1Why Your Checking Account Is Probably Costing You More Than You Think

Most people open a checking account in their twenties, never look at it again, and just... accept whatever the bank does to them. Monthly fees. ATM charges. Overdraft penalties. It adds up. One study found the average American pays over $300 a year in banking fees — fees that are entirely avoidable if you pick the right account.

And here's the thing nobody tells you: the best checking accounts in 2026 are dramatically better than they were even five years ago. Online banks and neobanks have essentially forced traditional banks to compete on features, which means you can now get a checking account with no monthly fee, 2-day early direct deposit, 50,000+ free ATMs, and decent interest — all for $0 a month.

So if you're still paying $12 to $15 a month for a basic checking account at a legacy bank, this guide is for you. We're going deep on every major option, ranked honestly, with real numbers.

2How Checking Accounts Actually Work

A checking account is just a transactional deposit account — it's designed for money moving in and out constantly. Paycheck hits Friday. Rent leaves Monday. Groceries, gas, subscriptions — all of it flows through your checking account. Unlike savings accounts, there are no federal limits on how many withdrawals you can make per month (that old Reg D rule limiting savings withdrawals to 6/month was suspended in 2020 and many banks have dropped the limit entirely).

When you deposit money, it sits at the bank. The bank lends most of it out — that's how they make money — and in exchange, you get FDIC insurance up to $250,000 per depositor per institution. Your money is safe even if the bank fails.

The mechanics day-to-day: you swipe your debit card, it hits your account within seconds via the Visa or Mastercard network. You write a check, it takes 1-3 business days to clear. You set up ACH direct deposit, your employer sends it through the Automated Clearing House network — usually lands 1-2 days before payday if your bank supports early direct deposit.

The routing number (9 digits) identifies your bank. Your account number identifies you. You'll need both for direct deposit, wire transfers, and setting up autopay anywhere.

One thing worth knowing: checking accounts used to pay essentially 0% interest. That's changed. Online banks now commonly offer 0.50% to 3.30% APY on checking balances — some even higher — which means your checking account can actually work a little harder for you while still being fully liquid.

3Types of Checking Accounts (Not All Are Created Equal)

Before we rank the best options, you need to know what you're shopping for. There are six main types:

**Free Checking Accounts**

No monthly fee, no minimum balance, no hoops to jump through. This is the baseline you should demand in 2026. Online banks basically made this standard. Capital One 360, Ally, Chime — they all do this. Traditional banks like Chase and BofA still charge monthly fees, but they're waiveable with basic conditions (more on that below).

**Online / High-Yield Checking Accounts**

These are checking accounts that pay real interest — sometimes competitive with high-yield savings accounts. Axos Rewards Checking goes up to 3.30% APY. Primis Bank's Premium checking hits 3.70% APY. SoFi's checking pays 0.50% APY flat, which isn't wild, but it's real money compared to the 0.01% you're getting at Chase. The catch is usually behavioral requirements: minimum debit card swipes, minimum monthly deposits, etc.

**Interest-Bearing vs Standard Checking**

A standard checking account pays nothing or nearly nothing. An interest-bearing checking account pays some APY. Almost every online bank now offers interest — the difference is how much and whether you have to jump through hoops to earn it.

**Business Checking Accounts**

Different category entirely. Business checking has higher transaction volumes, different fee structures, and often includes tools like invoicing integrations, multi-user access, and accounting software connections. Chase Business Complete, Mercury, and Relay are the main names worth knowing for small businesses and startups.

**Student Checking Accounts**

Mostly just regular checking accounts with the monthly fee waived if you're under 24 or enrolled in college. Chase College Checking, Bank of America Advantage SafeBalance for students — these exist mainly because banks want to capture customers young. They're fine. Not special.

**Second-Chance Checking Accounts**

For people who got flagged in ChexSystems — the banking industry's version of a credit report — for overdrafts, bounced checks, or accounts closed in bad standing. Most banks check ChexSystems before approving you for a checking account. Second-chance accounts skip that check, typically come with more restrictions and sometimes a small monthly fee, and give you a path back to normal banking. Capital One, Chime, and GO2bank all offer these. Worth knowing if you've had banking problems in the last five years.

No affiliate-padding fluff, no ranking the account that pays us the most first.

