1Why Most Budgets Fail Before February

You've done this before. January hits, you feel weirdly motivated, you open a spreadsheet or download an app, and you make this beautiful budget — color coded, every category filled in, totally realistic (you told yourself). Then life happens. The car needs tires. Your friend has a birthday dinner at a $90-per-head restaurant you didn't plan for. You buy coffee twice on a Tuesday. And by February 15th the whole thing is dead.

That's not a willpower problem. That's a system design problem.

Most budgets fail for a handful of very specific reasons, and once you see them you can't unsee them. The first one is that people build aspirational budgets instead of honest ones. They look at their spending and think 'I shouldn't be spending $400 on restaurants' and they write down $150. But they didn't change anything about their life — they just lied to their spreadsheet. A budget built on what you wish you spent is not a budget. It's a guilt document.

The second killer is that people treat a budget like a one-time project instead of an ongoing practice. You set it up once, forget to check it for three weeks, realize you're $600 over in groceries, feel terrible, and quit. A budget is more like a conversation with your money than a set of rules. It needs weekly check-ins — ten minutes, not two hours.

Third: too many categories. I've seen people make budgets with 40 line items. 'Work lunches' separate from 'personal lunches.' That level of granularity sounds impressive but it's cognitively exhausting to track. You'll stop. Five to eight categories is enough to start. You can always add later.

Fourth is the 'perfect or nothing' trap. You go over in dining by $30 and instead of adjusting next month, you just... abandon the whole system. A budget isn't a diet you cheated on. It's a tool. Tools that get used imperfectly are infinitely more valuable than perfect tools sitting in a drawer.

And fifth — the sneaky one — is forgetting non-monthly expenses. Your car insurance renews in March. Amazon Prime charges once a year. Your dentist isn't every month. When those hit, they feel like emergencies even though they were totally predictable. We'll cover sinking funds later in this guide, and that's exactly what they're for.

So what actually works? A budget that starts with your real numbers, not your ideal numbers. A system with very few moving parts. A check-in habit you can stick to even when life gets messy. And some kind of automation so the system runs even when you're not paying attention.

That's what this guide is going to give you.

2Every Major Budgeting Method, Actually Compared

There are five or six budgeting frameworks that show up everywhere. They're not all good. They're not all bad. They work for different people in different situations, and the one that works is the one you'll actually use — so let's get into the real differences.

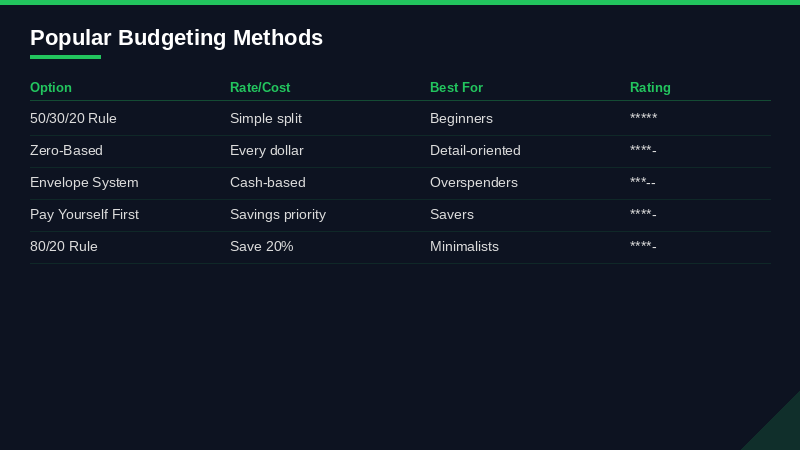

**The 50/30/20 Rule**

This is the most popular budgeting framework and also the most misunderstood. The idea is simple: 50% of your after-tax income goes to needs, 30% goes to wants, and 20% goes to savings and debt paydown. Senator Elizabeth Warren popularized it in a book she co-wrote with her daughter back in 2005, and it's held up surprisingly well as a starting framework.

Needs are housing, utilities, groceries, insurance, minimum debt payments, transportation. Wants are restaurants, entertainment, travel, subscriptions, hobbies. Savings is retirement contributions, emergency fund, extra debt payments.

Here's what people get wrong: they put too much in 'needs.' Your car payment on a car you bought because you wanted it is a want, not a need. Eating out three times a week is a want. The 50% needs category gets bloated when people are dishonest, and then there's nothing left for savings.

Who it works for: people who want a simple framework without tracking every dollar. People who are in reasonably good financial shape and just need guardrails. New budgeters who'd give up under something more complex.

Who it doesn't work for: people with high housing costs in expensive cities (in San Francisco or NYC, housing alone can eat 40-50% of take-home), people with significant debt, or people who need granular awareness to stay on track.

Real example at $60,000/year gross income (roughly $4,200/month take-home after taxes): $2,100 needs, $1,260 wants, $840 savings. That $840/month is $10,080/year — decent but not retirement-securing on its own.

**Zero-Based Budgeting**

This is the 'give every dollar a job' method. You take your monthly income and assign it to specific categories until you hit zero. Not zero money — zero unassigned dollars. If you make $4,500 a month, every single dollar gets a destination before the month starts.

This is what YNAB (You Need A Budget) is built on and it's genuinely powerful. The reason it works is that it forces you to make intentional decisions about money before you spend it, not after. You're not categorizing expenses in hindsight — you're allocating money with intention upfront.

It's more work than 50/30/20. You need to look at your numbers at least a couple times a month. And you need to 'roll with the punches' (YNAB's phrase for it) when reality diverges from plan — which it will, every month.

Who it's for: people who want tight control and are willing to do the work. People paying down debt aggressively. Anyone who tends to overspend and needs strong guardrails.

Who it's not for: people who hate administrative tasks, people with highly irregular income (though there are workarounds), anyone who burned out tracking every dollar before.

**Envelope Budgeting**

The old-school version of zero-based budgeting. You literally put cash in labeled envelopes — groceries, gas, restaurants, whatever — and when the envelope is empty, you're done spending in that category until next month. No credit cards, no debit cards for those purchases.

The physical cash thing is actually powerful psychology. People genuinely spend less with cash. The pain of handing over physical bills is more visceral than swiping a card, and that friction slows you down.

