1Why You Need to Invest (The Math Is Brutal If You Don't)

Let me start with something most people don't actually feel in their gut until it's too late.

Inflation. It's boring. It's invisible. And it is quietly eating your savings right now.

The Federal Reserve targets 2% inflation annually. That sounds harmless — two percent, whatever. But on $100,000 sitting in a savings account paying 0.01% (which is still what the big banks pay on basic checking), that's roughly $2,000 to $3,000 in real purchasing power gone. Every. Single. Year. You don't see a withdrawal. You don't get a notification. Your balance looks the same. But what that money can actually buy? That shrinks.

Over 10 years, $100,000 at 2% inflation is worth about $82,000 in today's dollars. Over 20 years, closer to $67,000. You didn't make a single bad investment. You just didn't invest at all, and the clock did the damage.

Now flip it. The S&P 500 has returned roughly 10% annually on average over the last 50 years — about 7% after inflation. Put that same $100,000 in a basic index fund and leave it for 20 years? You're looking at something closer to $386,000 in nominal terms. That's not a typo. That's compound growth doing its thing without you doing anything heroic.

The gap between those two outcomes — $67,000 in real purchasing power versus $386,000 — is the entire reason investing exists. It's not about getting rich quick. It's about not getting poor slowly.

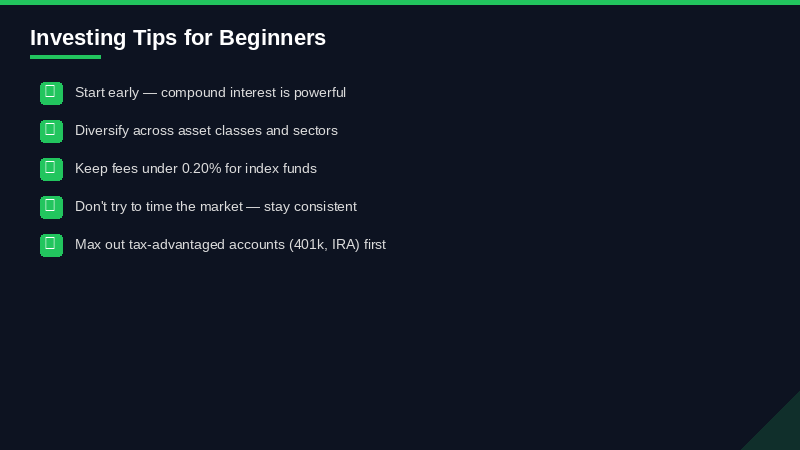

Here's what trips people up: they think investing is for people who have money figured out already. Like there's some threshold you have to cross before it makes sense. There isn't. You can start with $100. You can start today. The only variable that matters more than how much you invest is when you start — because time is the ingredient that makes everything else work.

A 25-year-old investing $300/month has a better outcome at 65 than a 35-year-old investing $600/month, all else equal. That's not motivational-poster math. That's actual math. Starting late costs you more than investing less.

2Investment Account Types — Which One Do You Actually Need

This is where most beginner guides lose people. They list every account type, define them in jargon, and you walk away more confused than when you started. Let me just tell you what to open and why.

**Taxable Brokerage Account**

This is the simplest thing. You open an account, you put money in, you buy stuff. No contribution limits. No income restrictions. You pay taxes on dividends and capital gains each year (or when you sell). This is the right account if you've already maxed your tax-advantaged accounts, or if you need flexibility to access your money before retirement.

Fidelity, Schwab, Vanguard, Robinhood — all of them offer this. Open one in about 10 minutes.

**Roth IRA — The One You Probably Want First**

For 2026 the contribution limit is $7,500 per year ($8,600 if you're 50 or older). You contribute after-tax money, it grows tax-free, and withdrawals in retirement are completely tax-free. No taxes on decades of growth. That's a massive deal.

The catch: income limits. If you're single and make more than $168,000 (phase-out starts at $153,000), you can't contribute directly. Married filing jointly, phase-out starts at $236,000 and cuts off at $246,000. There's a workaround called the backdoor Roth for high earners — we'll touch on that in the Roth vs Traditional section.

If you're in your 20s or 30s, earning a normal income, the Roth IRA is probably your best account. The math on tax-free compounding over 30-40 years is hard to beat.

**Traditional IRA**

Same $7,500 limit in 2026. You contribute pre-tax money (if you qualify for the deduction), it reduces your taxable income now, grows tax-deferred, and you pay ordinary income tax when you withdraw in retirement. Better choice if you're in a high tax bracket now and expect to be in a lower one in retirement.

Deductibility gets complicated if you (or your spouse) has a 401k at work. The IRS phases out the deduction at pretty modest income levels in that case — starting at $79,000 for single filers in 2026. If you can't deduct it, you're probably better off doing a Roth.

**401(k) — Max This Before Almost Anything Else**

If your employer offers a 401k with a match, that match is literally the best return available to you in finance. A 50% match on the first 6% of your salary is a 50% instant return before the market does anything. Nothing else competes with that.

The 2026 employee contribution limit is $24,500 (up from $23,500 in 2025). If you're 50 or older, add another $8,000 catch-up contribution — so $32,500 total. The contribution comes out pre-tax (traditional 401k) or post-tax (Roth 401k, if your employer offers it), and it doesn't count against your IRA limit.

If your employer matches, contribute at least enough to get the full match. Not doing this is leaving part of your compensation on the table.