4Best Checking Accounts 2026 — Ranked

Here's the honest breakdown. No affiliate-padding fluff, no ranking the account that pays us the most first.

---

**1. Charles Schwab Bank High Yield Investor Checking — Best for Travelers**

This is the one I'd tell a friend who travels internationally: get the Schwab checking account. Full stop.

Unlimited ATM fee reimbursements. Worldwide. Any ATM, anywhere on earth. They reimburse 100% of whatever the ATM charges you, showing up as a lump credit at month-end. No foreign transaction fees. No monthly fee. No minimum balance.

The catch: you have to also open a Schwab brokerage account. It takes five minutes and has no minimum balance requirement — you don't have to actually invest anything. It's just a linked account.

APY on the checking balance is modest (around 0.45%), but honestly nobody picks Schwab for the yield. They pick it because they've been to Europe and gotten dinged $5 at every ATM, and they're not doing that anymore.

Best for: frequent travelers, anyone who uses ATMs constantly.

---

**2. Ally Bank Spending Account — Best Online Bank for Most People**

Ally is what a checking account should look like in 2026. No monthly fee. No minimum balance. 75,000+ fee-free ATMs through Allpoint and MoneyPass. Up to $10 per month in reimbursements for out-of-network ATM fees (not unlimited like Schwab, but covers most people's needs).

The thing that makes Ally different: their overdraft protection is genuinely good. They don't charge overdraft fees — period. Instead they offer CoverDraft, which covers up to $100 (or $250 if you have qualifying direct deposits) at no charge. You just have to pay it back within 14 days. For people who occasionally get a little short before payday, this is a huge deal.

Interest: modest, but positive. Their checking earns a small amount. Their Ally Savings account earns significantly more, and it's easy to link the two.

App is clean. Customer service is available 24/7. And they've been around long enough that there's real trust in the brand. Not a fly-by-night neobank.

Best for: general everyday checking, people who want a no-drama online bank.

---

**3. SoFi Checking and Savings — Best for Direct Deposit Users**

SoFi won NerdWallet's Best Overall Bank award for 2026, and it's not hard to see why. The checking account pays 0.50% APY flat — no requirements, no hoops, just 0.50% on every dollar. Their linked savings account pays up to 3.30% APY with eligible direct deposit.

The real draw: early direct deposit. If you set up direct deposit with SoFi, your paycheck can hit up to two days early. For someone living paycheck to paycheck (or just someone who doesn't like waiting), that's legitimately valuable.

No monthly fees. No overdraft fees. 55,000+ fee-free Allpoint ATMs nationwide. And they offer a $300 welcome bonus right now for new accounts with qualifying direct deposits — one of the better bank bonuses available without a lot of complexity.

The SoFi app is also genuinely good — you can see your checking and savings in one place, set up vaults for different savings goals, and manage everything from your phone. They've built a financial ecosystem (loans, investing, insurance) so if you're someone who wants everything in one place, SoFi makes a compelling argument.

Best for: people who direct deposit, want early payday, and don't want to think too hard about it.

---

**4. Chase Total Checking — Best Traditional Bank**

Chase is the largest bank in the US and their Total Checking account is the default recommendation for anyone who needs branches, in-person service, or wants a big-name bank.

The $15 monthly fee is easy to waive: get at least $500 in monthly electronic deposits, or maintain a $1,500 minimum daily balance, or keep $5,000 across linked Chase accounts. Most people with direct deposit will hit that $500 threshold without trying.

Right now they're offering a $400 bonus for new accounts — open a Total Checking, make $1,000 in qualifying direct deposits within 90 days, and Chase drops $400 in your account. That offer expires April 15, 2026, but Chase runs promos like this constantly. If you're switching anyway, timing it with a bonus offer is easy money.

The Chase network is massive: 4,700+ branches, 15,000+ ATMs. If you've ever had a banking issue that couldn't be resolved over the phone and needed to sit across from a human, Chase is probably within a few miles of wherever you are.

Chase doesn't pay meaningful interest on checking balances. That's the tradeoff for the physical footprint. But if you need a traditional bank and you want the one that's least likely to cause you problems, Chase is it.

Best for: people who want branches, want a signup bonus, families.