The digital version is apps like Goodbudget, which we'll cover in the apps section. You're not literally using cash but you're simulating the envelope system digitally.

Who it's for: people who massively overspend on discretionary categories and need a hard stop mechanism. People who do well with physical/tangible systems. People paying off debt who need to be strict.

Who it's not for: people who use credit cards for rewards and pay in full (cash envelopes remove that option for those categories), people with highly variable spending patterns, anyone who needs to track less not more.

**Pay Yourself First**

The reverse of how most people budget. Normally people spend first and save whatever's left — which is often nothing. Pay yourself first flips it: the moment income hits, you immediately transfer your savings targets out. Retirement contribution goes. Emergency fund contribution goes. House down payment fund goes. What's left is yours to spend however you want, no tracking required.

This is the simplest system in practice. It's not really a budgeting method — it's a savings automation strategy — but it can work on its own if your main goal is building wealth and you're not trying to solve overspending in specific categories.

Who it's for: higher earners who don't have a spending problem, just a saving problem. People who hate tracking. Anyone whose main goal is building long-term wealth rather than managing day-to-day cashflow.

Who it's not for: people living close to the edge where every category matters. Anyone with debt they're trying to aggressively kill. People who need visibility into where their money actually goes.

**Reverse Budgeting**

Slightly different from pay yourself first. Reverse budgeting means you identify your financial goals first, fund them immediately when income arrives, then spend freely from what remains. The 'reverse' is that goals come before lifestyle, not after.

It's very similar to pay yourself first but the emphasis is on goals rather than savings buckets. You're asking 'what am I trying to build?' before asking 'what do I want to spend?'

Practically speaking, the mechanics are almost identical. Automate transfers to goal accounts on payday. Live on the rest.

**The Anti-Budget**

Not a real methodology name — I made that up — but some people just need to hear that it's okay to keep it loose. The anti-budget approach: track your spending for one month without judging it, identify two or three obvious leaks, plug those, and otherwise stop stressing about it.

This isn't advice to be financially reckless. It's recognition that for some people, the effort required by a detailed budget produces anxiety and burnout that's worse than the alternative. If you're saving enough, not accumulating debt, and moving toward your goals, spending $80 on random Amazon purchases without categorizing them is fine.

**Which One Should You Actually Use?**

If you're in debt: zero-based budgeting or envelope method. You need the control. If you're fine but not saving enough: pay yourself first. Simple and effective. If you want a middle path: 50/30/20 as guardrails plus pay yourself first for savings. If you're already doing well: reverse budgeting. Just fund goals first, live on rest.

The best budget is the one you'll actually maintain for 12 consecutive months.

3Best Budgeting Apps in 2026, Ranked Honestly

Mint is dead. Intuit killed it in early 2024 and the personal finance app landscape has been reshuffling ever since. Here's where things actually stand in 2026.

**YNAB (You Need A Budget) — $14.99/month or $109/year**

Still the gold standard for people who want to actually change their financial behavior. YNAB isn't a tracking app — it's a behavior change system built around four rules: give every dollar a job, embrace your true expenses, roll with the punches, age your money.

The interface has improved dramatically over the last few years. Syncing is real-time, the mobile app is genuinely good, and the learning curve that used to scare people off has been smoothed out considerably. New users get a 34-day free trial, which is enough time to know if it's for you.

What it does better than anything else: it makes you have a conversation with your money before you spend it. That proactive relationship with your finances is what separates YNAB users from people who track expenses in hindsight and feel bad about them.

The criticism: $14.99/month is not cheap. Over a year that's $180. If you only use it for three months and abandon it — which a lot of people do — you've paid $45 for something that didn't stick. But people who do stick with YNAB are almost fanatically loyal, and many report saving thousands in the first year. The math works if you commit.

Best for: zero-based budgeting devotees, debt payoff, people who need structure and accountability.

**Monarch Money — $9.99/month or $99.99/year**

Monarch emerged from the Mint collapse as probably the strongest all-around alternative. It's built for couples as much as individuals, has clean net worth tracking, solid investment account syncing, and a genuinely pleasant UI. The collaborative features — shared dashboards, dual logins, combined view — are better than anything else in the space right now.

The budgeting methodology is more flexible than YNAB. You can do category-based budgeting, or just use it for tracking and reporting without a formal budget. That flexibility is a feature for some people and a bug for others (if you don't have to budget, you probably won't).

At $9.99/month it's meaningfully cheaper than YNAB with a broader feature set in terms of tracking. It doesn't do zero-based budgeting as philosophically — YNAB is built around that method, Monarch is built around visibility and management.

Best for: couples, people who also want investment tracking, anyone who wants Mint-like visibility with modern design.

**Copilot — $11.99/month or $95.99/year**

Copilot is the prettiest budgeting app I've used. It's also Mac/iOS only, which immediately kills it for Android users, full stop. If you're in the Apple ecosystem though, Copilot is legitimately excellent.

The AI categorization is the best in class. It learns your spending patterns and gets the categories right way more often than competitors. The 'insights' feature surfaces genuinely useful patterns — not just 'you spent more on food this month' but actual trends that change how you think about your spending.

The design is so good it makes people actually open the app. That sounds trivial but it's not. An app you open every day is infinitely more valuable than an objectively superior app you never check.

The limitation besides Apple-only: it's more of a tracking and analysis tool than a proactive budget builder. There's budgeting functionality but it's not the same philosophy as YNAB.

Best for: Apple users who care about design, people who want smart insights, anyone who tried YNAB and found it too rigid.

**EveryDollar — Free (limited) or $17.99/month with Ramsey+**

EveryDollar is Dave Ramsey's budgeting app and it's built around zero-based budgeting. The free version works but requires manual transaction entry (no bank sync without the paid plan). The paid version through Ramsey+ is the most expensive option on this list at $17.99/month.

The app is solid. The zero-based approach is effective. The Baby Steps integration makes sense if you're in the Ramsey universe — paying off debt, building emergency fund, working through the steps.