**HSA — The Secret Triple Tax Advantage**

If you have a High Deductible Health Plan (HDHP), you qualify for a Health Savings Account. The 2026 limits are $4,400 for self-only coverage and $8,750 for family coverage.

Here's why this is underrated: contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. That's three tax advantages — no other account does all three. After age 65, you can withdraw for any reason and just pay ordinary income tax, making it basically a second Traditional IRA at that point.

Invest your HSA contributions rather than leaving them in the cash default. Most HSA providers let you invest in index funds once you hit a certain balance threshold ($1,000 is common). Fidelity's HSA has no threshold and lets you invest immediately — that's the one I'd recommend.

**Order of Operations (The Actual Priority List)**

1. Contribute to 401k up to the full employer match 2. Max your HSA (if eligible) 3. Max your Roth IRA ($7,500 in 2026) 4. Max your 401k ($24,500 total) 5. Taxable brokerage for anything beyond that

This order isn't universal — high earners, people with debt, or those planning to retire early might rearrange it — but for most people earning a normal income, this is the right sequence.

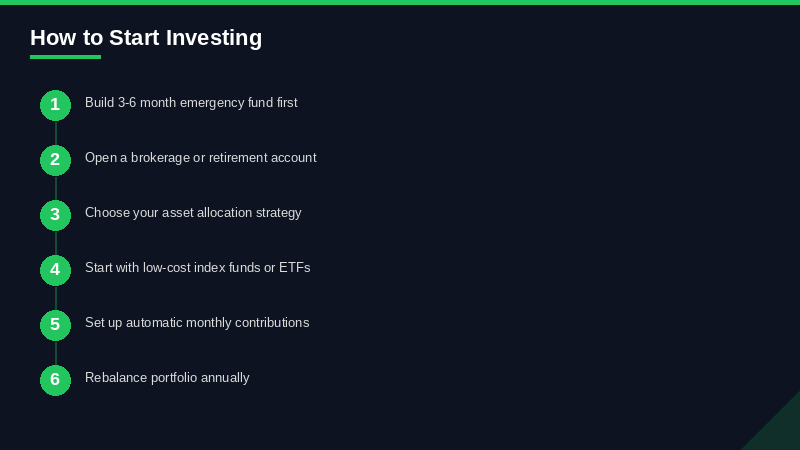

3How to Start Investing With $100

A hundred bucks. That's it. That's the real starting point now, not the theoretical 'someday when I have more' starting point.

Fractional shares changed everything. Five years ago, buying one share of Amazon meant having $3,000+ sitting around. Now you can buy $10 worth of Amazon, $25 worth of Apple, $50 worth of a Vanguard ETF. Every major brokerage offers fractional shares now. Fidelity calls them Stocks by the Slice. Schwab calls them Stock Slices. Robinhood just lets you do it natively.

With $100, here's what I'd actually do:

**Option 1: Buy VTI or VOO**

VTI is the Vanguard Total Stock Market ETF. 0.03% expense ratio. Owns ~3,700 US stocks. One share trades around $230 as of early 2026, but with fractional shares you just put in $100 and buy roughly 0.43 shares. Done. You now own a tiny piece of basically every public company in America.

VOO is the S&P 500 version — same 0.03% expense ratio, tracks the 500 largest US companies. One or the other. Both are fine. I don't think the difference matters much for a beginner.

**Option 2: Use a Robo-Advisor**

If you want someone else to handle the allocation — choosing what percentage goes in stocks vs bonds, rebalancing when things drift — a robo-advisor is worth considering. Betterment and Wealthfront both have a 0.25% annual fee and will build you a diversified portfolio based on your risk tolerance. Wealthfront requires a $500 minimum. Betterment has no minimum.

At $100, Betterment is your robo option. At $500+, you have more choices.

**Option 3: Just Buy FZROX**

Fidelity's Zero Total Market Index Fund. Expense ratio: 0.00%. That's not a typo. Free. Zero. No trading fees if you use Fidelity's platform. The catch is it's only available through Fidelity, can't be transferred in-kind to another broker, and has some tracking differences vs VTI. For a beginner at $100? Doesn't matter. It's free and it works.

**What to Actually Do Right Now**

1. Open a Roth IRA at Fidelity or Schwab (15 minutes, no minimum) 2. Set up a recurring deposit — even $25/week 3. Buy VTI, VOO, or FZROX with whatever you have 4. Automate it and stop watching it daily

That's the whole strategy. The rest is details.

This trips people up because the terms get used interchangeably, and sometimes they overlap.

4Index Funds vs ETFs — What's Actually the Difference

This trips people up because the terms get used interchangeably, and sometimes they overlap.

**Index fund**: A fund that tracks an index (like the S&P 500). Can be structured as a mutual fund or an ETF. Passive management. Low cost.

**ETF (Exchange-Traded Fund)**: A fund that trades on an exchange like a stock, meaning you can buy and sell throughout the trading day at the market price. ETFs can track indexes (most do) or be actively managed.

So most index funds you'll use are ETFs. But not all ETFs are index funds (there are active ETFs). And not all index funds are ETFs (Fidelity and Vanguard have mutual fund versions of index funds too).

For practical purposes as a beginner, the distinction that matters is ETF vs mutual fund — not index vs active.

**ETF advantages**: Trade throughout the day, often have slightly lower expense ratios, can be bought at fractional shares on most platforms, tax-efficient.

**Mutual fund advantages**: Can set up automatic investments in dollar amounts (not share amounts), DRIP reinvestment is seamless, sometimes available in your 401k when ETFs aren't.