---

**5. Capital One 360 Checking — Best Fee-Free Traditional-ish Bank**

Capital One sits in an interesting middle ground — they have real branches and Capital One Cafes in major cities, but they operate mostly like an online bank. No monthly fees. No minimum balance. No overdraft fees (they auto-decline transactions that would overdraft, or you can link a savings account for free transfers).

Their 360 Checking earns interest — not a lot, but something, unlike most traditional banks. And they offer robust overdraft options: Auto-Decline (safer, no fee), Free Savings Transfer (pulls from linked savings), and no-fee overdraft coverage.

Note: as of early 2026, Discover Bank completed its merger with Capital One, and Discover stopped accepting new banking applications in January 2026. Existing Discover accounts are migrating to Capital One. If you had a Discover Cashback Debit account (which paid 1% cash back on debit purchases — genuinely great), that's going away as the migration completes. Capital One doesn't currently have an equivalent cash back debit product.

Best for: people who want no fees, some branches, solid mobile banking.

---

**6. Bank of America Advantage Banking — Best If You're Already in the BofA Ecosystem**

Honest take: BofA checking isn't the most exciting account. The $12 monthly maintenance fee is waiveable if you receive at least $250/month in direct deposits or maintain a $1,500 minimum daily balance — which most people can hit. But you're jumping through hoops that Ally or Capital One don't make you jump through.

Where BofA shines is integration. If you have BofA credit cards, investments through Merrill, or a BofA business account, the Preferred Rewards program unlocks real benefits — bonus credit card points, discounts on loans, interest rate boosts on savings. The more BofA products you have, the more the whole ecosystem pays off.

One thing to watch: BofA is overhauling their Preferred Rewards program in May 2026. It's becoming BofA Rewards with new tier requirements tied to 3-month average daily balances. The minimum to waive monthly fees will require higher balance tiers than before for some account types. If you're a BofA customer, review the changes before May 26, 2026.

Current new account bonus: up to $300 with $5,000 in qualifying direct deposits within 90 days, or up to $500 with $10,000.

Best for: existing BofA customers, people deep in the BofA ecosystem.

---

**7. Axos Rewards Checking — Best High-Yield Checking for Power Users**

Axos is an online bank that nobody talks about enough. Their Rewards Checking account earns up to 3.30% APY — on a checking account. That's real money on a balance of $10,000 or $20,000.

The catch is the requirements. To hit the full 3.30%, you need: $1,500 or more in monthly direct deposits (0.40% base), plus 10 qualifying debit card purchases per month (adds more APY), plus an Axos Managed Portfolios investing account with $2,500 average daily balance. If that sounds like a lot of conditions... it is. The account rewards you for using Axos as your financial hub, not just a checking account.

If you're not going to meet all the requirements, you'd earn a lower APY — still better than most, but not the headline number.

Axos also does unlimited ATM fee reimbursements on Rewards Checking, which is a serious perk. No monthly fees. No overdraft fees. They're legitimately good and underrated.

Best for: people who want to maximize checking APY and will actually meet the requirements.

---

**8. Schwab vs Ally for ATM Access — Side-by-Side**

This comparison comes up constantly because both are online banks with strong ATM policies:

Schwab: Unlimited ATM reimbursements worldwide, no cap, no questions asked. You need a linked Schwab brokerage account (no minimum). The Schwab debit card is the gold standard for international travel.

Ally: $10/month reimbursement cap for out-of-network ATMs, plus 75,000+ fee-free ATMs in-network. For most domestic users, the $10 cap is more than enough. The difference only matters if you're hitting 4+ out-of-network ATMs a month or traveling internationally.

5The Real Talk on Checking Account Fees (And How to Kill Every One of Them)

Banks made $8.8 billion in overdraft fees in 2023 alone. That number is coming down — partly because regulators are paying attention, partly because online banks don't charge them — but it's still a massive wealth transfer from regular people to financial institutions.

Here are the four main fee categories you need to know:

**Monthly Maintenance Fees**

Range: $0 to $25/month depending on account type.

Chase Total Checking: $15/month, waived with $500+ monthly electronic deposits or $1,500 minimum daily balance. Bank of America Advantage Plus: $12/month, waived with $250+ monthly direct deposit or $1,500 minimum daily balance. Wells Fargo Everyday Checking: $10/month, waived with $500+ monthly deposits. Citibank Access Account: $10/month, waived with one qualifying activity per statement period.