The reason some people avoid it: Dave Ramsey's methodology is dogmatic in ways that don't fit every situation. He's anti-credit card absolutely, for example, which is a legitimate strategy for some people but not optimal for everyone. If you're fine with the Ramsey philosophy, EveryDollar is well built. If you bristle at any of it, YNAB is a better zero-based alternative.

Best for: Ramsey Baby Steps followers, zero-based budgeters who want tight integration with that system.

**Goodbudget — Free (limited) or $10/month**

Digital envelope budgeting. You create envelopes, fund them, and spend against them. It's simple, it works, and it's particularly good for couples who want a shared system. The free plan allows 20 envelopes and two devices — enough to get started and see if you like it.

Goodbudget doesn't sync to your bank accounts. You enter transactions manually or import a file. That's by design — the manual entry creates intentionality and friction. But for people who want automatic sync, it's a dealbreaker.

Best for: envelope budgeting fans, couples who want to share a budget, people who want an extremely simple system, anyone suspicious of linking bank accounts to apps.

**PocketGuard — Free (limited) or $12.99/month**

PocketGuard's core feature is calculating how much is 'in your pocket' — spendable money after bills, goals, and necessities are accounted for. It's a simple 'how much can I safely spend today?' number that updates in real time.

It's a great concept and the execution is good. The limitation is that it's more of a spendable cash calculator than a full budgeting system. It won't give you the depth of YNAB or the tracking richness of Monarch.

Best for: people who just want to know if they can afford something, simplicity maximalists, anyone who gets overwhelmed by full budgeting systems.

**The Honest Ranking**

1. YNAB — best for behavior change and debt payoff, worth the price if you commit 2. Monarch — best all-arounder, especially for couples 3. Copilot — best design and AI, Apple-only 4. Goodbudget — best simple/manual option, great for envelope method 5. PocketGuard — best for simplicity, weakest for depth 6. EveryDollar — solid if you're a Ramsey follower, overpriced otherwise

Honest take: most people would be fine with Monarch at $9.99/month. If you have a spending problem you need to actively manage, pay for YNAB. If you're on iPhone and care about design, try Copilot's free trial.

Tracking spending is the part everyone avoids and the part that matters most.

4How to Actually Track Your Spending (And Not Hate It)

Tracking spending is the part everyone avoids and the part that matters most. Without data, you're just guessing. With data, you make decisions. Here's how to make tracking sustainable.

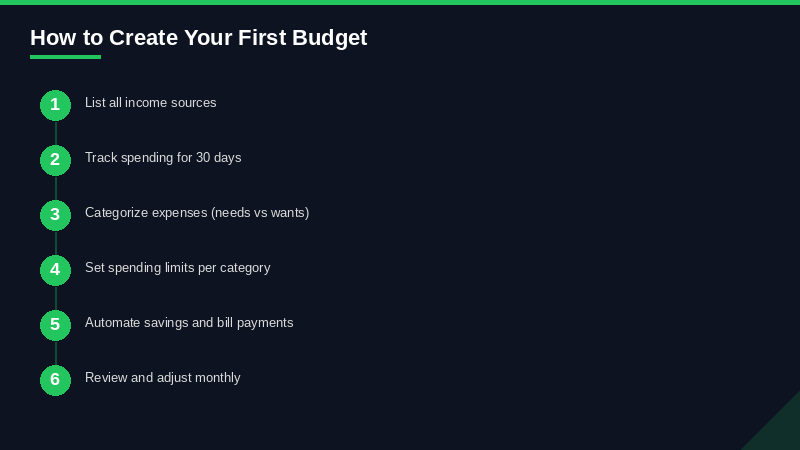

First, pick your method and commit for 90 days. Automatic syncing (YNAB, Monarch, Copilot) or manual entry (Goodbudget, spreadsheet) — both work, but mixing them halfway doesn't. If you go automatic, connect all your accounts: checking, savings, every credit card. If you go manual, get in the habit of entering transactions within 24 hours of making them.

Second, do a weekly 10-minute check-in. Not monthly — monthly is too infrequent to course-correct. Not daily — daily becomes obsessive and exhausting. Weekly is the rhythm that works. Set a recurring calendar event, Sunday night or Monday morning. Open the app, look at the week's spending by category, note anything surprising, adjust if needed. That's it. Ten minutes.

Third, categorize correctly from the start. Groceries are groceries. Target runs where you bought both groceries and a $40 shirt are not all groceries — split the transaction if your app allows it. Getting categories right in the first month saves enormous confusion later.

Fourth, review monthly and ask three questions: Where did I spend more than I expected? Where did I spend less? Is my savings rate moving in the right direction? You're not looking for perfection. You're looking for patterns.

Fifth — and this is the one people skip — track non-monthly expenses. Your annual subscriptions, quarterly insurance payments, semi-annual car registration. Put them in your tracking system even though they're not monthly. We'll talk about sinking funds below but you need visibility on these before you can plan for them.

A note on credit card tracking: credit cards make this easier, not harder, if you're using an app that syncs automatically. Every transaction is captured. With cash you have to remember or save receipts. The argument against credit cards for tracking is a myth — they generate perfect records. The argument against them for budgeting is that the psychological distance from spending makes it easier to overspend. Both things are true. Know which one applies to you.

Spreadsheet tracking is still completely valid in 2026. Google Sheets is free, there are dozens of good budgeting templates (search 'annual budget spreadsheet template' and you'll find clean ones), and if you're someone who finds app interfaces annoying, a spreadsheet you'll actually use beats an app you won't. The downside is manual entry for everything, but if that's the friction that keeps you engaged, it's worth it.

5Real Budget Breakdowns by Income Level

Abstract percentages are useless without actual numbers. Here are real breakdowns at four income levels using a modified 50/30/20 framework as a starting point, then adjusted for reality. All figures are monthly, post-tax.

**$30,000/year — roughly $2,200-2,400/month take-home**

This is tight. There's no way around that. At $30K, budgeting isn't optional — it's essential. The math doesn't work if you're not deliberate.

