1You're Not Alone (And the Numbers Are Worse Than You Think)

Total consumer debt in the U.S. just hit $18.8 trillion. That's not a typo. Trillion, with a T, at the end of 2025 — and it breaks down to roughly $105,000 per household when you do the math.

Here's how the average American's debt actually stacks up right now:

- **Mortgage**: $104,000+ (median balance on active mortgages is higher, but this is the per-household average across all households) - **Auto loans**: $24,602 (Experian Q3 2025 data) - **Credit cards**: ~$6,000 (average balance per cardholder) - **Student loans**: ~$38,000 (average federal borrower)

And those are averages. Plenty of people are sitting on $200K+ in combined debt wondering how they got here. If that's you — cool, let's work through it.

Before diving into tactics, one thing worth understanding: not all debt is created equal. A 2.8% mortgage from 2020 that you can still refinance or pay extra on is a completely different problem from a $9,000 credit card at 24.99% APR. The math matters. The order you attack it matters. And the emotional reality of carrying debt — the anxiety, the avoidance, the late-night Google spirals — matters too.

This guide covers everything from basic payoff math to negotiating directly with creditors to what actually happens when you file bankruptcy. Pick the section that fits where you are.

2The Real Cost of Doing Nothing

Let's do one piece of math before anything else, because it changes the way you think about urgency.

You have $8,000 on a credit card at 22% APR. You make minimum payments — let's say they start at $200/month and scale down as the balance drops, which is how minimums work.

How long does it take to pay off? **27 years.** Not a typo. Twenty-seven years.

Total interest paid over that period: **$14,423.** You borrowed $8,000 and paid back $22,423.

Now here's what changes if you pay $350/month instead: - Payoff: **2 years, 8 months** - Total interest: **$1,916** - Interest saved: **$12,507**

That $150/month difference saved you over twelve thousand dollars. That's a used car. That's a year of rent in a lot of markets. That's real money that stays in your pocket instead of going to a bank that already made plenty off you.

This is why minimum payments are basically a trap. Not a conspiracy — just math. The banks structure them that way because it maximizes revenue. Now you know. Let's not play by those rules.

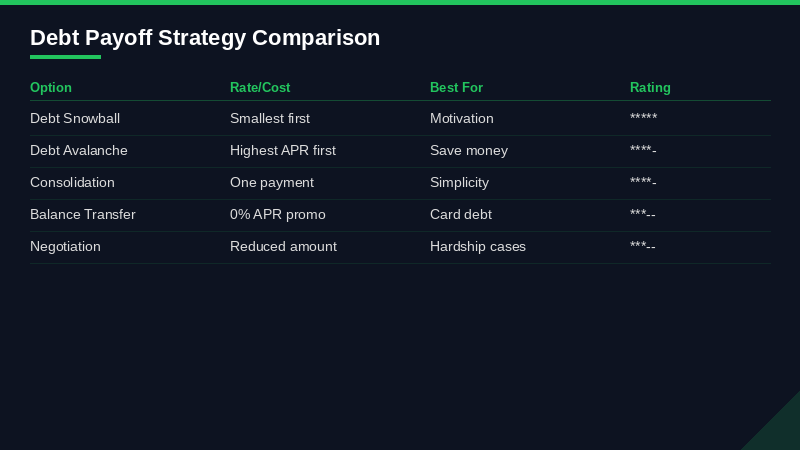

3Debt Snowball vs. Debt Avalanche — Which One Actually Works

Two strategies dominate the debt payoff world, and people argue about them constantly. Here's the honest take on both.

**Debt Avalanche**: Pay minimums on everything, throw every extra dollar at the highest-interest debt first. When that's paid off, roll those payments to the next highest rate. Mathematically optimal — saves the most money in interest.

**Debt Snowball**: Pay minimums on everything, throw every extra dollar at the smallest balance first. When that's paid off, roll those payments to the next smallest. Dave Ramsey made this famous. It's not optimal mathematically but it's extremely effective psychologically because you get wins fast.

Here's a real comparison. Say you have 5 credit cards and $500/month to throw at debt beyond minimums:

| Card | Balance | APR | Min Payment | |------|---------|-----|-------------| | Store Card | $1,200 | 29.99% | $35 | | Chase Freedom | $3,400 | 22.49% | $85 | | Citi Double Cash | $5,100 | 19.99% | $128 | | Discover It | $7,200 | 17.99% | $180 | | BofA Cash Rewards | $9,800 | 15.99% | $245 |

**Total minimum payments**: $673/month. You've got $500 extra = $1,173 total to work with.

**Avalanche results** (highest APR first — Store Card → Chase → Citi → Discover → BofA): - Total payoff time: **38 months** - Total interest paid: **$7,840**

**Snowball results** (smallest balance first — Store Card → Chase → Citi → Discover → BofA — same order in this case, actually): - Total payoff time: **38 months** - Total interest paid: **$8,210**

Difference: **$370 in favor of avalanche.** In this particular example the order is almost the same (the smallest debt also has the highest rate), so the gap is small. In cases where they diverge more — like if your biggest balance also had the highest rate — avalanche wins by more.