Online banks (Ally, SoFi, Capital One 360, Axos, Schwab): $0. No hoops.

How to kill it: Switch to an online bank, or set up direct deposit at your current bank. Almost every major bank waives the fee with direct deposit.

**Overdraft Fees**

This is the big one. Traditional banks historically charged $25 to $37 per overdraft transaction. That's per transaction — you buy a $4 coffee while overdrawn, you get hit with a $35 fee.

Good news: major banks have dramatically reduced overdraft fees under regulatory pressure. Chase dropped their overdraft fee to $34 but won't charge it if you're overdrawn by $50 or less at day's end, or if you bring it back within 50 bucks by the next business day. BofA cut their overdraft fee to $10 (down from $35) and capped it at two per day.

Online banks mostly don't charge overdraft fees at all. Ally has CoverDraft (covers up to $250, no fee). SoFi declines or covers depending on your setup. Axos charges $0 in overdraft fees.

How to kill it: Switch to an online bank, or at minimum link a savings account to your checking for free overdraft transfers. Never keep a near-zero balance.

**ATM Fees**

Out-of-network ATM fee from your bank: typically $2.50 to $3.50 per withdrawal. Fee from the ATM operator themselves: usually $3 to $5 on top.

So if you use a random ATM at a gas station, you might pay $8 for the privilege of accessing your own money. Every time.

How to kill it: Schwab (unlimited worldwide reimbursements), Axos Rewards (unlimited reimbursements), Ally (up to $10/month). Or use in-network ATMs — Chase has 15,000, Ally has 75,000 Allpoint/MoneyPass machines, SoFi has 55,000 Allpoint ATMs. There is zero reason to pay ATM fees in 2026.

**Wire Transfer Fees**

Incoming domestic wire: usually $0 to $15 at traditional banks. Outgoing domestic wire: $25 to $35 at most traditional banks. International wire: $25 to $50.

Chase charges $35 for outgoing domestic wires unless you're a premium account holder. Ally charges $20 for outgoing domestic wires. Axos charges $0 for domestic wires on some accounts. Mercury (business) charges $0 on domestic wires.

How to kill it: For most regular people, Zelle covers 99% of person-to-person transfers for free. For large business transfers, Mercury or Relay make more sense than Chase. If you're doing international, consider Wise (formerly TransferWise) instead of a bank wire — the exchange rates are dramatically better.

6Features That Actually Matter in 2026

Not all checking accounts are equal on the features side. Here's what's worth comparing:

**Early Direct Deposit**

This is bigger than it sounds. Most traditional banks hold your direct deposit until the official payday. Online banks — SoFi, Chime, Axos, Ally, Current — can see the deposit coming 1-2 days early and release it immediately.

SoFi: up to 2 days early. Chime: up to 2 days early. Axos: up to 2 days early. Ally: up to 1 day early on some transfers.

If you're a W2 employee who gets paid biweekly, that's potentially 26 extra days of access to your money per year. Not trivial.

**ATM Networks — the Numbers**

Chase: 15,000 ATMs (proprietary) Ally: 75,000 ATMs (Allpoint + MoneyPass) SoFi: 55,000 ATMs (Allpoint) Capital One: 70,000 ATMs (Capital One + AllPoint) Axos: reimbursements instead of proprietary network Schwab: unlimited reimbursements worldwide

**Mobile Check Deposit**

Every major bank does this now. The differences are in limits and hold times. Chase allows up to $10,000 per day via mobile deposit for established customers. Some online banks are more conservative at first and raise limits over time. If you regularly receive large checks (settlements, business payments), ask about limits before switching.

**Zelle Integration**

Zelle is now built into the apps of basically every major bank: Chase, BofA, Wells Fargo, Citi, Capital One, US Bank, Ally, and more. It's free, instant (usually), and works peer-to-peer between banks. This has replaced personal checks and cash for most people under 50.

Caveat: Zelle has a fraud problem. If you send money to a scammer, Zelle is not required to refund you the way a credit card company would. Never send Zelle payments to anyone you don't know personally.

