the difference into an escrow that subsidizes your payment for the first two years. It's a sales tool, but the math is genuinely positive if you get it as a true concession — the builder is paying the cost. Negotiate for this in new construction deals, especially in slower markets where builders are motivated.

13PMI: What It Is, What It Costs, and How to Kill It

Private mortgage insurance protects the lender — not you — if you default. You pay for their protection. It's the price of admission for conventional loans with less than 20% down, and it adds hundreds of dollars to your monthly payment.

**The Costs (2026 Rates)**

PMI is priced based on your loan-to-value ratio and credit score. Rough annual premium rates:

95% LTV (5% down): - 760+ credit score: 0.58-0.65% annually - 720-759: 0.70-0.80% - 680-719: 0.90-1.10% - Below 680: 1.20-1.50%+

90% LTV (10% down): - 760+: 0.35-0.40% - 720-759: 0.45-0.55% - 680-719: 0.55-0.70%

On a $315,000 loan at 90% LTV with a 720 credit score: 0.50% = $1,575/year = $131/month. That's the incentive to get to 20% equity.

**How to Remove PMI**

You have three paths:

Automatic cancellation: Under the Homeowners Protection Act (HPA), lenders must automatically cancel PMI when your loan balance reaches 78% of the original purchase price based on your scheduled payments. This is the floor — you don't have to do anything but it takes the longest.

Requested cancellation: When your balance hits 80% of the original purchase price, you can formally request cancellation. The lender can require: - A good payment history (no 30-day lates in the past year, no 60-day lates in the past 2 years) - Certification that no subordinate liens exist on the property - Sometimes a new appraisal showing value hasn't declined

Appraisal-based cancellation: If your home's value has increased significantly since purchase (which it has for most 2019-2022 buyers), you can order a new appraisal. If the appraisal demonstrates 20%+ equity based on current value, you can request PMI removal even if you haven't paid down 20% based on purchase price. Contact your servicer (not your original lender — loans get sold) about their specific process. Some require you to have owned the property for at least 2 years.

**Lender-Paid PMI vs. Borrower-Paid PMI**

Borrower-paid PMI (BPMI): Monthly premium. You pay it, you can cancel it when you hit 20% equity. Most common structure.

Single-premium PMI: Pay the entire PMI cost upfront at closing (usually 1-2% of loan amount rolled into closing costs). Higher upfront, no monthly PMI payment. Makes sense if you have excess cash but not enough for 20% down, and plan to stay long-term.

Lender-paid PMI (LPMI): Lender pays the PMI and you take a higher rate. Rate increase is permanent — can't be removed when you hit 20% equity. Compare carefully: if LPMI adds 0.375% to a $320,000 loan, that's ~$100/month more forever. BPMI on the same loan might be $140/month for 6 years until you hit 20% equity. Do the NPV math.

**FHA MIP vs. Conventional PMI**

This is where people get trapped. FHA MIP (mortgage insurance premium) is: - 1.75% upfront (rolled in) - 0.55-0.85% annual ongoing premium - With less than 10% down: doesn't go away for the life of the loan

Conventional PMI cancels at 20% equity. FHA MIP doesn't (with <10% down). On a 30-year loan, this can be a $30,000-$50,000+ difference in total insurance costs. If your credit score is 640+ and you can do conventional with PMI instead of FHA with MIP, run the comparison. FHA's rate advantage often doesn't offset the lifetime MIP cost.

14Common Mortgage Mistakes That Cost Real Money

Been watching these play out for years. The same mistakes show up over and over — not because people are dumb but because nobody told them.

