1What a Credit Score Actually Is (And Why Everyone Gets This Wrong)

Here's the thing nobody tells you upfront: there's no such thing as 'your' credit score. Singular. There are literally dozens of versions floating around, and the number your bank sees when you apply for a mortgage is probably not the same one you checked on your phone this morning.

A credit score is a three-digit number — almost always between 300 and 850 — that's supposed to represent how likely you are to repay a debt. Lenders don't want to read through your full credit report every time someone applies for a card, so a score gives them a fast signal. One number that bundles up years of financial behavior into something a loan officer can glance at in two seconds.

The math comes from scoring models — algorithms trained on millions of borrower records that learned which behaviors predict default risk. FICO (Fair Isaac Corporation) built the dominant model back in 1989 and it's still what most lenders pull. VantageScore came along in 2006 as a joint venture between the three major bureaus — Equifax, Experian, and TransUnion — and has been chipping away at FICO's dominance since.

Here's where people get confused: your credit data lives at those three bureaus, and each bureau might have slightly different information on file about you. So even with one scoring model, you can have three different scores just from the data differences. Add in that FICO has released FICO 8, FICO 9, FICO 10, FICO 10T, and industry-specific versions (FICO Auto Score 9, FICO Bankcard Score 9, etc.), and you've got... a lot of numbers.

For most people, FICO 8 is the one that matters most. It's the version used by the largest percentage of lenders. VantageScore 3.0 is what a lot of free monitoring services show you. And FICO 10T — which incorporates 'trended data' (tracking whether your balances are going up or down over time) — is gradually getting adopted by mortgage lenders.

None of this means the system is rigged against you or whatever. It just means you should stop obsessing over the specific number on Credit Karma and focus on the behaviors that move all the models in the same direction. Because — and this is actually good news — the fundamentals are basically identical across every model. Pay on time. Keep balances low. Don't apply for everything at once. The rest is noise.

2FICO vs VantageScore: What's Actually Different

People argue about this like it's a sports rivalry. It's not that dramatic. But the differences do matter depending on where you're applying.

FICO Score 8 is the industry standard. When a mortgage lender says 'we need a 620 to qualify,' they mean FICO — specifically, they'll pull all three bureaus and in many cases use the middle score. Auto lenders use FICO Auto Scores. Credit card issuers lean heavily on FICO Bankcard Scores. The specific version varies by lender, but if a creditor is doing a real underwriting decision on a big loan, they're almost certainly paying for a FICO score.

VantageScore is what you see on free tools. Credit Karma, NerdWallet, Capital One's CreditWise — all VantageScore 3.0. Experian's free tier shows both VantageScore and FICO. Discover's free FICO score program gives you an actual FICO 8, which is why it's more useful than most.

The score range is 300–850 for both current models, so at least that's consistent. VantageScore used to go 501–990 on older versions, which caused massive confusion. Now they match.

Where they diverge:

FICO requires at least one account that's six or more months old AND at least one account reported in the last six months to produce a score. No history, no score — you're 'unscorable.' VantageScore can generate a score with just one month of credit history, which is why people who are new to credit sometimes see a VantageScore but no FICO.

FICO treats multiple inquiries for mortgage, auto, and student loans as a single inquiry if they happen within a 45-day window. VantageScore does the same but uses a 14-day window. Matters if you're rate-shopping aggressively.

Late payments: FICO 9 and VantageScore 4.0 both ignore paid-off collections. FICO 8 still counts paid collections against you. This is a real difference — if you had a collection that you settled, your FICO 8 score is still penalized, but your VantageScore 4.0 score acts like it never happened.

Medical debt specifically: FICO 9 and VantageScore 3.0+ both weight medical collections less heavily than other types. FICO 8 doesn't distinguish.

Rent and utility payments: Neither model factors these in by default — they don't show up on your credit report unless you use a service like Experian Boost or rent reporting programs. Then Experian-based scores may reflect them, but TransUnion and Equifax won't.

Bottom line: Know your FICO score before any major loan application. Track VantageScore day-to-day as a directional indicator. The gap between them can easily be 20–40 points, so don't assume the number you see for free is the number your mortgage lender sees.

3The 5 FICO Factors — Exact Weights, Real Explanations

FICO publishes the factor weights. These aren't secrets. But most explanations of them are either too vague to be useful or written by someone who clearly hasn't had to actually manage credit under pressure. Let's fix that.

Payment History — 35%

The single biggest factor. One missed payment, 30 days late, can drop a score in the 780s by 90–110 points. That's not a typo. The higher your score, the harder you fall on a missed payment — you have more 'perfection premium' to lose. Someone with a 580 score misses a payment and drops maybe 20 points. Someone with a 780 drops 90–110. Life's unfair like that.

The damage fades over time. A 30-day late from five years ago barely moves your score. A 90-day late from 18 months ago still stings. The formula weights recency heavily. Seven years is when derogatory marks fall off entirely.

If you're one day late, call immediately. Creditors can sometimes 'goodwill' remove a late payment if you have a clean history otherwise. Not guaranteed, but it works often enough to always try.