**Account Number Portability**

Not a thing in the US yet (unlike the UK). When you switch banks, you get a new account number and routing number. Which means you have to update every autopay and direct deposit. Pain in the ass — but manageable with a checklist (we have one below).

**FDIC Insurance**

All the accounts in this guide are FDIC-insured up to $250,000 per depositor per institution. For most people that's more than enough. If you're parking more than $250K in a single bank, look at CDARS or multi-bank laddering strategies — though that's a different problem than most people reading this have.

7Checking vs Savings: What Goes Where

The short version: checking is for money you're spending. Savings is for money you're not touching.

Checking accounts are built for transactions — unlimited debit card swipes, Zelle transfers, autopay, ATM withdrawals. Savings accounts typically earn significantly higher APY (right now the national average is around 4-5% for high-yield savings) but are meant to sit and accumulate.

The classic strategy: keep 1-2 months of expenses in checking for daily operations. Keep your emergency fund and any near-term savings goal in a high-yield savings account linked to your checking. Move money between them as needed — it usually clears same-day or next day.

SoFi makes this seamless: one app, checking earns 0.50% APY, savings earns up to 3.30% APY, and Vaults let you sub-divide your savings by goal. Ally does the same thing — spending account linked to savings, automated savings rules, round-up features.

Dont put everything in checking. If you have $20,000 sitting in a Chase checking account earning 0.01% APY, you're leaving ~$800+ a year on the table versus a high-yield savings account at 4%+. The checking/savings split is one of the highest-ROI optimizations most people can make with basically no effort.

If you use cash regularly — and plenty of people do, especially at farmers markets, small businesses, restaurants that still go cash-only — ATM fees are a real ongoing expense.

8Best Banks for ATM Reimbursements (Deep Dive)

If you use cash regularly — and plenty of people do, especially at farmers markets, small businesses, restaurants that still go cash-only — ATM fees are a real ongoing expense. Here's the pecking order:

**Tier 1: Unlimited Worldwide**

Charles Schwab Bank High Yield Investor Checking: unlimited ATM fee reimbursements globally. The single best debit card for travelers on earth. When you withdraw euros at a Paris ATM and the machine charges you €4, Schwab credits you back. Every time. No monthly cap.

Axos Rewards Checking: unlimited ATM fee reimbursements in the US. Not quite global like Schwab, but domestic travelers get the same unlimited protection.

**Tier 2: Capped Reimbursement + Large Free Network**

Ally Bank: up to $10/month reimbursement for out-of-network ATMs + 75,000 free Allpoint/MoneyPass ATMs. For most people the $10 cap is irrelevant because they're hitting the free network first.

Capital One 360: 70,000 free ATMs through Capital One + Allpoint network. No out-of-network reimbursement, but the network is large enough that you rarely need it.

**Tier 3: Large Proprietary Network, No Reimbursement**

Chase: 15,000 proprietary ATMs, no reimbursement for others. Fine if you live near Chase ATMs. Annoying if you travel to places Chase isn't.

Bank of America: similar story — big in urban cores, gaps elsewhere.

**The Math on Schwab**

If you're using ATMs 3x a week and paying $5 average in fees: that's $780/year. Schwab gives you every dollar back. The account itself costs nothing. There's no reason not to have a Schwab checking account as your travel card even if it's not your primary account.

9Business Checking Accounts — The Comparison

Personal checking and business checking are different products for different problems. Business checking needs to handle higher transaction volumes, multiple users, integrations with accounting software like QuickBooks or Xero, and sometimes physical cash deposits.

Here are the main options worth considering for small businesses and startups:

**Chase Business Complete Checking**

Fee: $15/month, waiveable with $2,000 minimum daily balance. Transactions: 20 free teller transactions/month, unlimited debit card and ATM transactions. Best for: businesses that need physical branches, in-person cash deposits, or an existing Chase relationship. Bonus: Chase regularly runs business checking bonuses — check their current offers.

**Mercury**

Fee: $0. No monthly fees, ever. Best for: startups, tech companies, online businesses with no need for physical banking. Features: no-fee domestic and international wires, treasury accounts earning mid-4% APY, virtual cards, API access, team debit cards. Built for founders. Catch: no cash deposits. If your business handles physical cash, Mercury isn't it. Venture-backed darling in the startup world — if you're building something and your investors are in Silicon Valley, they'll nod approvingly at Mercury.