Here are the core ETFs you should know:

**VOO — Vanguard S&P 500 ETF** - Expense ratio: 0.03% - Tracks the S&P 500 (500 largest US companies) - ~$500B in assets under management - This is probably the most famous single ETF in retail investing - The S&P 500 has outperformed most active fund managers over any 15-year period

**VTI — Vanguard Total Stock Market ETF** - Expense ratio: 0.03% - Tracks the entire US stock market (~3,700 companies) - Includes small and mid-cap stocks VOO doesn't have - Slightly more diversified than VOO, very similar historical performance - My personal preference over VOO for total market exposure

**VXUS — Vanguard Total International Stock ETF** - Expense ratio: 0.07% - Everything outside the US — developed and emerging markets - ~8,000 international stocks - Controversial choice: international stocks have underperformed US stocks for 15+ years. But concentration in US-only is a real risk. A reasonable allocation: 70-80% VTI, 20-30% VXUS.

**BND — Vanguard Total Bond Market ETF** - Expense ratio: 0.03% - US bonds — government and corporate, short and long term - Ballast for your portfolio. Bonds tend to zig when stocks zag (not always, but usually) - If you're under 40, you probably don't need much of this. If you're 50+, it earns more of your allocation.

**The Three-Fund Portfolio**

VTI + VXUS + BND. That's it. Three ETFs, blended expense ratio around 0.04%, and you own essentially the entire global investable market with some fixed income as ballast. This is what Bogleheads have been preaching for decades, and the data backs it up. You don't need 15 funds. You don't need sector ETFs. You don't need a portfolio that requires a spreadsheet to manage.

**What About Sector ETFs?**

Tech ETFs, clean energy ETFs, biotech ETFs — these are almost always a distraction for beginners. They're fine for speculation with money you can afford to lose. They're not a foundation. The moment you start betting on sectors, you've moved from investing to guessing. Most of the time you're just buying yesterday's winners at today's elevated prices.

**Expense Ratios: Why 0.03% vs 1% Is a Huge Deal**

This is where most people underestimate math. A 1% annual expense ratio on $100,000 over 30 years costs you roughly $78,000 in lost compounding vs a 0.03% expense ratio fund. Active mutual funds routinely charge 0.5-1.5%. Hedge funds charge 2% + 20% of profits. The data consistently shows these higher fees aren't justified by performance. Buy cheap index funds. Keep costs low. Let the market do its thing.

5Best Brokerages for Beginners in 2026

Short version: Fidelity or Schwab. One of those two, you're set. The rest have tradeoffs worth knowing about.

**Fidelity — The One I'd Recommend First**

$0 account minimum. $0 commissions on stocks and ETFs. No account fees. Their own index funds (FZROX, FZILX) charge literally 0% expense ratios — nothing I've seen beats that. Fractional shares through Stocks by the Slice. HSA accounts with immediate investment ability. The app is solid. Research tools are excellent. Customer service is actually good, which isn't something you can say about every brokerage.

If you're starting from scratch in 2026 and don't already have a brokerage, open a Fidelity account. This isn't a hot take — it's just the objectively strongest all-around package for most people.

**Charles Schwab — Essentially Tied**

$0 account minimum. $0 commissions. No account fees. Their own index ETFs (SCHB, SCHX) are also extremely cheap — 0.03% expense ratios. Stock Slices for fractional shares on S&P 500 companies. Schwab Intelligent Portfolios (their robo) requires $5,000 but charges no management fee, which is unusual. Customer service is excellent. They absorbed TD Ameritrade, so the thinkorswim platform (for more active traders) is now under the Schwab umbrella if you ever want more sophisticated tools.

Fidelity vs Schwab is basically a coin flip. Pick one, stop overthinking it.

**Vanguard — Great Funds, Mediocre Platform**

Vanguard invented the index fund. Jack Bogle literally created the S&P 500 index fund for retail investors in 1976. The company is structured as investor-owned (fund shareholders own the company), which keeps costs aligned with your interests in a way no other brokerage can quite match.

But honestly? The platform is dated. The app has historically been clunky. They've been improving, but it's still not as polished as Fidelity or Schwab. And you can buy all the Vanguard ETFs (VOO, VTI, etc.) through Fidelity or Schwab commission-free anyway.

Who should use Vanguard: people who want to invest in Vanguard mutual funds directly (vs ETFs), or who want the ideological alignment with a truly investor-owned structure. Totally valid. But for a beginner optimizing for ease of use, Fidelity wins.

**Robinhood — Better Than Its Reputation, But With Caveats**

Robinhood gets blamed for gamifying investing, and that's fair — the dopamine-optimized UI has caused real harm by encouraging speculative behavior. But the account itself is fine. $0 minimum, $0 commissions, fractional shares, clean interface, now offers IRAs with a 1% contribution match (3% if you're on Gold at $5/month).

The 1% IRA match is actually interesting — it's real money. 1% on $7,500 = $75 free. 3% Gold = $225 free. Worth running the math if you were already going to use Robinhood.

Who should avoid Robinhood: anyone who's prone to checking their portfolio 20 times a day and making impulse trades. The app is literally designed to encourage that behavior. If you're going to set-it-and-forget-it on index funds, Robinhood is fine.

**SoFi — Solid for the SoFi Ecosystem**

$0 minimum, $0 commissions, fractional shares starting at $5. They offer their own automated investing (0.25% fee) and active investing in one platform. Good if you're already using SoFi for banking or loans and want everything in one place. Not the strongest standalone brokerage choice vs Fidelity/Schwab, but not bad.