Credit Utilization — 30%

This is the ratio of your revolving balance to your revolving limit. You have a $10,000 limit card with a $3,000 balance? That's 30% utilization. FICO scores this both per-card and in aggregate across all cards.

The conventional wisdom says 'keep it under 30%.' That's wrong — or at least, it's the floor, not the target. The highest scorers typically run under 10%. Under 7% is where you see 800+ territory pretty consistently.

Key insight: utilization has no memory. Unlike payment history, your utilization score resets every single month when your statement cuts. Crush your balance this month, your score jumps next month. This makes utilization the fastest lever you have. If you need to boost your score for a loan application in 60 days, pay down revolving balances first — it's the only factor that responds that quickly.

Also: a $0 balance might actually score slightly worse than a very low balance on some models. Utilization of exactly 0% sometimes reads as 'inactive.' Keep at least one card with a tiny balance — $5–20 — and pay it off each cycle.

Length of Credit History — 15%

Three components: age of oldest account, age of newest account, average age of all accounts. FICO rewards long, stable histories.

This is the factor that makes people most anxious about closing old cards. And honestly, the anxiety is mostly justified. If you close your oldest card, you don't immediately lose that history (it stays on your report for up to 10 more years) — but eventually it will drop off and your average age goes down. For most people, keeping old accounts open and occasionally using them for a small purchase is the right call.

Opening a lot of new accounts fast drags down your average account age hard. If you're in good shape and thinking about grabbing a few new rewards cards, spread them out by at least 6 months.

Credit Mix — 10%

FICO wants to see that you can handle different types of credit responsibly. Revolving (credit cards, HELOCs) plus installment (mortgages, auto loans, student loans, personal loans). Having both types scores better than having only one type.

This factor matters less than people think. A 10% weight means you're not going to see massive swings from credit mix changes. I wouldn't take out a loan you don't need just to improve your mix. But if you're already planning to finance something, it's worth knowing that adding an installment loan when you've only had credit cards can give your score a small bump.

New Credit — 10%

Every time you apply for credit, the lender does a hard inquiry. Each hard inquiry dings your score slightly — usually 5 points or less, and the impact fades within a year. They stay on your report for two years but only actively affect scoring for 12 months.

The real problem with applying for lots of new credit isn't the inquiries themselves — it's what it signals to the model. Multiple applications in a short window pattern-matches to financial stress. The model knows that people in trouble often go on application sprees before defaulting.

Exception: mortgage, auto, and student loan inquiries within a shopping window (45 days for FICO 8) count as one. If you're buying a house and getting quotes from five lenders in three weeks, that's one inquiry impact, not five.

Soft inquiries — when you check your own score, when employers do background checks, when credit card companies do prequalification checks — never affect your score. Zero. Never. Any tool that tells you checking your score hurts it is either outdated or lying.

The FICO 8 ranges are: 800–850: Exceptional.

4Score Ranges and What They Actually Mean for Your Life

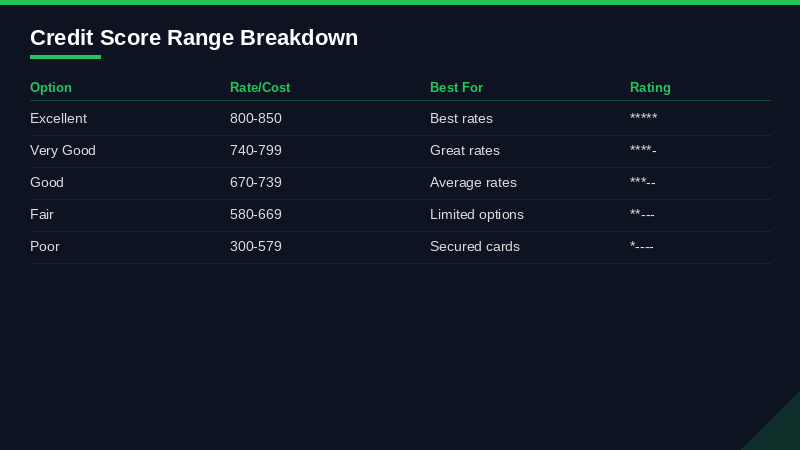

The FICO 8 ranges are:

800–850: Exceptional. You're getting the best rates available. Lenders compete for your business. These folks exist — about 21% of Americans are here as of 2025 data.

740–799: Very Good. Still excellent rates, minimal to no tier penalty versus Exceptional. Most premium rewards cards approve in this range without issue. Mortgage lenders love you.

670–739: Good. This is roughly average — median American FICO score is around 715. You'll get approved for most things but won't always snag the advertised rate. You're in the conversation.

580–669: Fair. You can still get approved for some cards, some auto loans with higher rates, and potentially FHA mortgages (FHA goes down to 580 with 3.5% down). But you're paying for it in interest.

300–579: Poor. Conventional financing is basically unavailable. Secured cards, credit builder loans, and becoming an authorized user are your primary rebuild tools.