**Not shopping multiple lenders**

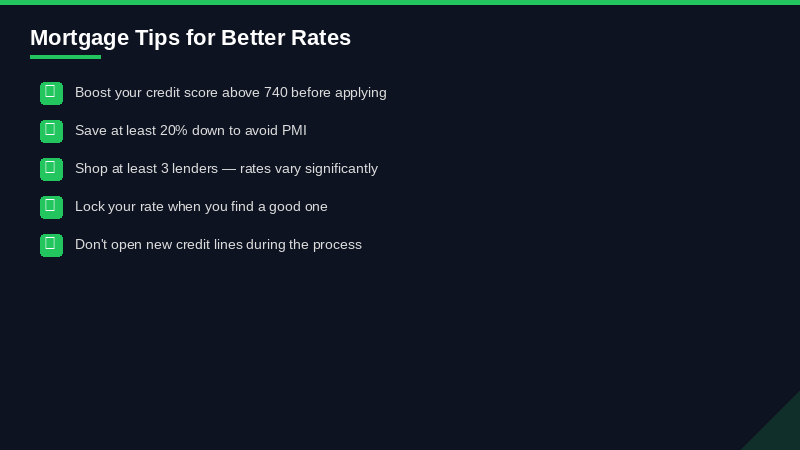

This is the biggest one. A quarter-point difference on a $400,000 mortgage is about $60/month — $21,600 over 30 years — and the origination fee differences can easily add another $3,000-$5,000. People spend 40 hours researching the perfect sofa and submit one mortgage application. Get at least three quotes. Five is better.

**Letting your credit score drift before application**

Opening a new credit card for the rewards points or buying a car three months before your mortgage application can shift your credit score meaningfully. New accounts lower average account age. Hard inquiries ding you. Increased utilization if you're carrying a balance. Every tier on the credit score ladder corresponds to a different rate. Going from 720 to 679 might cost you 0.25-0.375% on your rate. Don't touch your credit for at least 6 months before applying for a mortgage.

**Paying off old collections before closing (sometimes wrong)**

Counterintuitive: paying off an old collection account can temporarily lower your credit score because it updates the account's activity date, making it 'newer' in scoring models. Ask your loan officer or a credit consultant what to do with any derogatories before you make a move. Sometimes leaving them alone is better.

**Underestimating total housing costs**

The mortgage payment is one line item. Property taxes can add 1-3% of value per year depending on location. Homeowners insurance. HOA fees. Maintenance. Most financial models suggest budgeting 2-3% of home value annually for all costs beyond the mortgage. On a $450,000 home that's $9,000-$13,500/year on top of your mortgage payment. This catches first-time buyers completely off guard.

**Moving money around before or during underwriting**

Underwriters want to trace every dollar. Moving $20,000 from your investment account to your checking account to your savings account looks like layering to a bot. It generates 'large deposit' conditions and requires letters of explanation and account statements for every account the money touched. Keep your money in place during the mortgage process. If you must transfer, document it clearly and tell your loan officer immediately.

**Skipping the rate lock or locking too short**

Not locking your rate is a gamble. If rates move up 0.25% between application and closing, that's $60-80/month more — forever. Lock it. And lock long enough — if you're 30 days from closing, lock 45 days to give yourself buffer. The cost of a slightly longer lock is trivial vs. the risk of rate movement.

**Making the offer contingency-free to compete**

In hot markets buyers waive inspection contingencies and sometimes financing contingencies to make their offers more competitive. Waiving financing contingency means if your loan falls through, you lose your earnest money (typically 1-3% of purchase price). Only do this if you have iron-clad certainty of your loan approval — pre-underwritten approval, not just pre-approval. And on inspections: at minimum, do a walkthrough with an inspector before making an offer, even if you can't make it a formal contingency.

**Ignoring the Loan Estimate**

You get a Loan Estimate within 3 business days of application. Most people glance at the monthly payment and file it. Read it. Page 1 has your rate, term, monthly payment estimate. Page 2 has every closing cost line item. Page 3 has comparison tools. Compare your LE against other lenders' LEs. This is the document that protects you — use it.

**Quitting your job right before or during the process**

Employment status is verified at application and re-verified right before closing. Changing jobs during the mortgage process — especially to a different field or from salary to commission — can send you back to square one. Even a same-field, same-salary switch can cause issues if you're on any kind of probation period. Wait until after closing if at all possible.

**Forgetting about rate locks on new construction**

New construction timelines slip. If your builder says 'close in 60 days' you might actually close in 90 or 120. A 60-day rate lock expires and you're re-locking at a higher (or unknown) rate. Either get a longer lock from the start (and budget the cost) or choose a lender with free lock extensions on new construction. Many builders have preferred lenders who offer special rate protection for this reason.