Housing: $700-800 (this means roommates in most markets, or a very low cost-of-living area) Groceries: $250-300 (meal planning, buying in bulk where possible, minimal eating out) Transportation: $300 (car payment + insurance + gas, OR public transit + occasional rideshare) Utilities + phone: $150 Health insurance: $100-200 (employer-subsidized or marketplace plan at this income level) Minimum debt payments: $200 (student loans, credit card minimums) Essentials subtotal: ~$1,750

That leaves roughly $450-650 for everything else — discretionary spending, savings, extra debt payments. At this level, you're choosing between building an emergency fund and having a social life, essentially. That's not a failure of character. It's math.

The priority at $30K: build a $1,000 starter emergency fund first (takes 2-3 months of disciplined saving), then throw everything extra at high-interest debt, then work toward a full 3-month emergency fund. Retirement contributions are secondary until consumer debt is gone — the interest rate arbitrage almost never works in your favor.

One thing that moves the needle dramatically at this income: increasing income. A second $5-10/hour is worth more than optimizing a budget that's already nearly optimized. The floor is the problem, not the allocation.

**$50,000/year — roughly $3,400-3,700/month take-home**

This is where budgeting starts to feel more like real decision-making rather than just survival. There's actual discretionary money here, which means there are actual choices to make.

Housing: $1,000-1,200 (one-bedroom in a mid-tier city, or share in a higher-cost city) Groceries: $350 Transportation: $400-500 (car payment, insurance, gas) Utilities + phone + internet: $200 Health + dental insurance: $200 Subscriptions (Netflix, Spotify, etc.): $80 Minimum debt payments: $300 Essentials subtotal: ~$2,530-2,830

Discretionary/savings pool: $870-1,170/month

With that pool, I'd allocate: — Emergency fund contributions: $300/month (until you hit 3 months of expenses, roughly $7,500-9,000) — Retirement: $300/month into 401k (especially if employer match — that's free money) — Dining/entertainment: $200 — Clothing/personal: $100 — Miscellaneous: $170

At $50K you can actually save meaningfully, eliminate debt within a reasonable timeline, and have a modest but real social life. It requires attention but it's not desperate.

**$75,000/year — roughly $4,900-5,400/month take-home**

$75K is where a lot of people start lifestyle creeping in ways that derail them. Suddenly a nicer car feels affordable. A bigger apartment feels justified. The raises start going toward consumption instead of wealth building.

Housing: $1,400-1,700 (reasonable for one-bedroom or splitting two-bedroom in most major cities) Groceries: $400 Transportation: $600 (nicer car payment, still reasonable) Utilities + phone + internet: $250 Insurance (health, renter's, auto): $350 Subscriptions: $100 Debt payments: $400 Essentials subtotal: ~$3,500

Discretionary/savings pool: $1,400-1,900/month

At this level, retirement contributions should be higher. At minimum: contribute enough to capture full employer match. Ideally: work toward maxing the IRA ($7,000/year in 2026 = $583/month) while also contributing to 401k.

Allocation suggestion: — 401k (enough for full match): $300 — Roth IRA: $583 — Emergency fund (if not fully funded): $200 — Sinking funds (car maintenance, travel, irregular expenses): $200 — Dining/entertainment: $250 — Remaining ~$367: split between extra debt payoff and truly discretionary

$75K is also where you can start having meaningful goals conversations. Down payment fund? Start here. Trip to Europe? Sinking fund. These become achievable in 1-2 year timeframes at this income with discipline.

**$100,000/year — roughly $6,200-7,000/month take-home (varies by state)**

At $100K, the question shifts from 'can I afford this?' to 'what do I actually want to build with my money?' The basics are covered. Now it's strategy.

Housing: $1,800-2,200 (comfortable one-bedroom or two-bedroom with roommate in most major markets) Groceries: $500 Transportation: $700 (or less if you choose not to have a car) Utilities + phone + internet: $300 Insurance (health, life, auto, renter's): $500 Subscriptions/services: $150 Debt payments: $500 (student loans, etc.) Essentials subtotal: ~$4,450-4,850

Discretionary/savings pool: $1,350-2,550/month

At $100K the retirement math gets serious. Max your 401k contribution ($23,500 limit in 2026 = $1,958/month — that's not realistic for most people at this income but it's the ceiling). Realistically: $1,000-1,500/month into retirement between 401k and IRA is achievable and puts you in very good shape for the long term.

Allocation suggestion: — 401k: $1,000-1,500 — Roth IRA: $583 — Emergency fund (maintain at 3-6 months): $0-100 once funded — Sinking funds: $300-400 — Dining/entertainment/travel: $400-500 — Miscellaneous discretionary: whatever remains

The danger at $100K is thinking you've 'made it' and not tracking anything. Lifestyle creep is silent and fast at this income level. People making $100K who feel broke almost always have housing costs above 35% of take-home or a car payment that's eating 15%+ of their income.

6Budgeting on Irregular Income

Freelancers, contractors, commission salespeople, anyone with variable income — the standard monthly budget model doesn't work for you. Here's what actually does.

First, identify your floor income. Look at your last 12 months and find your lowest earning month. Not your average — your worst month. That's your budget baseline. Every fixed expense and minimum savings target has to work on that number. When you earn more, the extra goes to filling in the gaps and building reserves, not upgrading your lifestyle.

Second, open a 'buffer account.' This is separate from your emergency fund. It's a dedicated checking or high-yield savings account where you deposit income as it comes in, then 'pay yourself' a consistent monthly salary from it. If you make $4,000 in January and $9,000 in February, you pay yourself $5,000 both months. The buffer absorbs the variability. This is the single most effective system for irregular income budgeting because it converts chaos into predictability.

You want 1-3 months of your 'salary' in the buffer account as a cushion before you start this system. That takes time to build but it's worth doing. Without the buffer, you're still vulnerable to feast-and-famine cycles.

Third, taxes first. Always. This is where self-employed people get burned. Immediately upon receiving income, transfer your estimated tax withholding to a dedicated tax account. For most self-employed people this is 25-30% of gross income depending on your situation. Adjust based on your actual prior-year tax rate. Do not touch this money. Quarterly estimated payments go from this account.

Fourth, build your budget percentages on net income after taxes are set aside and before anything hits your buffer. Your budgeted 'salary' should already reflect this.