**What to Actually Look For in a Brokerage**

- No account minimum - No commissions on stocks and ETFs - Fractional shares - Good mobile app - SIPC protection (all major US brokerages have this) - IRA and taxable account options

All five brokerages above hit most of these. The differences are marginal. Pick one, open an account today, put $100 in, buy VTI. That action is worth infinitely more than another week of brokerage comparison research.

6Robo-Advisors Compared: When They're Worth It and When They're Not

Robo-advisors are automated portfolio managers. You answer some questions about your goals and risk tolerance, they build you a diversified portfolio of ETFs, and they automatically rebalance it and (usually) do tax-loss harvesting. You pay a small annual fee for this.

Are they worth it? Depends on what you're comparing them to.

Compared to paying 1% for a human financial advisor who just puts you in index funds anyway? Absolutely worth it.

Compared to just buying VTI yourself and doing nothing else? Marginally worse on cost, potentially better on behavior (because they smooth out panic selling through automatic rebalancing).

Here's where each one sits:

**Betterment** - Annual fee: 0.25% (Digital plan) / 0.40% (Premium, requires $100,000) - Account minimum: $0 - Features: Goal-based investing, tax-loss harvesting, automatic rebalancing, IRA options, joint accounts - Best for: Beginners who want a simple, well-designed robo experience with no minimum. The UX is excellent. Tax-loss harvesting kicks in early — you don't need $50K like at Schwab. - Verdict: Solid pick. The 0.25% fee is industry standard and reasonable for what you get.

**Wealthfront** - Annual fee: 0.25% - Account minimum: $500 - Features: Tax-loss harvesting on all accounts, direct indexing at $100K+, Wealthfront Cash Account (good APY), Path financial planning tool - Best for: People who want a slightly more sophisticated product. Wealthfront's direct indexing (buying individual stocks to replicate an index) starts at $100K and can meaningfully improve after-tax returns vs ETFs for higher earners. - Verdict: Essentially tied with Betterment. Pick based on which app you like better.

**Schwab Intelligent Portfolios** - Annual fee: $0 - Account minimum: $5,000 - Tax-loss harvesting: Available at $50,000+ - Features: Automatic rebalancing, 51 asset classes, access to CFPs via Premium ($300 setup + $30/month) - Best for: People with $5K+ who want automation with no management fee. The catch is they hold cash (3-10% of your portfolio in a Schwab money market), which is their revenue model. That cash drag is essentially the hidden fee. - Verdict: The $0 fee headline is appealing, but the cash drag can cost you 0.1-0.3% annually in opportunity cost. Not a deal-breaker, but worth knowing.

**Vanguard Digital Advisor** - Annual fee: Approximately 0.20% all-in (includes fund expense ratios) - Account minimum: $100 - Features: Uses Vanguard's own ETFs (VOO, BND, etc.), goal-based planning, automatic rebalancing - Best for: Vanguard loyalists who want a managed option. The all-in cost of ~0.20% (including fund expenses) is competitive. - Verdict: Good if you're already in the Vanguard ecosystem. Not a compelling reason to switch from Betterment/Wealthfront if you're starting fresh.

**SoFi Automated Investing** - Annual fee: 0.25% - Account minimum: $1 - Features: Goal-based portfolios, automatic rebalancing, free access to human advisors - Best for: SoFi customers who want everything in one place. - Verdict: Fine. The free advisor access is a nice perk. Not best-in-class on features vs Betterment/Wealthfront.

**The Honest Take on Robo-Advisors**

For most beginners with under $50,000, the main benefit of a robo-advisor is behavior management, not superior returns. They keep you invested during downturns through automatic rebalancing. They prevent you from chasing performance. They make it easy to set up recurring contributions.

If you're disciplined — meaning you won't panic sell when the market drops 30% — you can just buy VTI and call it a day. Your all-in cost will be 0.03% vs 0.25-0.28% at a robo. On $50,000 over 20 years that difference compounds to real money.

If you know yourself and know you need guardrails, pay the 0.25% and sleep better.

7Roth IRA vs Traditional IRA — The Tax Math Actually Matters

The standard advice is: if you're young and in a low tax bracket now, do Roth. If you're in a high bracket and expect to be lower in retirement, do Traditional. That's mostly right, but let's run some actual numbers.

**The Core Difference**

- **Roth IRA**: Pay taxes now, never pay taxes again on growth. Contribute after-tax dollars. Withdraw in retirement tax-free. - **Traditional IRA**: Get a tax deduction now (if you qualify), pay taxes on withdrawals in retirement. Contribute pre-tax dollars.

**Scenario 1: 25-year-old making $55,000**

Federal tax bracket: 22%. Marginal rate on that last dollar of income.

Roth IRA: Contribute $7,500. You already paid ~22% tax on that money. It grows for 40 years. You withdraw $0 in federal taxes.

Traditional IRA: Contribute $7,500, get a $1,650 deduction (22% of $7,500). In retirement, assuming you withdraw at a 15% effective rate, you pay ~$1,125 on that $7,500. You came out ahead by $525 on the deduction but behind on retirement taxes.

At modest income levels with long investment horizons, Roth almost always wins. The tax-free compounding over 40 years is worth more than the deduction today.

**Scenario 2: 45-year-old making $200,000**

Federal marginal rate: 32%. They've got maybe 20 years until retirement.