Here's what those tiers actually cost you in dollars, not just labels:

Mortgages (30-year fixed, $400,000 loan, 2026 approximate rates): - 760–850: ~6.5% → ~$2,528/month P&I - 700–759: ~6.7% → ~$2,579/month (+$51/month, $18,360 over loan life) - 660–699: ~7.1% → ~$2,683/month (+$155/month, $55,800 over loan life) - 620–659: ~7.6% → ~$2,820/month (+$292/month, $105,120 over loan life) - Below 620: May not qualify for conventional at all. FHA has its own rate structure.

Auto loans (new car, 60 months, $35,000): - 720+: ~6.8% → ~$690/month - 690–719: ~8.5% → ~$721/month - 660–689: ~11.2% → ~$763/month - 620–659: ~14.1% → ~$815/month - Below 620: Subprime territory, 18–25%+, or outright denial

Credit cards: The spread here is brutal. Someone with 780+ gets a 20% APR card offer while someone at 600 gets 29.99% — if they get approved at all. On a $5,000 balance that you carry month-to-month, that's the difference between $83/month and $125/month in interest. Real money.

These numbers aren't meant to depress you. They're meant to make the case that spending six months actively improving your score before a major purchase is one of the highest-return activities you can do with your time. Moving from 640 to 720 before buying a house can save you six figures over the life of the loan. That's not hyperbole.

5Where to Check Your Score for Free — Actually Free, No Tricks

Let's go through the real options, because 'free credit score' is one of the most abused phrases in personal finance. Some of these require a card enrollment, some are genuinely no-strings-attached.

Credit Karma

Free, no credit card required, doesn't expire. Shows VantageScore 3.0 from TransUnion and Equifax. Updated weekly. The interface is good, the score tracker is useful, and their credit card recommendations are... aggressively monetized, but you can ignore those. The score you see here is not what your mortgage lender pulls. Use it as a directional tracker, not a ground truth.

Discover Scorecard

This one's special: it shows your FICO Score 8 based on TransUnion data. No Discover card required — you can sign up at creditscorecard.discover.com for free. Updated monthly. If you want one free service that shows you an actual FICO score, this is the one.

Experian Free Account

Experian gives you free access to your Experian credit report plus your FICO Score 8. Also shows you VantageScore. The free tier is genuinely free (they have a paid 'Experian Boost' upsell but the base account is no-cost). Updated monthly. Strong choice.

Capital One CreditWise

Free for everyone, not just Capital One customers. VantageScore 3.0 from TransUnion. Has a simulation tool that lets you model what would happen to your score if you paid off debt, opened a new card, etc. The simulator is the best part — actually useful for planning.

Chase Credit Journey

VantageScore 3.0 from TransUnion. Free for everyone — not just Chase customers. Weekly updates. Clean interface.

Wells Fargo Credit Close-Up

FICO Score 9. Wells Fargo customers only. If you bank there, this is worth checking because FICO 9 (which ignores paid collections and weights medical debt lower) can be meaningfully higher than FICO 8 for people with any collection history.

AnnualCreditReport.com

This is different from a score — this is your actual credit report from all three bureaus. Federally mandated free access. Historically once per year per bureau; during COVID they moved it to weekly and as of 2025 it's still weekly free pulls. No score here, just the full report. You want to review this at minimum once a year to check for errors, fraudulent accounts, incorrect late payments. This is the one you use to dispute stuff.

What to look for when you pull your reports: any account you don't recognize (fraud), late payments you dispute as incorrect, accounts showing wrong balances, old negative items that should have aged off (7 years for most negatives, 10 years for Chapter 7 bankruptcy).

Bank and credit union portals: A growing number of banks now show your FICO score in your dashboard. Bank of America, Citi, US Bank all offer this. If your bank has it, use it — it's usually a more specific FICO version than what free tools show.

6How to Improve Your Score Fast: 30, 60, and 90-Day Strategies

People want a magic trick. There isn't one. But there are moves that work faster than others, and there's a logical sequencing to this that most articles get wrong.

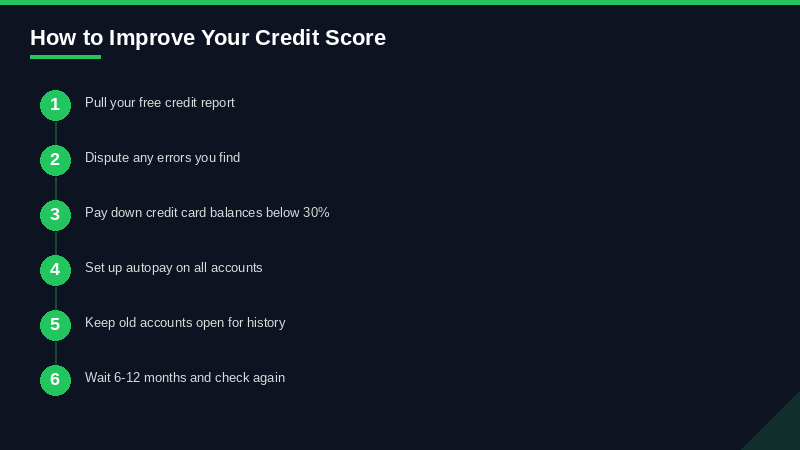

Before you do anything: pull all three credit reports from AnnualCreditReport.com and read them. Actually read them. Not just the score, the full report. You need to know what's dragging you down before you can fix it. I've seen people spending months making small optimizations while a $200 medical collection from 2019 is sitting there tanking them 50 points — something they could have disputed and removed.