But here's the real talk: if the avalanche feels abstract and you blow the budget in month 4 because you haven't paid off a single card yet, you lose way more than $370. The snowball keeps you in the game. I've seen people stick with snowball for 3 years and become completely debt-free. I've seen people start avalanche, get bored, give up, and gain back $5,000 in new charges.

**Pick the one you'll actually do.** Both beat minimum payments by a mile.

Balance transfers are one of the most powerful — and most misused — debt tools available.

4Balance Transfers: 21 Months at 0% Is a Real Weapon If You Use It Right

Balance transfers are one of the most powerful — and most misused — debt tools available. Done right, you basically freeze the interest clock on your credit card debt and pay it down with 100% of your payments going to principal.

Done wrong, you kick debt down the road and end up with more.

Let's talk about what's actually available right now (March 2026):

**Citi Simplicity Card** - 0% intro APR: **21 months** on balance transfers - Transfer fee: 3% for transfers made in first 4 months, then 5% - Regular APR after intro: variable, 18.49%–29.24% - No late fees, no penalty APR (hence "Simplicity")

**Wells Fargo Reflect Card** - 0% intro APR: **21 months** on balance transfers - Transfer fee: 5% (minimum $5) - Regular APR after intro: variable - Transfers must be made within 120 days to qualify for intro rate

**BankAmericard Credit Card** - 0% intro APR: **21 billing cycles** on balance transfers - Transfer fee: 5% - Regular APR after intro: 14.99%–25.99% - Transfers must be made within first 60 days

**Here's the actual math on a balance transfer:**

You have $8,000 at 22% APR. You transfer to Citi Simplicity.

- Transfer fee (3%): $240 - New balance: $8,240 - 21 months to pay it off interest-free - Required monthly payment to clear it: **$392/month** - Total cost if you pay it off in time: **$8,240** (versus $14,423+ if you'd kept paying minimums at 22%) - Savings vs. doing nothing: **$6,000+**

$240 in fees to save $6,000 in interest. That math is obvious.

**But there are traps.** A lot of them.

**Trap 1 — Not paying it off before the intro period ends.** If you transfer $8,000 and only pay off $5,000 before 21 months is up, the remaining $3,000 gets hit with the regular APR (often 20%+) — sometimes retroactively on all interest waived during the promo period. Read the fine print on this.

**Trap 2 — New purchases.** Some cards apply your payments to the lowest-rate balance first, meaning if you make new purchases on the card, your payments chip away at those (at 0%) while the old transferred balance accrues interest. Just don't use the balance transfer card for purchases.

**Trap 3 — Opening too many cards.** Each application hits your credit with a hard inquiry. If you're planning to apply for a mortgage in the next 12 months, be careful here.

**Step-by-step balance transfer strategy:** 1. Add up the balances you want to transfer 2. Pick a card with 0% intro APR — ideally no annual fee 3. Apply only if your credit score is 670+ (most of these require good to excellent credit) 4. Transfer within the stated window (60–120 days depending on the card) 5. Divide the transferred balance by the number of promo months and set up that exact autopay 6. Set a calendar reminder 2 months before the promo ends 7. Do not use the card for new purchases 8. If you can't pay it off in time, consider a second balance transfer — but that second-transfer fee eats into savings

If you've got $5,000–$15,000 in high-rate credit card debt and decent credit, a balance transfer is probably the single highest-ROI move you can make right now.

5Debt Consolidation Loans — When They Make Sense and When They Don't

Debt consolidation loans are personal loans you take out to pay off multiple debts — credit cards, medical bills, whatever — and then pay back the single loan at (hopefully) a lower interest rate.

The math works like this: if you have $15,000 in credit card debt at an average of 21% APR, and you can get a personal loan at 11% for 4 years, you save a meaningful amount of money and simplify your life down to one payment.

**When consolidation loans actually make sense:**

- Your credit score is 680+ (otherwise you won't qualify for rates low enough to make it worth it) - You have steady income (lenders want to see DTI below ~40%) - The loan rate is materially lower than your current debt rates — and I mean materially, not 2% - You commit to not recharging the credit cards you pay off (this is where it breaks down for most people)

**Current personal loan rates (March 2026, for reference):**

| Credit Score Range | Typical APR Range | |-------------------|-------------------| | 720–850 (Excellent) | 8%–14% | | 680–719 (Good) | 14%–20% | | 620–679 (Fair) | 20%–28% | | Below 620 | 28%–36%+ |

So if you have fair credit and you're consolidating 22% credit card debt into a 25% personal loan... that's not consolidation. That's just moving the same problem around.