Traditional IRA: Contribute $7,500, get a $2,400 tax deduction today. If effective tax rate in retirement is 20%, pay $1,500 on withdrawal. Net tax benefit: $900.

Roth IRA: Pay 32% on the contribution now. But remember — at this income level, they might not even qualify for a Roth IRA directly (income limit for single filers phases out between $153,000-$168,000 in 2026). They'd need to do a backdoor Roth.

At high income with a shorter runway, Traditional often makes more sense.

**Scenario 3: The Backdoor Roth**

If you make too much for a direct Roth IRA contribution, there's a legal workaround: contribute to a non-deductible Traditional IRA, then immediately convert it to Roth. The conversion triggers no tax because you already paid tax on the contribution.

Caveats: If you have other Traditional IRA money (from rollovers, deductible contributions, etc.), the pro-rata rule applies and can create a tax mess. Get a CPA to walk through this if you're in this situation. But in concept, it works.

**The Part People Forget: Roth Has No RMDs**

Traditional IRAs require you to start taking Required Minimum Distributions (RMDs) at age 73. The IRS wants their tax money eventually. Roth IRAs have no RMDs — you can let that money grow until you die and pass it to heirs tax-free.

For wealth transfer purposes and estate planning, Roth wins decisively.

**Which One Should YOU Do?**

Rough guidelines: - Under 35, income under $80K: Roth. Don't overthink it. - Under 50, income $80K-$150K: Probably Roth, especially if you expect income to grow. - Over 50 or income over $150K: Model it with your actual numbers or talk to a CPA. - Income over $168K (single) / $246K (married): Backdoor Roth or Traditional, depending on situation.

The right answer changes based on too many personal variables to give one universal recommendation. But if you're reading a beginner guide, you're probably in Roth territory.

The 401k is probably the account where most working Americans have the most money sitting, making the most consequential decisions without understanding them.

8The 401(k) Guide: Employer Match, Fund Selection, and Not Leaving Money on the Table

The 401k is probably the account where most working Americans have the most money sitting, making the most consequential decisions without understanding them.

Let's fix that.

**Contribution Limits in 2026**

Employee contribution limit: $24,500 (up from $23,500 in 2025) Catch-up contributions (age 50+): additional $8,000 Total maximum (employee + employer): $70,000

The employer contribution doesn't count against your $24,500 personal limit. So if your employer contributes $5,000, you can still put in $24,500 yourself.

**The Match — Get Every Dollar of It**

Common employer match structures: - 50% of contributions up to 6% of salary - 100% of contributions up to 3% of salary - Dollar-for-dollar up to 4% of salary

Example: You make $75,000. Employer matches 50% up to 6%. That means if you contribute 6% ($4,500), they add 3% ($2,250). Contribute less than 6%? You're leaving free money behind. Contribute more than 6%? Still good — just no more employer match on those additional dollars.

That 50% instant return on your first 6% is better than anything else available to you. Bond yields don't touch it. S&P 500 long-term average doesn't touch it. Literally nothing matches a 50% guaranteed return on investment. Contribute at least to the full match. Full stop.

**Fund Selection in Your 401k**

This is where people get paralyzed. Most 401k menus have 15-30 fund options, a bunch of jargon, and it's not obvious what to pick.

Here's the framework:

1. Look at expense ratios first. Ignore any fund with an expense ratio above 0.5% if there's a cheaper alternative that does roughly the same thing.

2. Find the S&P 500 index fund or total market index fund. In most plans this will be something like "Fidelity 500 Index (FXAIX)" or "Vanguard Institutional Index" or "Schwab S&P 500 Index." It should have an expense ratio below 0.05%.

3. If you want international exposure, find a total international index. If you want bonds, find a bond index.

4. Or, if your plan has them, use Target Date Funds. These are all-in-one funds that automatically shift more conservative as you approach retirement. A 2055 Target Date Fund is heavily stocks now, gradually becomes more bonds over time. Expense ratios on these are usually 0.10-0.15% at major providers. They're not optimal but they're excellent for someone who wants to pick one thing and be done.

**What to Avoid**

- Actively managed funds (the ones with a human stock-picker whose job is to beat the market). Most don't. You pay for it regardless. - Company stock. Unless you have specific reason to concentrate there, having both your paycheck and your retirement savings tied to your employer's fortunes is risk stacking. - Fixed income funds in your 20s and 30s. You have time. Stocks outperform bonds long-term. Don't defensively hold bonds at 28 because they feel safer.

**Traditional vs Roth 401k**

Many employers now offer both. Traditional 401k: pre-tax contributions, taxes on withdrawal. Roth 401k: after-tax contributions, tax-free withdrawal. Same logic as the IRA decision — your tax rate now vs your expected rate in retirement. Roth 401k has no income limit (unlike Roth IRA), so high earners can use it when they can't contribute to a Roth IRA directly.

**What Happens When You Leave a Job**

Roll it over to an IRA. Specifically, a direct rollover — the money goes from your old plan directly to your new IRA without you touching it. If you take a distribution first, they withhold 20% for taxes, and you have to replace that out of pocket to avoid it counting as a taxable distribution. It's a trap. Do a direct rollover. Always.

Rolling to an IRA at Fidelity or Schwab gives you more fund choices and usually lower fees than most employer 401k plans.

9Dollar-Cost Averaging vs Lump Sum — What the Data Actually Shows

You've probably heard both sides of this argument. "Time in the market beats timing the market" is one camp. "Spread your investments over time to reduce risk" is the other. Let's look at what actually happened historically.