First 30 Days: Fix Errors and Kill Utilization

Dispute every error you find — wrong late payments, accounts that aren't yours, balances that are incorrect. File disputes at Equifax, Experian, and TransUnion separately. They each have online dispute portals. By law they have 30 days to investigate and correct or remove the item. A single successfully removed error can move your score dramatically — sometimes 50+ points if it's a collection or a major late payment.

Same month: pay down every revolving balance as aggressively as possible. Credit card balances are the fastest-moving lever in the model. If you have $3,000 in card debt and $3,000 in savings sitting there, pay it off. I know the psychological safety of the savings cushion is real, but at 22% APR versus 4% in a savings account, you're losing money every month. Pay the cards.

If you can't pay off everything, prioritize cards that are closest to their limit. A card at 95% utilization hurts more than two cards at 30% combined — the per-card utilization component is real.

Days 30–60: Authorized User Strategy

If you have a family member or close friend with excellent credit and an old, low-utilization card, ask them to add you as an authorized user. You don't need the physical card. You don't need to ever use the account. When that account gets added to your credit report, you inherit its age, its on-time payment history, and its utilization in your aggregate numbers.

This move can add 30–50 points to a thin credit file in a single reporting cycle. For someone who's new to credit or rebuilding after a rough patch, it's one of the highest-leverage moves available. The primary cardholder's account doesn't get hurt. Their credit limit doesn't decrease. Their utilization doesn't change. It's a pure gift of credit history.

The flip side: if the primary cardholder has a late payment or maxes out after adding you, that shows up on your report too. Choose your authorized user benefactor carefully.

Days 60–90: Negotiate and Goodwill

For legitimate negative items on your report, you have more options than people think. 'Pay-for-delete' is when you negotiate with a collection agency to remove the item entirely in exchange for payment. This isn't technically supposed to be allowed under the credit reporting rules, but collection agencies do it — they're not required to report accurate information, they're just prohibited from reporting inaccurate information. Some will delete for full payment, some for a settlement, some refuse entirely. It's worth asking.

Goodwill letters to original creditors work for first-time lates. Write a letter explaining the circumstances (job loss, medical emergency, whatever) and ask nicely if they'll remove the late payment as a courtesy. Works more often than you'd think, especially if you've been a customer for years.

For active accounts with no lates: ask for a credit limit increase. If your limit goes from $5,000 to $8,000 and your balance stays the same, your utilization drops. Most issuers will do a soft pull for a limit increase request — ask first whether it'll be a hard pull. If it's soft, almost always worth doing.

Days 90+: Add Positive History

If your credit file is thin (few accounts, short history) or you're rebuilding from scratch, you need to add accounts. Two tools for this:

Secured credit cards: You deposit cash as collateral — usually $200–$500 — and that becomes your credit limit. The card reports to all three bureaus like a normal card. Use it for small purchases, pay in full each month. After 12–18 months of clean history, many issuers 'graduate' you to an unsecured card and return your deposit. Discover it Secured, Capital One Platinum Secured, and Chime Credit Builder are strong options with low or no annual fees.

Credit builder loans: Self (formerly Self Lender), Credit Strong, and many credit unions offer these. You pay monthly payments into a savings account that's locked until the loan term ends. When it's paid off, you get the money back (minus interest and fees) and you've built 12–24 months of on-time payment history. The money actually comes back to you, so the net cost is just the interest — usually $70–$120 on a 12-month loan. A reasonably cheap way to build payment history.

7The Authorized User Strategy: Full Breakdown

This one deserves its own section because it's massively underutilized and people have weird misconceptions about it.

An authorized user is someone added to another person's credit card account. The authorized user gets a card with their name on it. More importantly, the account's full history — age, payment record, utilization — shows up on the authorized user's credit report.

Who it helps most: people with thin files (under 3–4 accounts), recent credit damage, or no credit history at all. If you're 21 and just starting out, being added to a parent's 15-year-old card with a $20,000 limit and perfect payment history is like instantly inheriting a really solid credit foundation.

Who it doesn't help much: people with extensive credit histories of their own. Adding one more account to someone who already has 12 accounts with long history barely moves the needle.

Does it actually work? Yes, definitively. FICO 8 includes authorized user accounts in scoring. VantageScore does too. There was a period when FICO tried to exclude them (FICO 08 was partly designed to reduce the impact), but they backed off and AU accounts still count.

The industry that grew up around this — 'tradeline renting' — is worth knowing about and worth not using. Services will sell you access to a stranger's old account as an authorized user for $100–$300 a slot. FICO has algorithms specifically designed to detect this and they periodically penalize it. Not worth the risk, especially with a mortgage application where underwriters look at your file closely. The only AU strategy worth using is genuine family/friend relationships.