For irregular income, I'd rank the budgeting methods this way: zero-based budgeting wins, because it forces you to re-budget every month based on what actually came in. The 50/30/20 rule works as guardrails. Envelope budgeting is harder because irregular income makes envelope funding inconsistent month-to-month.

One more thing: irregular income budgeters need a bigger emergency fund. Where salaried employees might be fine with 3 months of expenses, people with variable income should target 6 months minimum, ideally closer to 9 months if your income swings are large. The math is different. Your income itself is more volatile, so you need more cushion against a bad run.

7Budgeting for Couples: How to Do Money Together Without Ruining Your Relationship

Money is one of the top causes of divorce. Which means getting this right is not just a financial question — it's a relationship question. And unlike most financial decisions, there's genuine legitimate disagreement about the right approach.

There are basically three systems couples use:

**Full merge.** All income goes into joint accounts. All spending comes from joint accounts. No individual allowances, no separate spending money. This is the traditional model and it works for couples with similar spending habits, similar financial goals, and high mutual trust. The advantage is total transparency and maximum savings power. The challenge is that autonomy disappears — buying your partner a surprise gift, spending on a hobby they think is stupid, or just having independent purchases without justification feels impossible.

**Full separation.** Each partner keeps their own accounts, splits shared expenses (usually proportionally to income), and maintains independent financial lives. This works for people who were financially independent before the relationship and value autonomy highly. The challenge is that it can create an adversarial dynamic around shared expenses and makes long-term joint goals harder to coordinate.

**The hybrid (what most couples actually need).** Joint accounts for shared expenses — rent/mortgage, utilities, groceries, shared subscriptions, saving toward joint goals. Individual accounts for personal spending, each partner gets a 'no questions asked' personal spending budget. This approach respects autonomy while pooling resources for shared goals.

How to determine the personal spending budget: decide as a couple what the total monthly household discretionary budget is, then split it however makes sense for your situation. Equal splits work for roughly equal incomes. Proportional splits work when income is highly unequal. The important thing is that the personal budget is genuinely no-questions-asked — you don't interrogate each other's spending within it.

The actual conversation you need to have, which most couples avoid: values alignment. Does one partner prioritize experiences (travel, restaurants) while the other prioritizes security (bigger emergency fund, faster retirement contributions)? Does one partner have debt the other doesn't? Are your income trajectories similar or very different? These conversations are uncomfortable but they're the foundation. Budget mechanics without values alignment is just papering over conflict.

Practically, Monarch Money is the best app for couples right now. It supports two-person login, shared dashboards, and combined net worth tracking. YNAB works well too. Goodbudget is excellent for couples who like the envelope method and want simplicity.

One rule that prevents a lot of fights: agree on a spending threshold above which both partners discuss before purchasing. $200 is a common number. Below that, spend freely within your personal budget. Above that, quick conversation. This isn't about controlling each other — it's about preventing the surprise of a $500 purchase appearing on the statement.

And please — schedule a monthly money date. It sounds corny but couples who talk about money regularly have dramatically fewer financial arguments than those who avoid it until there's a crisis. Thirty minutes, wine if you want, look at last month together, plan next month. That's it.

Three to six months of expenses is the standard advice.

8Emergency Fund: How Much Is Actually Enough

Three to six months of expenses is the standard advice. It's also incomplete.

Here's what actually determines how much emergency fund you need:

Job security: If you work in a stable profession with high demand (nursing, accounting, certain trades), three months is probably fine. If you're in a volatile industry, work in media or tech where layoffs happen suddenly, or are self-employed, you want six months minimum. I'd argue nine months if your income is very irregular.

Dependents: Kids change the calculus. Medical emergencies, school emergencies, dependent income surprises — they multiply. Add one to two months for each dependent, roughly.

Income situation: Single income household? The risk of that one income stopping is unhedged. Two-income household? If one partner loses a job, the other is still bringing money in. Two-income households can get away with three months where single-income households need five or six.

Health: Chronic health issues, high-deductible health plans, anything that could generate a large unexpected medical bill — factor that in. Know your out-of-pocket maximum on your health insurance. That number should be covered by your emergency fund alone.

What counts as an emergency fund: it has to be liquid. High-yield savings account. Money market account. Not stocks. Not I-bonds you can't redeem for 12 months. Not your Roth IRA (even though contributions can technically be withdrawn penalty-free, using retirement money for emergencies is a bad habit). Liquid. Accessible within one to two business days.

Where to keep it: a high-yield savings account separate from your main checking account. Wealthfront Cash Account currently pays competitive rates. Ally Bank. Marcus by Goldman Sachs. SoFi. The separation is intentional — 'out of sight, out of mind' reduces the temptation to dip in for non-emergencies.

What is and isn't an emergency: job loss, major medical expense, critical car repair, major home repair — yes. A sale you don't want to miss — no. A vacation you didn't budget for — no. Your friend's destination wedding — no (that's a sinking fund situation). The emergency fund is for genuine emergencies, not big discretionary spending you didn't plan ahead for.

How fast to build it: most financial planners say build a $1,000 starter emergency fund first, then focus on high-interest debt, then fully fund the emergency fund. That sequencing is right. The reasoning is that without any buffer, every minor unexpected expense goes on a credit card and defeats your debt paydown progress. The $1,000 starter fund creates a buffer for the small stuff while you're working on bigger debt.

At $50K income: a fully funded emergency fund is around $8,000-12,000 (three to six months of $2,500-4,000 monthly expenses). That takes 18-24 months saving $400-500/month. That's normal. Don't be discouraged by the timeline.

9Sinking Funds: The Budget Category Most People Are Missing

A sinking fund is money you set aside every month for a predictable future expense. The name comes from accounting — 'sinking' a debt over time. But the concept is simple: if you know you're going to spend money on something eventually, save for it monthly so it doesn't feel like an emergency when it arrives.

Examples that should absolutely be sinking funds:

Car maintenance: Average car repair in the US is now over $400. Oil changes, tires, unexpected repairs — if you have a car, you will spend money on it. Set aside $75-150/month depending on the age of your vehicle.

Annual subscriptions: Amazon Prime ($139/year), Microsoft 365 ($99/year), Costco membership ($65/year), your domain renewal, your antivirus software. Add them up, divide by 12, set that aside monthly.