**Vanguard's Research**

Vanguard studied this using MSCI World Index data from 1976-2022. The result: lump sum investing outperformed dollar-cost averaging (DCA) 68% of the time across global markets, measured over a one-year period.

The logic is simple. If markets go up over time (they have, historically), you want your money invested as early as possible. Every month your money sits in cash waiting to be deployed, you're missing out on expected returns.

Lump sum wins about two-thirds of the time. DCA wins the other third — primarily when markets decline after you invest.

**But DCA Isn't Wrong Either**

Here's the thing. For most people in the real world, DCA is what they're already doing — they get a paycheck, they contribute to their 401k, they buy $200 worth of VTI. That's DCA by default. And that's totally fine. Automating regular contributions is one of the best investing habits you can build.

The lump sum vs DCA debate really applies to one specific situation: you have a windfall (inheritance, bonus, sale of something) and you're deciding whether to invest it all at once or spread it over 6-12 months.

The data says invest it all at once. But if doing so would cause you to panic and sell everything when it drops 15% in month 2, spreading it out might be better for your actual outcome even if it's suboptimal on paper.

Behavioral finance is real. A theoretically optimal strategy you can't stick to is worse than a slightly suboptimal one you execute perfectly.

**The Practical Answer**

- Regular income investing: just automate it. Put in $X per paycheck, buy index funds, done. - Lump sum situation: invest it all now if you can stomach volatility. Spread over 3-6 months if you know you'll freak out otherwise. - Never let money sit in cash for a year 'waiting for the right time.' There's no right time. The right time was yesterday.

The worst outcome is analysis paralysis — sitting in cash for 12 months trying to decide when to invest, missing the market going up 15% while you deliberated.

10Asset Allocation by Age — The Old Rules and Why They Need Updating

The classic rule you've probably heard: 100 minus your age in stocks.

30 years old? 70% stocks, 30% bonds. 60 years old? 40% stocks, 60% bonds.

This rule was invented when people retired at 65 and expected to live another 10-15 years. Life expectancy has shifted. People are retiring later (or needing money to last 30+ years). Bond yields were historically higher too — bonds used to actually provide meaningful income. For most of the 2010s they barely beat inflation.

The updated version most advisors use now: 120 minus your age. Still a rough heuristic but better accounts for longer lifespans.

30 years old: 90% stocks, 10% bonds. 40 years old: 80% stocks, 20% bonds. 50 years old: 70% stocks, 30% bonds. 60 years old: 60% stocks, 40% bonds.

**My actual take**: If you're under 35, I'm not sure why you own bonds at all. Seriously. You have 30-35 years of compounding ahead of you. Bonds are a drag on long-term growth. A 25-year-old who's 90/10 stocks/bonds would historically have done better just being 100% stocks. The volatility is scary in the moment but it's noise at that time horizon.

Once you're 10-15 years from retirement, shifting toward more fixed income makes genuine sense — not because bonds are great, but because sequence-of-returns risk becomes real. If the market crashes 40% right before you retire, that's a material problem. A 40% crash when you're 30 is annoying and recoverable. At 62? Much harder.

**International Allocation**

Separate from stocks/bonds, there's the question of US vs international. US stocks have dominated international for the last 15 years. But concentration risk is real — if you're 100% US equities and US markets have a lost decade (it's happened before, see 2000-2010), that's a serious problem.

Reasonable ranges: - All US: fine, especially if you work in the US and your human capital is already US-denominated - 70% US / 30% international: more diversified, closer to global market weight - VT (Vanguard Total World) at 0.07% expense ratio: just holds the whole world in one fund, market-cap weighted (~62% US currently)

There's no universally correct answer here. I lean toward at least 20% international just to avoid extreme concentration.

**Simple Allocations by Stage**

- Early career (20s-30s): 100% equities. Split between US (VTI or VOO) and maybe some international (VXUS). Zero bonds, unless you genuinely can't sleep. - Mid career (40s): Still mostly equities. Maybe 80-85%. Start thinking about when you want to retire. - Pre-retirement (50s): 65-75% equities. Add bonds for stability. BND is fine. - At retirement: Typically 40-60% equities, rest in fixed income. Depends heavily on your Social Security, pension, other income sources.

Remember: at retirement you're not liquidating everything at once. You've got a 20-30 year distribution period. You still want growth. Pure bonds at 65 is a recipe for outliving your money.

11Dividend Investing Basics — What It Is and What the Hype Gets Wrong

Dividend investing has a passionate following online. The pitch is appealing: buy stocks that pay you regular cash, live off the dividends, financial independence achieved. There are YouTube channels with millions of subscribers built around this idea.

Let me give you the real picture.

**What Dividends Are**

When a company pays a dividend, it distributes cash directly to shareholders. Typically quarterly. Expressed as a yield — a $50 stock paying $2/year has a 4% dividend yield.

You can build a portfolio of dividend-paying stocks or funds. VYM (Vanguard High Dividend Yield ETF, expense ratio 0.06%) and SCHD (Schwab US Dividend Equity ETF, expense ratio 0.06%) are the two most popular dividend ETFs.

**The Misconception**

Here's what dividend investors often miss: dividends are not free money. When a company pays you a $1 dividend, the stock price drops by approximately $1 on the ex-dividend date. You're not richer — you've just moved money from the stock column to the cash column.

Total return = price appreciation + dividends. High-dividend stocks often have lower price appreciation. Low-dividend or no-dividend stocks (most growth stocks) reinvest that cash into the business, generating price appreciation instead.