**The trap everyone falls into:** You consolidate $12,000 onto a personal loan. Six months later the credit cards (now zeroed out) have $8,000 of new charges on them. You've turned a $12,000 problem into a $20,000 problem. This isn't theoretical — it's extremely common.

If you consolidate, cut up the cards or reduce the limits immediately. Leave one for emergencies with a $500 limit. Don't negotiate with yourself on this.

**Where to look for consolidation loans:** - LightStream (part of SunTrust/Truist) — competitive rates for excellent credit - SoFi — good for borrowers with stable income and good scores - Marcus by Goldman Sachs — no fees, solid rates - Discover Personal Loans — fixed rates, good customer service - Your local credit union — often better rates than banks for members

Always compare APR, not just the monthly payment. A 5-year loan at 14% looks cheaper per month than a 3-year loan at 12%, but you pay more total. Run the full-cost math.

6Student Loans in 2026: What Actually Exists Now

The student loan landscape shifted again. Here's the honest status as of early 2026 — not the political spin, just what's available and what it costs.

**The SAVE Plan situation:** SAVE (Saving on a Valuable Education) is effectively dead. Federal courts blocked it in 2024, the Education Department proposed a settlement to formally terminate it in December 2025, and new enrollments are not happening. If you were on SAVE, you've likely been moved to a general forbearance while the legal situation resolves — which means no payments required but interest may or may not be accruing depending on the specific status.

**What's actually available:**

**IBR (Income-Based Repayment)** - For loans before July 2014: 15% of discretionary income, 25-year forgiveness - For loans after July 2014: 10% of discretionary income, 20-year forgiveness - Discretionary income = AGI minus 150% of federal poverty line - Qualifies for PSLF

**Real IBR payment examples** (single borrower, 2026 poverty guidelines):

| Income (AGI) | IBR Payment (10%) | IBR Payment (15%) | |-------------|-------------------|-------------------| | $35,000 | $132/month | $198/month | | $50,000 | $257/month | $385/month | | $65,000 | $382/month | $573/month | | $80,000 | $507/month | $760/month |

*Assumes single filer, family size 1, 2026 federal poverty level ~$15,060*

**ICR (Income-Contingent Repayment)** - 20% of discretionary income OR what you'd pay on a 12-year fixed plan — whichever is less - 25-year forgiveness - Qualifies for PSLF - Available for Parent PLUS loans (after consolidation)

**RAP (Repayment Assistance Plan) — Coming 2028** A new plan signed into law July 4, 2025 that will replace SAVE, PAYE, and ICR by July 1, 2028. RAP will use a sliding scale based on income. Details are still being finalized by the Department of Education.

**Standard 10-Year Plan** If you can swing it, this is still the best deal long-term. You pay more monthly but pay dramatically less total interest. On $38,000 at 6.5% interest, your monthly payment is ~$431 and total interest paid is ~$13,700.

On IBR at $50K income? You pay $257/month but over 20 years you'll pay much more in total — and any forgiven amount at the end is taxable as income (except PSLF, which is permanently tax-free).

**PSLF (Public Service Loan Forgiveness)** - 120 qualifying payments (10 years) while working full-time for a qualifying employer - Qualifying employers: government at any level, 501(c)(3) nonprofits, some other public service organizations - Must be on a qualifying repayment plan (IBR, ICR, PAYE all qualify) - Forgiven amount is **tax-free** — this is huge - Actual qualifying payment track record must be submitted via the PSLF Form annually

If you work in public service, PSLF is one of the best financial deals available to you. A doctor at a nonprofit hospital with $200K in med school debt who earns $180K can have massive balances forgiven tax-free after 10 years of IBR payments. The numbers are staggering.

**Student Loan Refinancing** Refinancing federal loans into a private loan can lower your rate but permanently strips you of federal protections: income-driven repayment, PSLF eligibility, deferment options, potential forgiveness. It's a one-way door.

Refinancing makes sense **only if**: - You work in the private sector (no PSLF) - You have stable income and no plans to use IDR - You have strong credit (700+) and can qualify for rates meaningfully below your federal rate - Your balance is manageable enough that you don't need IDR as a safety net

Current refi rates for strong credit borrowers run 5.5%–8% on fixed terms. If your federal rate is 7.5% and you can refi to 5.5% on a 10-year fixed, that's real savings — maybe $3,000–$8,000 depending on balance. Just know what you're giving up.

**The default cliff:** Student loan delinquency is at 9.6% for 90+ day defaults as of Q4 2025. If you've stopped paying and haven't enrolled in IBR, call 1-800-4-FED-AID (1-800-433-3243) today. Federal loans in default can be rehabilitated through a 9-month program — it removes the default notation from your credit report.