How to do it right: The primary cardholder calls their credit card company and adds you as an AU with your name and social security number. It reports to the bureaus within one billing cycle — usually 30–45 days. You can have the card mailed to their address if you don't want the physical card at all.

If you're the primary cardholder and want to help someone out: low utilization on that card and no late payments are the two things that matter. An AU spot on a card that's 90% utilized helps them almost not at all and might actually hurt them. Clean up your own card first.

Credit builder loans are a weird product when you first encounter them.

8Credit Builder Loans: How They Actually Work

Credit builder loans are a weird product when you first encounter them. You're borrowing money... but you can't spend it? Yeah. That's the deal.

Here's the mechanics: you apply for a credit builder loan (often $500–$2,000), and instead of receiving the money, it gets held in a savings account or CD. You make monthly payments — principal plus interest — for 12 or 24 months. Every payment gets reported to the credit bureaus. At the end of the term, you get the money back, minus the interest you paid.

The practical cost: a typical Self ($25/month for 24 months) loan might return you $520 on a $600 total payment — you paid $80 in interest to build 24 months of perfect payment history. That's the cost of the product. Is it worth it? For someone rebuilding with zero positive trade lines, yes, very probably.

Best options as of 2026:

Self (formerly Self Lender) — biggest name in the space, fully online, reports to all three bureaus. Plans from $25–$150/month. Their secured Visa card is also available after you hit $100 in savings, giving you a revolving account too.

Credit Strong — subsidiary of Austin Capital Bank. Strong options for building both installment and revolving history simultaneously. Their MAGNUM product is designed for people who want higher credit limit impact.

Local credit unions — often have the lowest-cost credit builder loans. Some charge no interest at all, just a small administrative fee. Worth calling your local credit union before going the fintech route.

Chime Credit Builder — technically a secured card rather than an installment loan, but works on similar principles. No hard pull, no minimum security deposit, reports to all three bureaus. If you have a Chime spending account, this is a genuinely good option.

Key thing people miss: you must actually make the payments on time. This seems obvious but the loan itself does nothing for your credit — the on-time payment history does. Missing payments on a credit builder loan is worse than not having one.

9Disputing Errors: Step-by-Step

Credit report errors are more common than most people realize. A 2021 Consumer Reports study found that 34% of Americans had at least one error on their credit report. Not all errors are score-damaging — some are just address discrepancies — but a meaningful percentage involve things like incorrect late payments, duplicate accounts, wrong balances, or accounts that aren't yours at all.

Start at AnnualCreditReport.com. Pull all three. Download or screenshot everything. You need to dispute each bureau separately where inaccuracies appear.

Step 1: Identify and document the error. Know exactly what you're disputing — the account name, account number (or partial), the specific item that's wrong, and what the correct information is. 'This late payment is wrong' isn't specific enough. 'This Discover card account shows a 30-day late in January 2024 but I have bank records showing the payment was made on time' is specific enough.

Step 2: Gather evidence. Bank statements, payment confirmation emails, receipts — whatever supports your claim. You're not legally required to provide evidence for a dispute, but providing it speeds things up enormously and improves your odds.

Step 3: File the dispute. Three ways to do this:

Online: equifax.com/personal/credit-report-services, experian.com/disputes, transunion.com/credit-disputes. Fastest, easiest, and creates a timestamp. Recommended for most people.

Mail: Certified mail, return receipt requested, to the bureau's dispute address. Slower but creates a paper trail that online submissions don't guarantee. If you're dealing with a complex situation or a dispute that might end up in court, mail is better.

Phone: Works but I don't recommend it. No written record, easy for things to get lost.

Step 4: Wait. Bureaus have 30 days to investigate (sometimes 45 if you provide additional information during the investigation period). They contact the original furnisher (the bank or collection agency) and ask them to verify the information. If the furnisher can't verify, the item must be removed or corrected.

Step 5: Check results. You'll get a response by mail or online portal. Three outcomes: removed, corrected, or 'verified as accurate' (meaning they confirmed it with the furnisher). If it's verified but you know it's wrong:

File a dispute directly with the original creditor. Sometimes the bureau takes whatever the creditor says, but the creditor's own records might actually support your case if you get someone on the phone.

File a complaint with the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov. The CFPB doesn't adjudicate disputes, but creditors pay attention when a CFPB complaint comes in.

Consult a credit attorney. Many work on contingency for Fair Credit Reporting Act (FCRA) violations. If a bureau or furnisher is knowingly reporting inaccurate information after you've disputed it, that's an FCRA violation and you have legal recourse.

Common disputes that work: accounts that aren't yours (identity theft or bureau mix-up), late payments where you have payment evidence, discharged debts still showing a balance, duplicate accounts, debts past the 7-year reporting limit.

Common disputes that don't work: you genuinely did miss the payment and you're hoping they can't verify it, you want to dispute a debt just because you don't like it, the item is accurate but unflattering. Bureaus aren't obligated to remove accurate negative information.

10Hard Pulls vs Soft Pulls: The Complete Picture

Hard inquiries and soft inquiries. This is one of the most misunderstood parts of the credit system, and the fear around hard pulls is way overblown.