Mathematically, $1 in dividends vs $1 in price appreciation are equivalent before taxes. After taxes, dividends are actually slightly worse — you pay taxes on dividends in taxable accounts every year whether you want the cash or not. Capital gains are only taxed when you sell.

**When Dividend Investing Makes Sense**

- Retirement income: If you genuinely need cash flow from your portfolio, dividends provide it without needing to sell shares. Psychologically easier for many retirees. - DRIP (Dividend Reinvestment Plans): Automatically reinvest dividends back into the stock. Over decades this compounds nicely. - Taxable accounts in retirement, lower income: Qualified dividends are taxed at 0% for single filers with income under ~$47,000 in 2026. That's favorable.

**For Beginners**

Don't build your strategy around dividends in the accumulation phase (while you're working and saving). VTI has a ~1.4% dividend yield and grows. SCHD has a ~3.5% yield but somewhat lower total return historically. In a Roth IRA, the distinction barely matters. In a taxable account, VTI's lower yield means less tax drag.

Focus on total return. Dividends are a component of that, not a separate thing to optimize for.

If you've never looked at a stock quote before, here's what all those numbers mean.

12How to Read a Stock Quote

If you've never looked at a stock quote before, here's what all those numbers mean.

Pull up any stock — let's say Apple (AAPL). You'll see:

**Price**: The current market price per share. What you'd pay if you bought it right now at market price.

**Change / % Change**: How much the price moved from yesterday's closing price. AAPL +1.23 (+0.58%) means up $1.23 or 0.58% since yesterday's close.

**Market Cap**: Total value of the company. Price × shares outstanding. This tells you the company's size — mega cap (>$200B), large cap ($10B-$200B), mid cap ($2B-$10B), small cap (<$2B).

**52-Week High/Low**: The highest and lowest price the stock traded at over the past year. Gives context for whether the current price is near the top or bottom of its recent range.

**P/E Ratio (Price-to-Earnings)**: Price per share divided by earnings per share. If a stock trades at $100 and earned $5 per share last year, P/E is 20x. It means you're paying $20 for every $1 of annual earnings. Higher P/E = the market expects more future growth. S&P 500 long-run average P/E is around 16-17x. A P/E of 35 implies significant expected growth.

**EPS (Earnings Per Share)**: Net income divided by shares outstanding. How much the company earns per share.

**Dividend Yield**: Annual dividend / current price. A $50 stock paying $1.50/year in dividends has a 3% yield.

**Volume**: Number of shares traded today. High volume on a price move = more conviction. Low volume = could be noise.

**Average Volume**: Normal daily trading volume. Compares to today's volume.

**Beta**: How volatile the stock is relative to the market. Beta of 1.0 = moves with the market. Beta of 1.5 = 50% more volatile than market. Beta of 0.5 = half as volatile.

**For index fund investors, most of this doesn't matter day-to-day.** You buy VTI, you're buying all of this complexity aggregated. The price you see is just what the fund is worth today. Check it quarterly at most.

13Common Beginner Mistakes That Cost Real Money

I've seen these over and over. Some of them cost people years of compounding. None of them are things you have to experience firsthand.

**Mistake 1: Trying to Time the Market**

This is the big one. "I'll invest when it goes back down a bit." "I'm going to wait until after the election." "It seems like a bad time."

The market always seems like a bad time to someone. There is always a reason to wait. And yet the market has gone up over any long enough time period. Every dollar you kept in cash waiting for a better entry point is a dollar that missed that growth.

Does market timing ever work? Yes. Is it consistently reproducible? No. Even professional fund managers fail to time the market reliably. The data is brutal on this: just be invested.

**Mistake 2: Panic Selling During Downturns**

Markets go down. Not sometimes — regularly. A 10% correction happens roughly every 16 months on average. A 20% bear market happens every few years. A 30-50% crash (2008, 2020) happens once or twice per decade.

Selling during a crash locks in losses and almost always means you miss the recovery. The S&P 500 dropped ~34% in February-March 2020. It fully recovered by August 2020 — five months. People who sold in March and waited for it to 'stabilize' before buying back in either bought back higher or missed most of the recovery.

The right move during a crash is boring: do nothing. Or if you can — buy more.

**Mistake 3: Not Diversifying**

Putting 80% of your portfolio in one stock because you 'believe in the company' is not investing. It's a bet. Even great companies go down 50-80% during bad stretches. Ask anyone who was 80% in Meta in 2022 (down 76% peak to trough).

Total market index funds solve this problem by definition. You can't have concentration risk when you own 3,700 companies.

**Mistake 4: Ignoring Expense Ratios**

Already covered this in the ETF section but it bears repeating. A mutual fund charging 1% vs an index ETF charging 0.03% will cost you tens of thousands of dollars over a 30-year period on a meaningful portfolio. The difference in performance rarely justifies the cost. Check the expense ratio on everything you own.

**Mistake 5: Not Contributing to the 401k Match**

I have no patience for this one. If your employer will match 50% of your contributions up to 6% of salary, and you're contributing 3% instead of 6%, you are literally declining part of your compensation. It's like saying 'no thanks' to a raise. There is no rational justification for this.

**Mistake 6: Checking Your Portfolio Too Often**

This sounds like a weird mistake but hear me out. The more often you check, the more noise you see, and the more emotional decisions you make. Daily fluctuations mean nothing for a long-term investor. If you check your portfolio every day, you're creating opportunities to panic or get overconfident based on information that shouldn't affect your strategy.