7How to Negotiate With Creditors (Scripts, Real Numbers, What Actually Works)

Most people don't know you can negotiate directly with your own creditors. You absolutely can. And you don't need a debt settlement company to do it — in fact, for most people, doing it yourself saves money and avoids the scams that dominate that industry.

**Who to call and when:**

Different types of creditors have different policies:

- **Original creditor (still owns the debt)**: Most willing to negotiate hardship plans, temporarily reduced rates, or settlements if the debt is 90–180 days past due. They want to avoid selling the debt for pennies on the dollar. - **Debt collector (bought your debt)**: Bought it for 3–15 cents on the dollar. Even settling at 40–50% is profitable for them. More flexible than you'd think. - **Medical debt (hospital or provider)**: Often has separate financial assistance departments. Very different conversation.

**Settlement percentages — real numbers:**

For credit card debt that's significantly past due (90+ days), typical settlement ranges are: - **Original creditor**: 40–60% of outstanding balance - **Debt buyer/collector**: 25–50% of outstanding balance (they paid less for it) - **For very old debt (2–4 years)**: Sometimes 20–30%

These aren't guaranteed, but they're realistic starting points backed by what actually gets accepted.

**The negotiation — step by step:**

**Step 1: Know your situation before you call.** What's the balance? What can you actually pay right now, as a lump sum? Collectors strongly prefer lump sums over payment plans because payment plans default. If you can come with cash in hand (or in your bank account), you have leverage.

**Step 2: Get the right person.** Call the main number and ask for the "hardship department" or "debt resolution team." Don't waste time with a front-line rep who has zero authority to negotiate. If they say they don't have one, ask to speak with a supervisor or someone in the "account resolution" group.

**Step 3: The script.**

> "Hi, I'm calling about account [number]. I've been going through a financial hardship and I want to resolve this account, but I'm not in a position to pay the full balance. I have [X dollars] available right now as a one-time payment. I'm trying to understand what options might be available to settle this account."

Then stop talking. Let them respond. Don't say anything more about your situation than that. Don't mention how much you actually have in your bank account. Don't act desperate.

**Step 4: Their counteroffer.** They'll probably come back with something like "We can settle for 75%." You say:

> "I appreciate that. I really am trying to resolve this and I want to make it easy. But right now I can only do [your number — start lower than you're willing to go]. Is there anything you can do to make that work?"

**Step 5: Get it in writing before you pay.** Non-negotiable. Before you give any banking information or make any payment, get a written settlement agreement that clearly states: - The account number - The settlement amount - That payment of this amount satisfies the debt in full - How the account will be reported to credit bureaus

Email is fine. "Text me the settlement details" is fine. Just don't pay before you have something in writing.

**Step 6: The credit reporting ask.** Ask them to report the account as "Paid in Full" rather than "Settled" or "Settled for Less Than Full Balance." They won't always agree, but it doesn't hurt to ask and sometimes they will.

**Tax trap on forgiven debt:** If a creditor forgives $600 or more, they're required to send you a 1099-C and report it as income to the IRS. You'll owe income taxes on the forgiven amount as if it were income. On a $5,000 settlement where they forgave $3,000, that's potentially $600–$900 in taxes depending on your bracket. Know this going in. There's an insolvency exemption if your liabilities exceeded your assets at the time of the forgiveness — talk to a tax pro if the numbers are large.

Debt settlement companies charge you to do exactly what you can do yourself — negotiate with creditors.

8Debt Settlement Companies — The Brutal Honest Truth

Debt settlement companies charge you to do exactly what you can do yourself — negotiate with creditors. The problem isn't just the fees. It's the model.

**Here's how the model works:**

1. You stop paying your creditors (they tell you to do this to make yourself a more attractive settlement candidate) 2. You deposit money monthly into a dedicated escrow account 3. Over 2–4 years, as accounts charge off and get sold to collectors, they negotiate settlements 4. They take 15–25% of your enrolled debt as their fee — often paid before your debts are settled

**The real costs:**

- Your credit score gets destroyed during the non-payment period — we're talking 100–150 point drops - You can get sued by creditors while you're in the program (this happens regularly) - You'll owe taxes on forgiven amounts - Programs often take 3–4 years and not all debts get settled - Fees on $30,000 enrolled debt: $4,500–$7,500 in just program fees, before any interest or legal costs

**Who it might make sense for:**

Debt settlement is worth considering if you have $20,000+ in unsecured debt (credit cards, medical bills, personal loans), you're already significantly delinquent, and you genuinely cannot afford any payment plan. In that situation — where the alternative is bankruptcy — it's a tool worth understanding.

But for most people who can still afford some payment, it's a destructive path.