**Relay**

Fee: $0 base (Relay Pro is $30/month for advanced AP features). Best for: businesses that want organized multi-account setups — you can open up to 20 checking accounts and 2 savings accounts under one business profile. Features: team debit cards, spending limits, roles and permissions, free ACH/wires on base tier. Relay Pro adds: same-day ACH, outgoing wires, accounts payable features. Ideal for: small business owners and bookkeepers who want everything organized by purpose (payroll account, tax account, operating account, etc.).

**Axos Basic Business Checking**

Fee: $0 with qualifying conditions. Bonus: $200 promotion running through mid-2026 for new accounts. Best for: businesses that want a simple, no-fee online business account.

**The Short Answer on Business Checking**

If you need branches: Chase. If you're a startup or fully digital business: Mercury. If you want organized multi-account management: Relay. If you want APY on your business cash: Mercury's treasury accounts or Relay's interest tiers beat Chase by miles.

10Bank Bonuses for New Checking Accounts — Free Money, Honestly

Bank bonuses are real, they're taxable (you'll get a 1099 at year-end), and they're worth chasing if you're switching anyway. Here are the current major offers as of March 2026:

**Chase Total Checking: $400** Requirement: Open a new Chase Total Checking account and receive at least $1,000 in qualifying direct deposits within 90 days of coupon enrollment. Expires: April 15, 2026. Notes: Not available to existing Chase checking customers or accounts closed in the last 90 days or closed with negative balance in the last 3 years. Chase frequently relaunches these promos, so if you miss this one, check back in a month.

**Citibank: Up to $325 (or more in tiers)** Requirement: Receive at least two enhanced direct deposits totaling $3,000 or more within 90 days of opening. Tiered structure: $325 at the base level, $750 with $30,000 in deposits, $1,500 with $200,000. For most people: $325 with a paycheck redirect is very achievable.

**Bank of America: Up to $500** Tiered by deposit amount: $100 with $2,000 direct deposits within 90 days, $300 with $5,000, $500 with $10,000. For most W2 workers: $300 with two paychecks is realistic.

**SoFi: Up to $300** Requirement: New member with eligible direct deposit, $300 with qualifying deposits. Notes: SoFi structures their bonus through a combination of cash + fee credits. Verify current terms on their site.

**Axos: $200 for business, various personal offers** Axos runs rotating promotions. Their basic business checking has a $200 offer running currently.

**The Strategy**

Bank bonuses are essentially free money for doing what you'd be doing anyway (direct deposit). The friction is the 2-3 month window and the redirect process. If you're planning to switch banks, do it during a bonus window. The $400 Chase bonus is one of the better publicly available bonuses right now.

Just be aware: if you close the account within 6 months, banks typically claw back the bonus.

11Digital Banks vs Traditional Banks — Honest Comparison

This debate has basically been settled in favor of digital banks for most use cases. But 'most' isn't 'all.' Here's the honest breakdown:

**Where Digital Banks Win**

Fees: Zero monthly fees, zero overdraft fees, zero ATM fees (with good accounts). Traditional banks still charge for all of these by default.

Early direct deposit: Online banks can see deposits coming 1-2 days early and release funds immediately. Traditional banks typically make you wait.

APY: Online banks pay actual interest on checking balances. Big traditional banks pay essentially nothing — Chase checking earns 0.01% APY.

Mobile experience: Ally, SoFi, Chime — these companies were built for mobile. Their apps are genuinely excellent. Chase and BofA have decent apps but they were retrofitted onto legacy infrastructure.

Account opening: open online in 5 minutes. Traditional banks sometimes require you to come in.

**Where Traditional Banks Win**

Branches: if something goes wrong — fraudulent charge, complicated wire, estate banking — walking into a branch and talking to a human is still valuable. Ally and SoFi are phone/chat only.

Cash deposits: digital-only banks don't do cash deposits at all or make it extremely inconvenient (ATM deposits at limited machines). If you handle cash regularly, you need a traditional bank.

Lending relationships: Chase, BofA, Wells Fargo have in-house mortgage, auto, and personal loan products that often work better when paired with a checking account. Your direct deposit history with a traditional bank can sometimes help your loan application.