Check quarterly. Or set it up and look at it annually. Either is fine.

**Mistake 7: Holding Too Much Cash**

'Emergency fund' is necessary and good — three to six months of expenses in a high-yield savings account. Beyond that, cash is a slowly depreciating asset. People hold cash because it feels safe. It's not safe — it's losing purchasing power to inflation. Invest it.

**Mistake 8: Chasing Last Year's Winners**

Whatever went up the most last year is not a good predictor of what will go up the most next year. In fact, the best-performing sector of one year tends to revert toward the mean. Buying crypto ETFs in November 2021, cannabis stocks in 2019, or dot-com stocks in 1999 all felt like momentum. Chasing momentum into single sectors or themes is how people blow up their portfolios.

**Mistake 9: Waiting Until Everything Is Perfect**

Waiting until you understand everything perfectly before investing means waiting forever. The market doesn't pause while you get ready. Start with a small amount, learn by doing, improve over time. A $100 position in VTI is better than a $0 position accompanied by 200 hours of research.

14Bonds and Fixed Income Basics

Bonds confuse more beginners than they should. Let me simplify them.

When you buy a bond, you're lending money to a borrower — a government, a city, or a company. They pay you interest (the coupon rate) for the duration of the loan, then return your principal at maturity.

A 10-year Treasury bond at 4.5% means: you lend the US government $1,000, they pay you $45/year for 10 years, then return $1,000 at the end.

**Key Relationship: Interest Rates and Bond Prices Move Opposite**

This trips people up. When interest rates go up, existing bond prices go down. Why? Because your 4% bond is less attractive when new bonds are paying 5%. The market discounts its price until the yield is competitive.

This is why bonds got destroyed in 2022 — the fastest rate hiking cycle in decades caused bond prices to fall dramatically. BND (the Vanguard Total Bond ETF) dropped about 15% in 2022. Not the 'safe' performance people expected.

**Types of Bonds**

*US Treasuries*: Backed by the full faith and credit of the US government. Basically zero default risk. Current yields (as of early 2026) are in the 4-4.5% range depending on maturity.

*Corporate bonds*: Issued by companies. Higher yield than Treasuries but with default risk. Investment-grade corporates (like Apple, JPMorgan) are low default risk. High-yield bonds (junk bonds) pay more but carry real default risk.

*Municipal bonds*: Issued by state/local governments. Interest is usually exempt from federal income tax — more attractive for high earners in taxable accounts.

*TIPS (Treasury Inflation-Protected Securities)*: Principal adjusts with inflation. Real yield (above inflation) rather than nominal yield. Good hedge against inflation in your fixed income allocation.

**BND vs Individual Bonds**

For most investors, BND (or its mutual fund equivalent, VBTLX) is the right answer. It holds thousands of bonds across different maturities and credit qualities. 0.03% expense ratio. Liquid, diversified, auto-rebalancing. Don't pick individual bonds unless you're sophisticated about fixed income and have a specific reason.

**When Should You Own Bonds?**

- Young investors (under 40): Minimal or none, unless you have specific short-term goals - Pre-retirement (50s): Start adding, 15-25% allocation reasonable - At retirement: 30-50% depending on your income needs and risk tolerance - In taxable accounts: TIPS or munis might be preferable to reduce tax drag

Bonds aren't exciting. They're not supposed to be. They're the anchor that keeps your portfolio from swinging wildly when markets get volatile.

15T-Bills as a Savings Alternative — When 4%+ Risk-Free Makes Sense

T-bills (Treasury bills) are short-term US government debt — maturities ranging from 4 weeks to 52 weeks. And right now they're genuinely competitive with what you'd earn investing in bonds, while taking essentially no risk.

As of early 2026, 3-month T-bills are yielding in the 4%+ range. Compare that to: - Average bank savings account: 0.46% - Online HYSA (high-yield savings accounts): 4-5% - Money market funds: similar range

**How to Buy T-Bills**

*TreasuryDirect.gov*: Buy directly from the US Treasury. No fees. Minimum $100. The interface is dated and clunky but it works.

*Through your brokerage*: Fidelity, Schwab, and Vanguard all let you buy T-bills like any other security. Easier interface. Can set up automatic rollovers.

*T-bill ETFs*: SGOV (iShares 0-3 Month Treasury Bond ETF, expense ratio 0.09%) and BIL (SPDR Bloomberg 1-3 Month T-Bill ETF, expense ratio 0.1356%) offer T-bill exposure with the ease of a regular ETF trade. Slight yield drag from expense ratios but very convenient.

*Money market funds*: SPAXX (Fidelity) and VMFXX (Vanguard) are money market funds that invest primarily in T-bills and short-term government securities. Most brokerages sweep uninvested cash into these automatically.

**State Tax Advantage**

Interest from Treasury securities is exempt from state and local income tax. If you live in a high-tax state (California, New York, New Jersey), this makes T-bills more attractive than a HYSA paying the same rate — the after-tax yield is higher.

**When T-Bills Make Sense**

- Emergency fund beyond what you need instantly accessible: 3-6 months in T-bills or money market is reasonable - Saving for a specific goal in 1-3 years (down payment, car, etc.): T-bills give you yield without stock market risk - Short-term cash you're deploying slowly: better than sitting in a 0.01% checking account

T-bills are NOT a substitute for long-term investing. At 4%, you're roughly keeping up with inflation. You're not building wealth. But for the cash you need to keep safe and liquid, they're the right tool.