**Red flags for scam companies:** - Guarantees specific results ("We'll settle for 50%!") — no one can guarantee that - Upfront fees before any debt is settled (illegal under FTC rules for telemarketing) - Claims to be a nonprofit but charges heavy fees - Pressure to sign up same-day

**Legitimate resources:** The NFCC (National Foundation for Credit Counseling) at nfcc.org connects you with nonprofit credit counselors who charge sliding-scale fees and offer Debt Management Plans — these are different from settlement, involve paying the full principal at reduced interest rates, and don't trash your credit the same way.

9Bankruptcy — What It Actually Looks Like From the Inside

Bankruptcy has a stigma that makes people avoid it past the point where it's the right answer. It's a legal process that exists specifically because sometimes people genuinely can't pay their debts and need a structured way out. It's not moral failure. It's a financial tool.

That said, it has real consequences and you should know what you're walking into.

**Chapter 7 — Liquidation**

Chapter 7 wipes out most unsecured debt (credit cards, medical bills, personal loans) in about 3–6 months. It's fast. The trade-off: a trustee can sell your non-exempt assets to pay creditors.

But in practice, most Chapter 7 filers are "no-asset" cases — meaning everything they own is protected by exemptions and creditors get nothing. The typical person filing Chapter 7 has minimal savings, an older car, and a rented apartment. There's often nothing for creditors to take.

**What you keep (federal exemptions, updated April 2025):** - Homestead: up to $27,900 (or more under state exemptions — some states are unlimited) - Vehicle: up to $4,450 - Household goods/furniture: up to $700 per item - Retirement accounts: 401(k), IRA — generally fully exempt - Tools of the trade: up to $2,800

Many states have their own exemption schemes that are more generous — Texas and Florida, famously, have unlimited homestead exemptions.

**The means test:** To qualify for Chapter 7, your income must be below your state's median income for your household size, OR you must pass a more detailed means test showing you don't have enough disposable income to fund a Chapter 13 plan.

2026 income limits vary by state and household size — for a single person in Texas, roughly $65,000. For a family of 4 in California, $135,000+. These are ballpark figures; the actual means test uses a 6-month income average.

**What Chapter 7 does NOT discharge:** - Student loans (with narrow hardship exceptions) - Alimony and child support - Most tax debts - Debts from fraud - Recent tax penalties

**Chapter 13 — Reorganization**

Chapter 13 is a 3–5 year repayment plan under court supervision. You keep all your property (including things that might get sold in Chapter 7) but you pay back some or all of your debt through the plan.

It makes sense if: - You earn too much to qualify for Chapter 7 - You're behind on a mortgage and want to catch up through the plan (Chapter 13 can stop foreclosure) - You have non-exempt assets you want to keep - You have debts that can't be discharged in Chapter 7 that you want to restructure

**The recovery timeline:**

Chapter 7 stays on your credit report for **10 years**. Chapter 13 stays for **7 years**.

But — and this is important — credit starts recovering faster than most people expect if you start rebuilding immediately. Many people with a Chapter 7 filing have credit scores in the 640–680 range within 2 years by getting a secured credit card, keeping utilization low, and paying everything on time.

**Cost of filing:** - Chapter 7 filing fee: $338 - Chapter 13 filing fee: $313 - Attorney fees: $1,000–$3,500 for Chapter 7, $3,000–$6,000+ for Chapter 13

You can file pro se (without an attorney) but it's genuinely complicated and mistakes can get your case dismissed. If you can't afford an attorney, look for legal aid organizations in your area — many take bankruptcy cases for low-income filers.

**One more thing:** there's an automatic stay that kicks in the moment you file. All collection calls, wage garnishments, foreclosure proceedings, and lawsuit efforts must stop immediately. If you're being garnished or are close to foreclosure, filing buys you time even if you eventually don't go through with it (though dismissing voluntarily has implications).

10Medical Debt: You Have More Rights Than You Probably Know

Medical debt is a $200 billion problem in this country and most people don't know how to fight it. Here's what you can actually do.

**The credit report situation (complicated as of 2026):**

The three major credit bureaus — Equifax, Experian, and TransUnion — voluntarily agreed in 2022 to remove paid medical debts and medical debts under $500 from credit reports. That's still in effect.

The CFPB tried to go further in 2025 with a rule banning all medical debt from credit reports. A federal judge struck it down. So as of early 2026, the rule that medical debts under $500 don't appear on reports and paid medical bills don't appear is the operative standard. Bills over $500 that are unpaid can still appear.

State laws vary significantly — 15+ states have passed their own protections banning medical debt from credit reports entirely.

**The No Surprises Act:** Passed in 2022, this law protects you from surprise bills for emergency services from out-of-network providers. If you get billed for emergency care from an out-of-network ER doc who treated you at an in-network hospital, that's a potential NSA violation. The CFPB has stated that collecting debts barred under the NSA may violate the FDCPA.

What to do: if you got a surprise bill for emergency services, file a complaint at NoSurprises.HHS.gov and dispute it with the hospital billing department explicitly citing the No Surprises Act.