Holidays: Most people spend $500-1,500 on Christmas gifts and travel. Divide by 12, that's $42-125/month. If you're saving $100/month starting in January, you have $1,200 by December and you're not putting gifts on a credit card you'll be paying off until March.

Vacation: Same math. Decide what you want to spend on vacation this year. Divide by 12. Save that monthly.

Medical/dental: Even with insurance, copays and deductibles add up. $50-100/month for a health-related sinking fund is realistic.

Home repairs (if you own): The common rule is 1-2% of home value per year for maintenance. On a $350,000 house that's $3,500-7,000/year or $290-580/month. That sounds like a lot until your HVAC dies and you need $5,000.

How to structure sinking funds: they can live in separate high-yield savings account buckets (Ally and Marcus let you create named sub-accounts), in a spreadsheet that tracks earmarked amounts within one account, or as categories in YNAB (which is actually perfect for this).

The psychological shift sinking funds create is significant. When December rolls around and Christmas shopping doesn't stress you out financially — that's the system working. When your car needs new brakes and you just... pay for it without an emotional crisis — that's the sinking fund doing its job. These formerly irregular expenses become predictable, budgeted, non-events.

Realistic starting list for most people: car maintenance ($100/month), holidays ($100/month), vacation ($150/month), medical ($75/month). That's $425/month that used to feel like emergencies and now just... isn't.

10How to Actually Cut Expenses (With Specific Scripts)

Everyone tells you to cut subscriptions and skip lattes. Here's the actual substance behind those clichés — and some approaches that move real money.

**The Subscription Audit**

Open your bank and credit card statements from the last three months. Look for every recurring charge. Every single one. Make a list. You will find services you forgot about. I guarantee it.

For each subscription, ask two questions: Did I use this at all in the last 30 days? If yes — would I sign up for it today at this price if I didn't already have it? The second question is the important one. Subscriptions have a way of feeling 'free' because the charge is automatic and you've been paying for months. But if you saw a sign-up page today for a service you barely use at $12.99/month, would you enter your credit card? If the answer is no, cancel it.

Common forgotten subscriptions: gym memberships (average American has 2.3 unused streaming services), free trials that converted to paid, app subscriptions from 2 years ago, Audible credit accumulations, newspaper subscriptions from news addiction periods, Duolingo Plus, cloud storage you've outgrown the need for.

The average American household pays for subscriptions they don't use regularly. A one-hour audit can realistically save $50-150/month.

**Insurance Shopping**

Auto and home/renters insurance premiums have gone up significantly in 2024-2025. Shopping your rates annually is now more valuable than it used to be. Rates vary widely between carriers even for identical coverage.

Auto insurance: Get quotes from at least three carriers. Use a comparison site (The Zebra, Policygenius) to get multiple quotes fast. Raising your deductible from $500 to $1,000 typically drops your premium 10-15%. Bundling home and auto with the same carrier saves 5-15%. If you're a low-mileage driver, ask about per-mile insurance (Root, Metromile before it merged) or usage-based discounts.

Renters/homeowners insurance: Same comparison shopping approach. Make sure you're not over-insured on personal property if you haven't updated your policy since you moved in.

Health insurance: During open enrollment, actually compare plans instead of auto-renewing. A high-deductible health plan paired with an HSA makes sense for healthy people who don't use much healthcare — the premium savings often exceed the deductible difference, and the HSA contribution is triple-tax-advantaged.

**Negotiation Scripts**

You can negotiate more bills than you think. Here are specific approaches:

Internet/cable: 'I'm looking at switching to [competitor name] — they're offering [competitive rate] for similar service. I've been a customer for [X years]. Is there anything you can do for me?' Retention departments have authority to offer discounts. Call, don't email. Being ready to actually cancel increases your leverage.

Credit card interest rate: 'I've been a customer for [X years] and I've maintained a good payment history. I'd like to request a reduction in my APR.' This doesn't always work but success rates are higher than most people expect, especially with good payment history. A 3-5% rate reduction on a $5,000 balance saves $150-250/year.

Medical bills: Never pay the first number on a medical bill. Call and ask for the self-pay discount (if you're paying out of pocket) or ask billing to review the charges for errors (there often are some). For large bills, ask about payment plans with no interest. For truly unaffordable bills, ask about financial assistance programs — hospitals are legally required to offer them if they're nonprofit, and most are.

Gym membership: 'I'm considering canceling — is there a lower tier or a promotional rate I could switch to?' Most gyms would rather keep you at $20/month than lose you at $50/month.

**Food and Groceries**

Food is one of the few variable expenses with significant room to cut without lifestyle degradation if you're strategic. A few approaches that actually move the needle:

Meal planning before grocery shopping. Not a rigid meal plan necessarily — just knowing what you'll cook for the week before you shop. This eliminates random purchases that don't turn into meals and reduces food waste (Americans throw away roughly 30-40% of food purchased, which is essentially money in the garbage).

Focus cooking proteins in bulk. Chicken thighs, ground beef, beans, eggs — buy in quantity, cook on Sunday, use throughout the week. Convenience is the actual enemy of a food budget, and batch cooking reduces the 'I don't feel like cooking, let's just order' moments.

Reduce but don't eliminate restaurants. Going from dining out 5 times a week to 2-3 times a week while not suffering socially is realistic for most people. Going from 5 to zero is not realistic and leads to binge splurges.

11Budgeting for Major Goals

Goals are why budgeting matters. The discipline isn't the point — the house, the wedding, the trip, the retirement — those are the point. Here's how to actually budget for the big ones.

**House Down Payment**

The math in 2026: median home price in the US is roughly $415,000. A 20% down payment is $83,000. A 10% down payment (still avoiding PMI at many lenders with right qualifications, or accepting PMI costs) is $41,500.

At $500/month saved in a high-yield savings account earning 4-4.5%: $41,500 in roughly 7 years. That's a long time. To compress the timeline: $1,000/month gets you there in 3.5 years. $1,500/month in 2.5 years.