Hard inquiry: happens when you apply for credit — a card, loan, mortgage, auto financing, apartment lease sometimes. The creditor is requesting to pull your full report to make an underwriting decision. This requires your authorization. It shows up on your credit report for two years. It affects your FICO score for approximately 12 months. The impact per inquiry: typically 2–5 points, occasionally up to 10 for someone with a very thin file or multiple recent inquiries.

Soft inquiry: happens when you check your own score, when a company pre-screens you for an offer, when your existing creditor does a periodic account review, when an employer does a background check. Never affects your credit score. Never. Not a little bit. Zero. You can check your score every single day and it won't move a single point from inquiries. (It might move from balance updates, but that's not the inquiry.)

The rate-shopping exception is real and people should use it. If you're shopping for a mortgage and getting quotes from four lenders over three weeks, FICO 8 bundles those into one inquiry for scoring purposes because they all occur within 45 days and they're all for the same loan type. Same for auto loans and student loans. So shop aggressively — get multiple quotes, don't let the fear of hard pulls stop you from comparing rates on a $400,000 mortgage. The cost of rate shopping inquiries is maybe 5 points. The cost of taking a rate 0.3% higher because you didn't shop is thousands of dollars.

For credit cards, there's no rate-shopping exception — each application is a separate inquiry. But an individual card inquiry is still just 2–5 points and fades within a year, so don't avoid applying for something useful just because of inquiry fear.

When does it matter? If you're about to apply for a mortgage in 30–60 days, don't open new cards or take new loans. Not because of the inquiry points, but because mortgage underwriters look at your full credit behavior recently and new accounts send a signal they don't love. If you're not planning a major application for 6+ months, a new inquiry is genuinely not worth worrying about.

11Rebuilding After Bankruptcy or Collections

This is the section I wish more sites wrote honestly, because the advice here is either 'just wait it out' (useless) or 'this one weird trick' (scammy). The reality is somewhere in between: rebuilding after serious credit damage takes time, but there's a lot you can do to accelerate it and a lot of traps to avoid.

After Chapter 7 Bankruptcy

Chapter 7 stays on your credit report for 10 years. Chapter 13 stays for 7 years. You will see your score in the 500s or lower initially. But — and this is important — many people see their scores start recovering within 12–18 months of discharge, not 10 years.

Why? Because as of discharge, your discharged debts show $0 balance. Your debt-to-income ratio might actually look better than it did before. You can't file again for 8 years (Chapter 7). Some lenders see post-bankruptcy borrowers as lower risk than pre-bankruptcy borrowers who are drowning in debt — you've had the reset.

The rebuild plan after bankruptcy: Month 1–3: Get a secured credit card immediately after discharge. Capital One Secured, Discover it Secured, and OpenSky (no credit check, no bank account required) are the most accessible options. Use it for one small recurring charge (Netflix, gas) and pay in full each month.

Month 3–6: Add a credit builder loan from Self or a credit union. Now you have both revolving and installment history building simultaneously.

Month 12: If you've been clean, many issuers will approve you for a basic unsecured card. Capital One has historically been bankruptcy-friendly after 12 months clean. Your secured card may graduate automatically.

Year 2–3: You're now looking at scores in the mid-600s to low 700s if you've been disciplined. Some people with otherwise clean new files hit 700+ by year 3 post-bankruptcy. Yes, the bankruptcy notation is still there. But lenders looking at your recent file see 3 years of clean credit.

Year 4+: FHA mortgages become available 2 years after Chapter 7 discharge. Conventional mortgages — 4 years. VA loans — 2 years. So bankruptcy doesn't mean homeownership is 10 years away. It's more like 2–4 years if you rebuild actively.

After Collections

Collections are more nuanced. An unpaid collection from 2020 is hurting you. Your options:

Pay for delete: Negotiate with the collection agency. Get the agreement in writing before you pay. Many will do it, especially smaller agencies or on older debts.

Settlement: If you can't pay in full, settle for less. This doesn't remove the item but it changes the status to 'settled' and shows a $0 balance. Under FICO 9 and VantageScore 4.0, a paid or settled collection has virtually no scoring impact. Under FICO 8 (still most common), paid collections still hurt, but less than unpaid ones.

Wait it out: Collections fall off after 7 years from the original delinquency date (not from when it was sent to collections — from when you first missed the payment with the original creditor). If a collection is 5 years old, it'll be gone in 2 years and its impact is already faded.

Do NOT: randomly 'reactivate' old debts by making partial payments. In some states, making any payment restarts the statute of limitations for legal collection. Always talk to a credit counselor or attorney before paying on a very old debt.

Medical collections specifically: Under rules finalized by the CFPB, medical debt under $500 is no longer included in credit reports as of 2025. Medical debt between $500 and $500+ may still appear but gets weighted less heavily in newer scoring models. If you have medical collections, verify whether they should even be on your report under the new rules.

Both prevent new creditors from accessing your credit report, which means someone can't open a new account in your name even if they have your Social Security number.