**Charity care:** Every nonprofit hospital (and many for-profit ones) has a financial assistance or charity care program. By IRS rules, nonprofit hospitals must maintain and publicize these programs — it's part of their tax-exempt status.

For low-to-moderate income patients, charity care can mean: - Full write-off of the bill (below 200% of poverty line at many hospitals) - Significant discounts (50–80%) for those above that threshold - Interest-free payment plans

How to access it: Ask to speak with a patient financial advocate or billing department. Request the hospital's "Financial Assistance Policy" by name — they're required to give it to you. Apply before the bill goes to collections. Most hospitals will still accept charity care applications even after a bill goes to collections; call and ask.

**Negotiating medical bills directly:** Hospital chargemaster prices (what they bill) are often 3–5x what insurance companies actually pay. If you're uninsured or paying out of pocket: - Ask what they'd accept from your state's Medicaid program — that's the floor - Ask for the "prompt pay discount" or "self-pay rate" — many hospitals have a standard 20–40% discount for patients paying in full at time of service - For larger bills, make a settlement offer similar to credit card negotiation — hospitals often settle past-due accounts for 40–60 cents on the dollar rather than sell to a collector for 3 cents

**Payment plans:** Hospitals are generally required to offer affordable payment plans before sending accounts to collections. The standard is no more than 20% of monthly income. Push back if they offer you a plan you can't afford — ask specifically for their income-based payment plan.

**If it's already in collections:** Medical debt collectors are still subject to the FDCPA (Fair Debt Collection Practices Act). They can't call before 8am or after 9pm. They can't use abusive language. You can send a written request to stop contact. And you can dispute the debt if it's incorrect.

11Credit Card Debt Fast Track — Real Math on Getting Out

Let's go deeper on credit card payoff because it's where most people have the most leverage and the most pain.

We already ran the $8,000 at 22% example. Let's build a real playbook.

**The interest calculation you need to understand:**

Most credit cards compound daily. The daily periodic rate on a 22% APR card is 22% ÷ 365 = 0.0603% per day. On an $8,000 balance that's $4.82 in interest every single day you carry that balance.

$4.82 a day. $146.78 a month. Just sitting there.

This is why making extra payments mid-month actually helps — every extra payment immediately reduces the principal the daily interest calculates against.

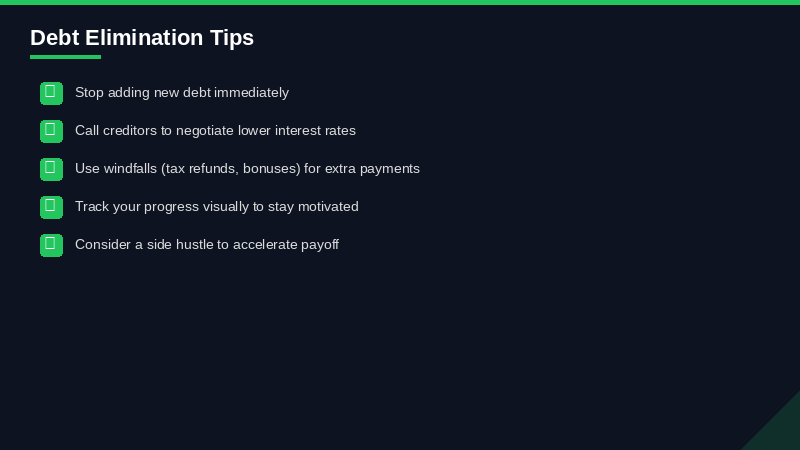

**Call and ask for a lower rate.**

Seriously. This works more often than people think. Call your credit card company, say you've been a customer for X years, you've seen promotional rates advertised and want to know if there's anything they can do. Customer retention reps at Citi, Chase, and Bank of America have the ability to temporarily lower your rate. You might get a few points knocked off for 6–12 months. On $8,000 at 22%, dropping to 17% saves you $400/year in interest.

It takes 8 minutes and it's free.