Where to hold down payment savings: high-yield savings account for anything you need within 2 years (rates currently 4-5% at Wealthfront, Betterment, Ally). If your timeline is 3+ years, a CD ladder or low-risk bond funds are reasonable. Do not put your down payment fund in stocks unless your timeline is 5+ years and you're genuinely prepared to push back your purchase if the market tanks.

First-time homebuyer programs: many states have programs offering down payment assistance, reduced rates, or grants. Check your state housing finance agency before assuming you need the full 20%.

**Wedding**

Average US wedding cost in 2026 is around $35,000. That's a number that makes a lot of people feel sick, and honestly it should — it's a lot of money for one day. But the range is enormous: $10,000 to $100,000+, and the drivers are guest count and venue.

If you're planning to budget for a wedding: start 18-24 months out. Decide on a target number before falling in love with venues. Guest count is the biggest lever — cutting 30 guests can save $6,000-9,000 depending on cost per head.

Save in a dedicated HYSA. At 4% yield, $1,500/month for 24 months generates roughly $37,400 plus interest. If you have family contributions, factor those in separately.

**Baby**

The first year of a baby's life costs $15,000-25,000 depending on childcare situation and location. Childcare alone in major cities can run $2,000-3,000/month. If you're planning a family, start the financial prep at least 18 months before your target date.

Key financial moves before baby: max your HSA if you're on an HDHP (a birth and first-year medical costs are substantial), build your emergency fund to 6 months (income disruption risk goes up), check employer maternity/paternity leave policy and plan for any unpaid leave period, investigate childcare costs in your area before conception if possible (waitlists for infant daycare in many cities are 12-18 months long).

**Retirement**

The 4% rule: you need 25x your annual expenses to retire. If you spend $60,000/year, you need $1.5 million. If you spend $80,000/year, $2 million.

The timeline math: at a 7% average annual return, investing $500/month from age 25 grows to roughly $1.37 million by age 65. $1,000/month from age 25 grows to about $2.74 million. The same $1,000/month started at age 35 grows to only about $1.2 million by age 65. Time is the variable that matters most. Starting late is still better than not starting, but the cost of waiting is real.

Your money priorities should shift as your life changes.

12Financial Goals by Decade

Your money priorities should shift as your life changes. Here's a realistic framework for each decade — not aspirational puffery, just what the math and the research support.

**Your 20s: Foundation**

The 20s are about building the foundations that compound over everything else. The biggest financial mistake of your 20s isn't overspending — it's not starting retirement contributions because the amount seems too small to matter.

Priorities in order: 1. Emergency fund: $1,000 starter, then 3 months of expenses 2. Employer 401k match: always, no exceptions. This is a 50-100% immediate return 3. Pay off high-interest debt: anything above 7-8% APR 4. Roth IRA: ideal account for 20s because you're probably in a lower tax bracket now than you will be later 5. Build skills and income: in your 20s, increasing your income capacity matters more than optimizing a small budget

What to avoid: lifestyle inflation when income increases. Every raise should go partially to savings before going to spending. The first raise you get, direct 50% to increased retirement contributions. You won't miss money you never saw.

**Your 30s: Acceleration**

The 30s typically bring higher income, often major life events (marriage, kids, home purchase), and the beginning of real wealth building.

Priorities: 1. Adequate emergency fund (6 months with kids or a mortgage) 2. 401k and IRA contributions — target 15% of gross income toward retirement 3. Life insurance (if you have dependents — term life, not whole life) 4. Mortgage if homeownership is a goal 5. College savings (529) if you have or plan to have kids — don't sacrifice your retirement for kids' college. They can get loans. You can't borrow for retirement.

The income-lifestyle-wealth triangle: in your 30s, income goes up but so do expenses (house, kids). The gap between what you earn and what you spend is what becomes wealth. Guard that gap aggressively.

**Your 40s: Wealth Accumulation**

The 40s are when the math starts doing heavy lifting if you've been consistent. Compound interest starts to visibly accelerate your account balances.

Priorities: 1. Max out tax-advantaged accounts if possible — 401k ($23,500 in 2026), IRA ($7,000) 2. Catch-up contributions start at age 50 ($7,500 extra in 401k) — plan for this 3. Children approaching college age — 529 contributions, financial aid strategy 4. Mortgage paydown strategy (personal decision — not always the mathematically optimal choice, but often the emotionally valuable one) 5. Begin tax diversification: mix of traditional (pre-tax) and Roth (post-tax) accounts

The dangerous 40s trap: 'I'll catch up on retirement later.' You're past the point where time is unlimited. The next 20 years will be the most important of your wealth building window.

**Your 50s: Pre-Retirement**

The 50s are about preparation, risk management, and catching up if needed.

Priorities: 1. Catch-up contributions: 401k catch-up is $7,500/year extra at 50+. Use it. 2. Get a clear retirement projection: not 'am I saving enough' in the abstract, but an actual projection with actual numbers 3. Reduce risk in investment portfolio gradually — the sequence-of-returns risk matters more as you approach retirement 4. Pay off mortgage if you plan to retire with a paid-off home 5. Long-term care insurance: 50s is the time to buy it (cheaper than waiting to 60s, at a point where you can still get it)

Lifestyle cost check: in your 50s, kids are (hopefully) financially independent, mortgage may be lower. Do your actual monthly expenses support the retirement income you're planning for?

**Your 60s: Transition**

Priorities: 1. Social Security optimization: when to claim is one of the biggest financial decisions of retirement. Waiting from 62 to 70 increases your benefit by roughly 76%. If you're healthy, waiting pays off. Run the break-even analysis. 2. Roth conversion strategy: before RMDs kick in at 73, consider converting traditional IRA money to Roth in the low-income years between retirement and Social Security 3. Healthcare bridge: if you retire before 65, you need health insurance for the Medicare gap years. This is often the biggest overlooked cost in early retirement plans 4. Withdrawal rate planning: the 4% rule is a starting point, not a law. Adjust for your specific situation, Social Security income, pension if any, and expense projections

13Cash Management Accounts and High-Yield Savings

If your emergency fund and short-term savings are sitting in a traditional bank savings account earning 0.01-0.5%, you're leaving meaningful money on the table. The options for parking cash have gotten genuinely good.