12Credit Freeze vs Credit Lock — And When to Use Each

Both prevent new creditors from accessing your credit report, which means someone can't open a new account in your name even if they have your Social Security number. They do basically the same thing but through different mechanisms.

Credit freeze: legal right under federal law (the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018). Free to place, free to lift at all three bureaus. When active, lenders who try to pull your credit get back nothing — the report is inaccessible. To apply for new credit yourself, you temporarily lift the freeze, apply, then refreeze. Lifting takes minutes online. Freezes work even if the bureau's systems have issues or the company changes its policies — it's a legal obligation.

Credit lock: proprietary product from each bureau — Experian Lock, TransUnion's TrueIdentity/InstantLock, Equifax Lock & Alert. Functionally similar but it's a toggle in an app rather than a legal mechanism. Usually faster to toggle on/off than a freeze. Often comes with monitoring features attached. Some are free, some are premium services.

Which to use: If identity theft is a real concern, use the freeze. It has legal protections. The lock is more convenient for people who apply for credit frequently but want protection when they're not actively in an application period.

When should everyone have a freeze on? If you're not planning to apply for credit in the near future, honestly, there's a solid argument for keeping a freeze on permanently. Data breaches are constant. Your SSN is probably already in a breach database somewhere. A freeze means that data can't be weaponized. Lifting it for 24 hours when you need to apply is a minor inconvenience versus the real cost of dealing with fraudulent accounts on your credit.

Placing a freeze: Go to each bureau separately. - Equifax: equifax.com/personal/credit-report-services/credit-freeze - Experian: experian.com/freeze/center - TransUnion: transunion.com/credit-freeze

You'll create a PIN or account. Keep it. You'll need it to lift the freeze. Don't lose the PIN — recovering it takes longer than you want when you're in a loan officer's office trying to close on a house.

13Credit Monitoring Services: Compared Honestly

There are free services, cheap services, and expensive services. The free ones are genuinely good now. The expensive ones are selling you mostly peace of mind plus some identity theft insurance.

Free options worth using:

Credit Karma — free, no-catch, shows TransUnion and Equifax VantageScore 3.0. Alerts you to new accounts, inquiries, changes to your report. Good enough for most people.

Experian free account — FICO Score 8 on Experian data, free credit report, Experian Boost (lets you add rent, utilities, streaming to your Experian file for a potential score bump). The boost feature is worth trying — free, adds positive history, and the worst case is it doesn't help. Experian CreditLock is also included in the paid upgrade but the basic account is free.

Capital One CreditWise — available to everyone, not just Capital One customers. Good for monitoring TransUnion.

AnnualCreditReport.com — not monitoring per se, but weekly free reports from all three bureaus. If you're disciplined enough to check monthly, this is free and complete.

Paid services:

IdentityForce ($19.99–$34.99/month) — three-bureau monitoring, identity theft insurance up to $1M, social media monitoring, dark web scanning. Good if you're worried about identity theft specifically.

Aura ($12–$15/month for individuals) — well-rated, aggressive identity theft insurance, credit monitoring across all three bureaus, VPN and antivirus included. Good value if you want the full security package.

LifeLock (Norton) ($11.99–$34.99/month) — widely known brand, three-bureau monitoring, up to $1M identity theft insurance on higher tiers. Mixed customer service reviews but solid product.

Experian IdentityWorks ($24.99/month) — direct from the bureau, three-bureau monitoring, FICO scores from all three bureaus (not just one), dark web monitoring, $1M identity theft insurance. If you want official Experian monitoring rather than a third party, this is it.

My honest take: for most people, Credit Karma plus Discover Scorecard (for your actual FICO 8) plus a credit freeze covers 90% of what you'd pay $15–$35/month for. The main thing you're paying for with premium services is the identity theft insurance, which has enough exclusions in most policies that it's less valuable than it sounds. If you're high-profile, have been a victim of identity theft before, or just want zero hassle, paying for Aura or IdentityForce is reasonable. Otherwise, use the free stack.

14The Big Credit Score Myths — Killed One by One

Some of these myths are so embedded that even well-meaning financial advisors repeat them. Let's go through the biggest ones.

Myth: Checking your own credit score hurts it. Dead wrong. Checking your own score is a soft inquiry. Soft inquiries have zero impact on your score. Zero. You can check it every single day. The myth probably comes from confusion with hard inquiries (from lenders), which do have a small impact. But you checking your own score? Completely harmless. Check it constantly — the more you understand it, the better you'll manage it.

Myth: Carrying a balance helps your credit score. Nope. I hate this one because it costs people real money. The idea is that carrying a small balance 'shows the bank you're using the card.' What it actually does is cost you interest at 20–28% APR for no scoring benefit. Paying in full every month is the optimal move — you show credit utilization (because your statement balance is reported before you pay), you demonstrate the account is active, and you pay $0 in interest. The myth might have originated from a misunderstanding of how statement balances work, or it might have been spread by card issuers who benefit from people carrying balances. Either way, it's wrong.