**If you have multiple cards, here's the actual optimization:**

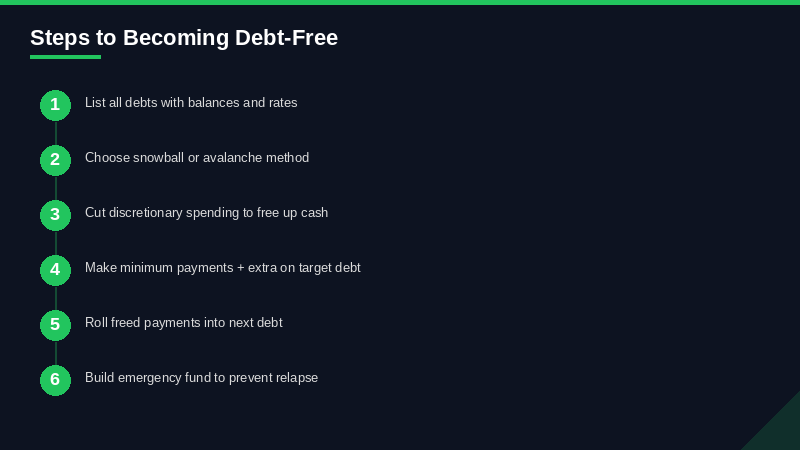

1. Stop using all the cards — freeze them in a bag of water in your freezer (old trick, works psychologically) 2. List them with current balance, APR, and minimum payment 3. Pick snowball or avalanche (see earlier section) 4. Find every extra dollar in your budget — subscriptions you don't use, food delivery that's become a habit, anything 5. Automate the minimum payments on everything 6. Manually pay the extra amount each month to your target card right after payday 7. When a card hits zero, update the spreadsheet, feel actual joy, redirect that payment to the next card

**The side income accelerator:**

Every extra $500/month you can put toward debt on that $26,700 five-card balance from our earlier example cuts 8–10 months off the payoff timeline and saves $2,000–$3,000 in interest. Sell stuff on Facebook Marketplace. Pick up one weekend shift. Freelance anything you can. The marginal return on debt repayment is guaranteed — you're earning your interest rate on every extra dollar you pay. Right now that's 20%+ on most cards. There's no investment that beats a guaranteed 20% return.

Mortgage debt is different from consumer debt in a few important ways: it's usually the lowest interest rate you have, the interest is often tax-deductible (if you itemize), and pa...

12Mortgage Payoff Strategies — When It Makes Sense to Pay Extra

Mortgage debt is different from consumer debt in a few important ways: it's usually the lowest interest rate you have, the interest is often tax-deductible (if you itemize), and paying it off early doesn't always optimize your financial position.

That said, there's a real psychological and financial case for owning your home free and clear, and these strategies work.

**Biweekly payments:**

Instead of 12 monthly payments per year, you make 26 biweekly half-payments. That's equivalent to 13 monthly payments per year — one extra payment annually with no significant budget impact.

On a $300,000 mortgage at 6.5% on a 30-year term: - Standard monthly: 30 years, $227,545 in total interest - Biweekly: **24 years and 7 months**, $178,992 in total interest - **Savings: $48,553 and 5.5 years**

You can set this up directly with most mortgage servicers. Some charge a small fee for the program — skip that, just make an extra principal payment equal to 1/12 of your monthly payment instead.

**Extra principal payments:**

Every dollar of extra principal payment saves you the full mortgage interest rate on that dollar for every remaining year of the loan. On a 6.5% mortgage with 20 years left, paying $100 extra per month saves about $3,800 in total interest and shaves 16 months off the loan.

$500/month extra on that same loan: saves $12,400 and 4.5 years.

Always designate extra payments as "principal only" — call your servicer or check the payment portal. If you just pay extra without specifying, some servicers apply it toward next month's payment (which includes interest) rather than straight to principal.

**Round up:**

If your payment is $1,847, pay $2,000. The $153 difference goes to principal every month. Over 30 years that accumulates to a surprising amount — you'd typically cut 2–3 years off the loan and save $15,000–$25,000 depending on your rate and balance. Almost no budget impact.

**Should you pay off your mortgage vs. invest?**

This is the real question and there's no universal answer. If your mortgage rate is 3.25% from 2020 and you're considering dumping extra money into it versus maxing your 401(k) or investing in index funds... the math heavily favors investing. Historical S&P 500 returns around 10% annualized beat a 3.25% guaranteed rate pretty comfortably.

But if your mortgage rate is 7.5% from 2023 or 2024, the calculation changes. And if the psychological weight of carrying a mortgage is keeping you up at night, that has real value too. Financial decisions aren't purely spreadsheet problems.

13Debt-Free Timeline: What to Expect at Different Debt Levels

Real talk on timelines. These assume you're putting a meaningful amount toward debt above minimums and making some budget changes.

**Under $10,000 in unsecured debt:** - Aggressive payoff (every extra dollar): 12–18 months - Moderate effort (some budget adjustments): 24–30 months - Tools that help: balance transfer card if you have decent credit, snowball method

**$10,000–$30,000 in unsecured debt:** - Aggressive: 2.5–4 years - Moderate: 5–7 years - Consider: balance transfer for the highest-rate portion, debt consolidation loan if credit is good, budget audit to find $300–$500/month more toward debt

**$30,000–$60,000 in unsecured debt:** - This is serious. Aggressive payoff takes 5–8 years unless income is strong. - Strongly consider a debt consolidation loan to reduce the interest drag - At this level, a nonprofit credit counselor or DMP (Debt Management Plan) through NFCC can be genuinely helpful — they negotiate reduced rates with creditors (typically 6–10%) and you make one payment to the NFCC member agency - If the debt is primarily credit cards and you're delinquent, direct negotiation becomes realistic