**Wealthfront Cash Account**

Currently one of the best cash accounts available. Offers FDIC insurance through partner banks (up to $8 million for individual accounts via program banks), no minimum, no fees, and competitive APY that adjusts with the Fed funds rate. Wealthfront also offers automated investing if you want to graduate from cash to investment accounts on the same platform. The interface is clean, transfers are fast (typically 1 business day), and the mobile app is solid.

The slight downside: it's not a traditional bank. No physical branches, no ATM access (cash is for savings, not day-to-day spending). Use it alongside a checking account, not instead of one.

**Betterment Cash Reserve**

Betterment's high-yield savings product. Similar FDIC insurance structure through partner banks, competitive APY, no minimum, no fees. Betterment's advantage is the integrated investment accounts — if you want your emergency fund, short-term savings, and investment portfolio all in one place with automatic rebalancing and tax-loss harvesting, Betterment is a strong integrated option.

**Ally Bank**

The established player. FDIC insured (traditional, not program bank), no minimum, no fees, competitive rates. Ally's biggest advantage is the sub-account feature — you can create separate buckets within one savings account, which is perfect for sinking funds. Name them 'Car Maintenance,' 'Vacation 2026,' 'Holiday Gifts,' and fund each separately. Ally also has a checking account and CDs if you want everything under one digital roof.

**High-Yield Savings vs. Money Market vs. CDs**

High-yield savings: most flexible, rate adjusts with Fed, instant liquidity. Best for emergency funds and sinking funds where you need access.

Money market accounts: similar rates, often slightly higher minimums, sometimes come with check-writing. Functionally similar to HYSA for most purposes.

CDs: higher rates in exchange for locking up money for a term (3 months to 5 years). Best for money you know you won't need. A CD ladder (buying CDs with staggered maturities) gives you both rate and liquidity.

In 2026 with rates where they are: a HYSA earning 4-5% APY on your emergency fund is meaningful money. On a $15,000 emergency fund, that's $600-750/year in interest, tax-deferred in a standard savings account structure. Take the free money.

14Automating Your Finances

The goal of automation is to make good financial behavior the default instead of the exception. Willpower is finite. Systems are indefinite.

Here's the full automation stack, in order of setup:

**Step 1: Direct deposit split**

If your employer allows it, split your direct deposit. Route the savings percentage directly to a separate savings account before it ever hits checking. 15% to savings, 85% to checking. You never see the savings amount in your spending account, so it doesn't feel like you're saving — it just happens.

If direct deposit split isn't possible, set up an automatic transfer from checking to savings on payday — the day income arrives, not a week later when you've already spent some of it.

**Step 2: Automate retirement**

401k contributions are already automatic if you're enrolled — they come out pre-paycheck. Make sure you're contributing enough to get the full employer match. If your employer auto-enrolled you at 3%, that's probably not enough. Bump it up. Most 401k platforms let you schedule an annual 1% increase automatically — set that up once and forget it.

IRA contributions: set up a monthly automatic investment into your IRA. $583/month funds a full $7,000 IRA in a year. Even $200/month is meaningful compounding.

**Step 3: Automate bill payments**

Auto-pay every fixed bill: rent/mortgage, utilities, car payment, insurance, phone. Fixed amounts, predictable dates, zero thought required. For credit cards: auto-pay the full statement balance, not the minimum. Minimum payment autopay is a trap — it means you'll never accidentally miss a payment, but you'll also carry a balance if you forget to manually pay more.

**Step 4: Sinking fund automation**

For each sinking fund category, set up an automatic monthly transfer on payday. $100 to car maintenance bucket, $125 to vacation bucket, $100 to holiday fund. These run without intervention. When the goal is funded, redirect the automation.

**Step 5: Investment automation**

Beyond retirement accounts: if you have a taxable brokerage account (you should once you've maxed tax-advantaged space), set up automatic investment into a simple index fund — total market or S&P 500 equivalent. Dollar cost averaging removes the 'when to invest' anxiety and ensures you buy in both up and down markets.

Wealthfront and Betterment both automate the investment side completely. You set a target allocation, they handle rebalancing, dividend reinvestment, and tax-loss harvesting. Fidelity and Schwab auto-invest features work similarly with individual funds.

**What automation doesn't replace**

Automation handles execution. It doesn't replace judgment. You still need to review your spending monthly to catch drift, adjust savings rates when income changes, and rebalance your financial plan when life changes (new job, move, new family member, debt payoff). The automation takes away the daily execution burden. The monthly review takes care of the rest.

Target time commitment once fully automated: one hour setup, ten minutes weekly, thirty minutes monthly. That's it. Your finances run in the background like utilities.

15Building a Budget When You Feel Like You Have Nothing Left

Some people reading this are doing the math and it doesn't work. Income covers expenses with nothing left over, or barely. The budget advice of 'save 20%' feels like a cruel joke when you're trying to figure out how rent and groceries both happen this month.

This section is for that situation specifically.

First, the honest take: if your income genuinely doesn't cover your necessary expenses, budgeting is a symptom treatment, not a cure. The underlying problem is an income gap, and that requires either income increase or expense reduction at a structural level — not just optimization.

But here's what does help even when the math is tight:

Know your actual numbers. Even when the numbers are bad, knowing them is better than not knowing. Uncertainty about money is more stressful than bad certainty. If you know you have $200 left after bills, you can make a decision. If you don't know, you'll spend $300 and feel blindsided.

Prioritize in this order: food, housing, utilities, transportation to work. These before everything. Credit card minimum payments before credit card extra payments. Medical minimums. Everything else is secondary when money is genuinely scarce.

Call people. Medical bills, utility companies, credit card companies, student loan servicers — all of them have hardship programs that are not well advertised. 'I'm experiencing financial hardship and I'd like to explore payment reduction options' is a sentence that unlocks programs that exist specifically for this situation.

Look for income opportunities before cutting anything more. At very low incomes, the spending side has very little room left. The income side has more. One additional shift per week, a small side service, selling unused items — even $200-300/month in additional income can change the whole picture at lower income levels.

And the small thing that actually matters: a $1,000 emergency fund. Even at very tight incomes, working toward that number first before everything else creates a buffer between you and the cycle where every unexpected expense becomes a new credit card balance.