Trust and familiarity: some people — especially older generations — simply feel more secure at a big bank with FDIC insurance prominently advertised, physical offices, and decades of history.

**The Smart Play**

Honestly? Have both. A Schwab or Ally account for everyday spending (no fees, better ATMs) and a Chase or BofA account if you need branch access occasionally. There's no rule that says one checking account. Many financially savvy people keep 2-3 accounts: one for daily spending, one for bills/autopay, one travel card.

Overdraft protection sounds like a service the bank is doing for you.

12Overdraft Protection — What Your Options Actually Are

Overdraft protection sounds like a service the bank is doing for you. It's not. It's been a primary profit center for traditional banks for decades — one they're finally being forced to roll back.

Here are the options, from worst to best:

**Standard Overdraft Coverage (aka 'Courtesy Pay')**

The bank covers your overdraft and charges you a fee — historically $35 per transaction. Citi and Chase have dropped fees, BofA reduced theirs to $10. But you're still paying for the bank's 'generosity' in covering a transaction that overdraws you by $7.

Avoid this if possible.

**Overdraft Transfer from Savings**

Free at most banks. When your checking goes negative, the bank automatically transfers money from your linked savings account. Capital One does this for free. Chase charges $12 for this service (per transfer), which is annoying. Wells Fargo charges $12.50. Ally and SoFi do it free.

This is fine. Set it up.

**CoverDraft / Buffer Programs**

Ally's version: CoverDraft covers up to $100 ($250 with qualifying deposits) at zero charge, paid back automatically when your next deposit hits. You're not paying a fee, you're just getting a short-term buffer.

Chime's SpotMe works similarly — up to $200 buffer on debit purchases with no fee, based on your Chime account history.

**Auto-Decline**

Capital One 360's default: if a transaction would overdraft you, it's declined. No fee, no coverage. Some people prefer this — better to have your card declined than pay overdraft fees.

**The Setup You Should Have**

If you're at a bank that charges overdraft fees: link a savings account for free overdraft transfers, and turn off courtesy pay (standard overdraft coverage) for debit card purchases. This is opt-out at most banks — you have to explicitly request it. Call or do it in the app settings.

If you switch to Ally or SoFi: problem mostly solved by default.

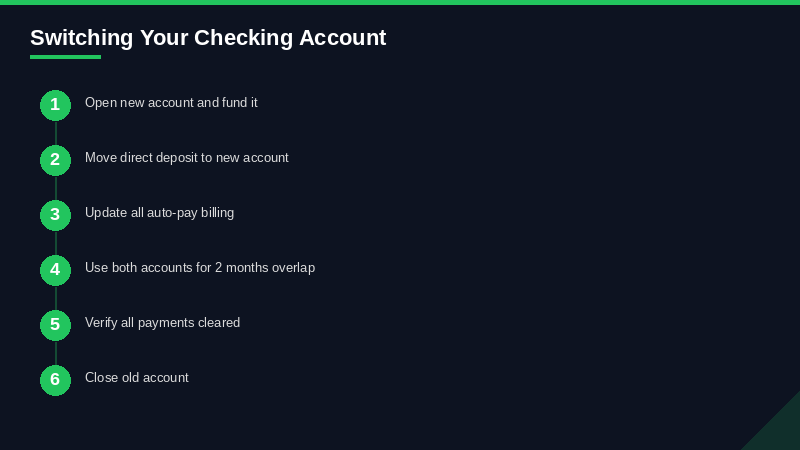

13How to Switch Banks — Step-by-Step Checklist

Switching banks is one of those things that seems harder than it is. Most people put it off for years because the friction feels high. It isn't, really — it takes about 30-45 minutes total spread over a month. Here's the exact playbook:

**Week 1: Open the New Account**

Open your new account first. Get the account number and routing number. Fund it with a small initial deposit (even $25 works at most online banks — many have $0 minimum).

**Week 1-2: Audit Your Old Account**

Pull 3-6 months of bank statements. List every recurring charge: subscriptions (Netflix, Spotify, gym, etc.), autopay bills (utilities, insurance, phone), and any automatic transfers. You're looking for annual charges too, not just monthly — quarterly insurance premiums, annual subscriptions.