Myth: Closing old cards you don't use is smart. Usually backwards. Closing an old card with no annual fee almost always hurts your score — it reduces your total available credit (increases utilization) and removes account age over time. The only times to close a card are: it has an annual fee you can't justify, you're prone to overspending with it, or you're getting married and simplifying joint finances. Otherwise, lock it in a drawer and forget it exists.

Myth: You only have one credit score. As covered earlier — you have dozens. Each bureau, each model version, each industry-specific score. Don't obsess over one number.

Myth: Once you reach 800 you don't need to worry. Your score can go down just as fast from 820 as from 720 if you miss a payment or spike your utilization. Maintaining an excellent score requires ongoing behavior, not a onetime achievement.

Myth: A debt settlement is almost as good as paying in full. It's not. 'Settled' stays on your credit report for 7 years and signals to lenders that you paid less than you owed. Paying in full — or getting pay-for-delete — is materially better for your score and for your creditworthiness in manual underwriting reviews (like mortgages, where a human looks at your file).

Myth: Opening lots of store credit cards is great for your credit. The inquiry hit is small, sure. But store cards typically have low limits ($300–$1,000), which means even a modest balance is high utilization on that card. And the average account age impact of opening several new accounts is real. Retail cards are fine for specific strategic purposes but opening them indiscriminately is not a credit-building strategy.

Myth: Income affects your credit score. It doesn't. Your income isn't on your credit report. A millionaire with a spotty payment history has a worse score than a teacher with a perfect 20-year track record. Income shows up on loan applications for debt-to-income calculations, but it has zero direct impact on your credit score. This is also why sometimes people with high incomes are surprised when their score is mediocre — they assumed the money would carry them.

Myth: Your score resets after 7 years. Not quite. Negative items fall off after 7 years (10 for Chapter 7 bankruptcy). Positive accounts can stay on your report indefinitely — that's actually a feature. A 20-year-old account with perfect payment history is still helping you at year 20. The 7-year thing only applies to the negative items dropping off, not to your whole credit history wiping clean.

15How Credit Scores Affect Mortgage, Auto, and Card Rates — Real Numbers

This section is numbers, but they're important numbers. Not hypothetical ranges — these are based on actual rate tiers that lenders publish or commonly apply, calibrated to 2026 market rates.

Mortgages

Mortgage lenders use FICO Score 2 (Experian), FICO Score 5 (Equifax), and FICO Score 4 (TransUnion) — all older FICO versions specifically for mortgage lending. They pull all three and use the middle score. This is different from FICO 8, which means your mortgage score can differ from your 'regular' FICO 8 by 10–30 points.

Conventional loan rate tiers (30-year fixed, $400k loan, 2026 rates approximate): - 760–850: Best available rate, around 6.5–6.7% - 740–759: +0.1% to best rate - 720–739: +0.2–0.3% - 700–719: +0.3–0.5% - 680–699: +0.5–0.75% - 660–679: +0.75–1.0% - 640–659: +1.0–1.5% - 620–639: +1.5–2.0%, or lender overlays may require FHA - Below 620: Conventional rarely available; FHA with 3.5% down minimum

On a $400,000 loan, the difference between a 760 score (6.6%) and a 680 score (7.2%) is: - 760: $2,555/month → $919,980 total cost over 30 years - 680: $2,717/month → $978,120 total cost over 30 years - Difference: $162/month, $58,140 total

Auto Loans

Auto lenders typically use FICO Auto Score 8 or 9, which weight your auto loan payment history more heavily than standard FICO 8. Your auto score can be higher or lower than your standard score depending on your history with vehicle loans.

New car, 60-month loan, $35,000, 2026 average rates by tier: - Super Prime (720+): 6.5–7.5% - Prime (660–719): 8.5–11% - Non-Prime (620–659): 12–15% - Subprime (580–619): 17–22% - Deep Subprime (below 580): 23–28% (or denial)

Monthly payments on $35,000 at 60 months: - 7% (720+): $693/month → $41,580 total - 10% (660–719): $743/month → $44,580 total (+$3,000) - 14% (620–659): $814/month → $48,840 total (+$7,260) - 20% (subprime): $928/month → $55,680 total (+$14,100)

That $14,100 difference between a 720 score and a 580 score on a mid-priced car purchase is real money. If you're in the 580s and need a car, seriously consider a credit builder loan for 12 months to get to 620+ before financing.

Credit Cards

Credit cards are harder to give exact numbers for because issuers use a wider range of factors and the ranges within their cards can be enormous. The same card might offer anywhere from 19.99% to 29.99% APR depending on your creditworthiness.

Typical approval thresholds by card category: - Premium travel cards (Chase Sapphire Reserve, Amex Platinum): 720+ practical minimum, 700+ possible - Cashback rewards (Chase Freedom, Discover it): 670+ - Basic cards (Capital One Quicksilver standard): 640+ - Secured cards: Available regardless of score (no minimum)

On a $5,000 revolving balance: - 19.99% APR: $83/month in interest - 24.99% APR: $104/month in interest - 29.99% APR: $125/month in interest

Don't carry balances on credit cards. But if you do, having good credit at least means you're paying less for it.