**Over $60,000 in unsecured debt:** - Without major income change, this is a 10+ year mountain on minimum payments - Bankruptcy (Chapter 7 or 13) deserves serious consideration — not as a failure but as a legitimate tool - Debt settlement is also on the table at this level, with eyes wide open about credit damage and taxes - A free consultation with a bankruptcy attorney costs nothing and gives you a clear picture of options

**Student loans (separate category):** - Under $30K: Standard 10-year plan is manageable for most college graduates. Pay extra when possible. - $30K–$75K: IDR (IBR) + income-focused repayment. If public sector, PSLF is probably the play. - Over $75K+: IBR/PSLF analysis becomes critical. The math on paying aggressively vs. riding IBR to forgiveness is genuinely complex and depends on income trajectory, sector, and family size. A $20 consultation with a student loan specialist (Student Loan Planner, for example) can save you tens of thousands.

14Apps and Tools That Actually Help

There's no shortage of budgeting apps. Most of them are fine. Here's the honest take on the ones specifically useful for debt payoff:

**YNAB (You Need a Budget) — $109/year** The best budgeting system for getting out of debt, period. YNAB's core philosophy — every dollar gets a job before you spend it — is exactly what debt payoff requires. You assign money to debt payments when you receive income, not when payments are due. This sounds like a small thing but it completely changes how you relate to your money.

The app connects to your accounts, tracks spending in real time, and has a genuinely good mobile app. The learning curve is real — YNAB works differently from every other budgeting app and you have to commit to learning it. First-time users who quit in week 2 don't get the results. Users who stick with it for 3+ months regularly report saving $600+ per month they didn't know they had.

Free 34-day trial, then $109/year. Worth it for most people with real debt.

**Undebt.it — Free (paid version $12/year)** This one is specifically built for the debt payoff journey. You enter all your debts, choose your strategy (snowball or avalanche), and it generates a complete payoff schedule showing exactly which debt to hit when, what your total interest cost is, and a date when you'll be debt-free.

The visual payoff plan is motivating in a way that a spreadsheet isn't. Seeing "June 2028" as your debt-free date is different from knowing it intellectually. Highly recommend for anyone who needs structure and a finish line.

**Tally — free to use** Tally is specifically for credit card debt. It analyzes all your cards, manages payment scheduling to minimize interest, and optionally offers a line of credit at a lower rate to consolidate balances. The automated payment management alone is useful — it makes sure you never miss a minimum payment (which tanks your credit and adds penalty APRs).

Note: Tally's line of credit offering requires a 670+ credit score and isn't available in all states. The free payment management tool is broadly available and genuinely useful.

**Credit Karma / Experian Free** Not specifically debt payoff tools but useful for monitoring credit score during the payoff process. Watching your score go up as balances decrease is legitimately motivating. Also useful for catching errors on your credit report, which happen more often than they should.

**A spreadsheet:** Dont overlook this. A simple Google Sheet with your debts, balances, APRs, minimum payments, and extra payment allocation is sometimes the most honest and useful tool. Nothing to subscribe to, nothing to link, just math that you control. There are dozens of free debt payoff spreadsheet templates on Google Sheets gallery.

15Building the Budget That Makes Debt Payoff Possible

Every debt payoff strategy assumes you have money to direct toward debt beyond minimums. Where does that money come from? Almost always from finding it in an existing budget.

Here's how to do a budget audit in about 45 minutes:

**Step 1 — Print or export your last 3 months of transactions.** All accounts. Don't edit.

**Step 2 — Categorize every single transaction.** Housing, food (split groceries and restaurants), subscriptions, transportation, entertainment, clothing, miscellaneous. No judgment, just data.

**Step 3 — Find the subscriptions.** Most people find $80–$200/month in subscriptions they'd forgotten about. Cancel anything you haven't used in 60 days. Don't negotiate with yourself.

**Step 4 — Look at restaurants/delivery.** This is the biggest leak in most budgets. Not because eating out is bad but because food delivery apps have dramatically increased what people spend on food without them noticing. If you're spending $600/month on Uber Eats and DoorDash, that's real money.

**Step 5 — Set a debt payoff amount first, not last.** Most budgeting advice says to allocate income, handle expenses, and put what's left toward debt. Flip that. When you get paid, immediately transfer your debt payoff amount to a separate account or make the payment. What's left is what you live on. This is "paying yourself first" applied to debt elimination.

**Step 6 — Track for 30 days.** Budget doesn't work on paper, it works when you check it in real time. The first time you look at your spending mid-month and see you've already hit your restaurant budget with 2 weeks left, that changes behavior.

Most people doing a serious budget audit find $300–$600/month they can redirect to debt without dramatically impacting quality of life. That's the engine that powers everything else in this guide.