Also list any incoming deposits other than your main paycheck: freelance payments, Venmo transfers, government benefits, side income.

**Week 2-3: Update Direct Deposit**

Contact HR or your payroll provider. Give them the new routing and account numbers. Most employers have an online HR portal for this. It typically takes 1-2 pay cycles to take effect, so do this early.

If you get Social Security or VA benefits, update separately at ssa.gov or va.gov.

**Week 2-3: Update Autopay and Subscriptions**

Work through your list. Update each biller's bank account info. Don't rush this — one missed update and you get a late fee or a service interruption.

Pro tip: update bills in order of consequence. Start with rent/mortgage, utilities, insurance. Streaming services can wait.

**Week 4-6: Monitor Both Accounts**

Keep both accounts open. Let at least 2 pay cycles hit the new account to confirm direct deposit is working. Watch the old account for any stragglers — a biller you missed, a quarterly charge you forgot about.

Do NOT close the old account until you're confident everything has migrated.

**Week 6-8: Close the Old Account**

Confirm zero outstanding checks, zero pending transactions. Zero balance (or transfer remaining funds). Call or visit to request account closure. Get written confirmation.

If there's a credit line or overdraft protection attached to the checking account, closing the account may affect your credit. Usually not a big deal for checking accounts, but worth knowing.

**Common Mistakes**

Closing the old account too fast — checks you forgot about will bounce. Forgetting annual subscriptions — they'll charge the old account and fail. Not confirming direct deposit actually switched — one paycheck going to a zero-balance closed account is a bad day.

14Student Checking Accounts — What to Actually Get

The student-specific checking account market exists mostly as a marketing move by big banks to capture customers early. That said, the student fee waivers are real and worth taking if you're in school.

**Chase College Checking**

No monthly service fee for up to 5 years while in school (requires proof of student status). After that, waiveable with $500/month electronic deposits. Standard Chase features — 15,000 ATMs, good mobile app, Zelle. A solid first account.

**Bank of America Advantage SafeBalance**

No overdraft fees by design (transactions are declined if insufficient funds). $4.95/month fee, waived for students under 25 or Preferred Rewards members. No paper checks (it's purely debit-based). Good for students who want guardrails against overdrafting.

**The Honest Recommendation for Students**

Get a Chase College Checking for the branch access and the $125 student bonus (they run this periodically). But also open an Ally or SoFi account. Use Chase for on-campus cash needs. Use Ally for your savings and online spending. You're building habits now that will pay off for decades — might as well start with no fees.

15Second-Chance Checking Accounts — Getting Back in the Game

ChexSystems is the banking world's equivalent of a credit report, but for bank account behavior. If you had a checking account closed for overdrafts, bounced checks, or unpaid fees, there's a good chance you're in ChexSystems. Most banks check it before approving a new account — and if you're flagged, you get denied.

ChexSystems data stays on your record for 5 years.

Second-chance accounts don't check ChexSystems (or they look past it). Here are the real options:

**Capital One 360 Checking** Capital One uses its own evaluation instead of strict ChexSystems reliance. A lot of people with negative ChexSystems history get approved. No monthly fee, no overdraft fees. This is the cleanest second-chance path — you're getting a normal-ish account, not a punitive second-tier product.

**Chime** Chime doesn't use ChexSystems and approves nearly everyone. No monthly fee, SpotMe overdraft buffer (up to $200), early direct deposit. The app is excellent. The drawback: Chime is not a bank (it's a fintech that uses Bancorp Bank and Stride Bank as backend), which makes some people uncomfortable, though accounts are FDIC-insured.

**GO2bank (Green Dot)** $5/month fee, waived with qualifying direct deposit. Does not check ChexSystems. Offers an overdraft buffer up to $200 for eligible members. Fine as a temporary bridge.

**The Path Forward**

Second-chance accounts report your positive behavior to ChexSystems. After 12-24 months of no issues — no overdrafts, no returned items, no negative balance — your record looks better and you can qualify for standard accounts. Capital One 360 or Chime → 12-24 months of clean behavior → any major bank.

The other path: wait out the 5 years. Not always the fastest, but if you have an old account that'll age off ChexSystems soon, sometimes it's worth waiting.